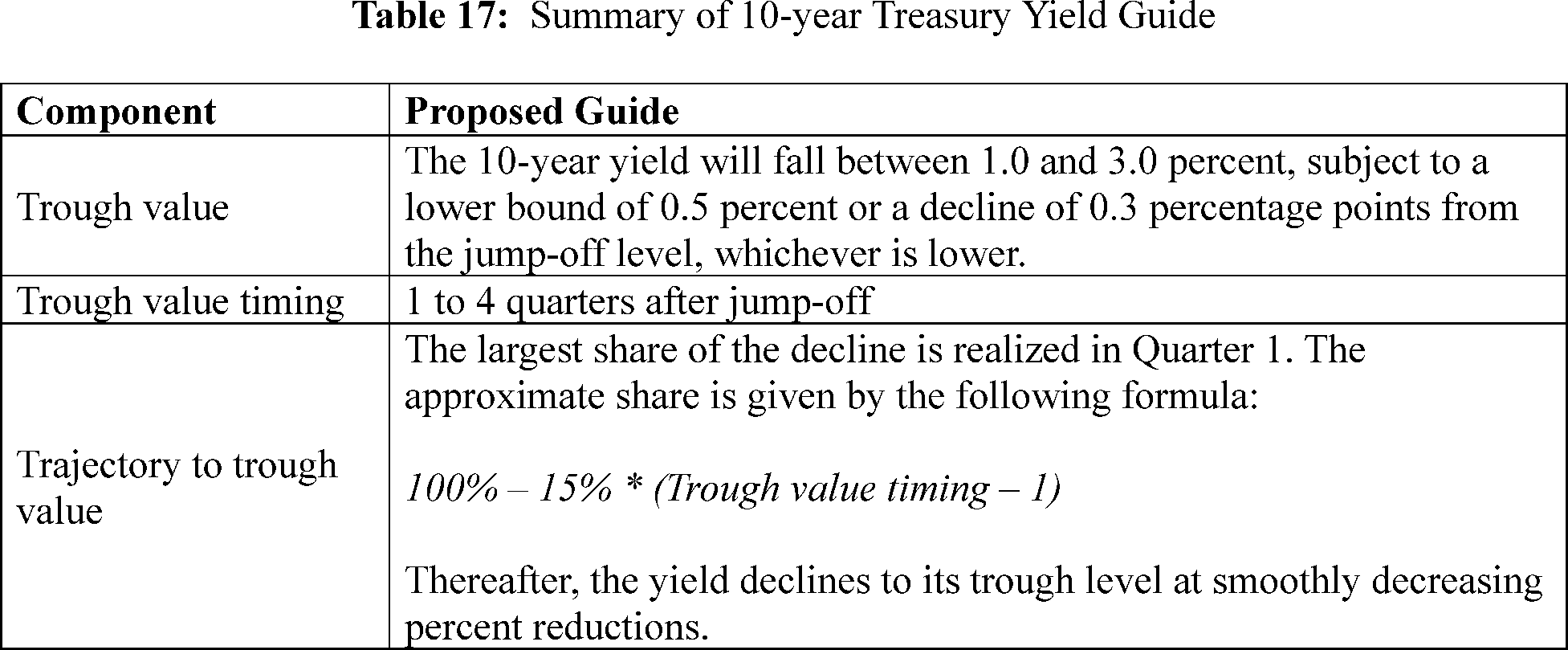

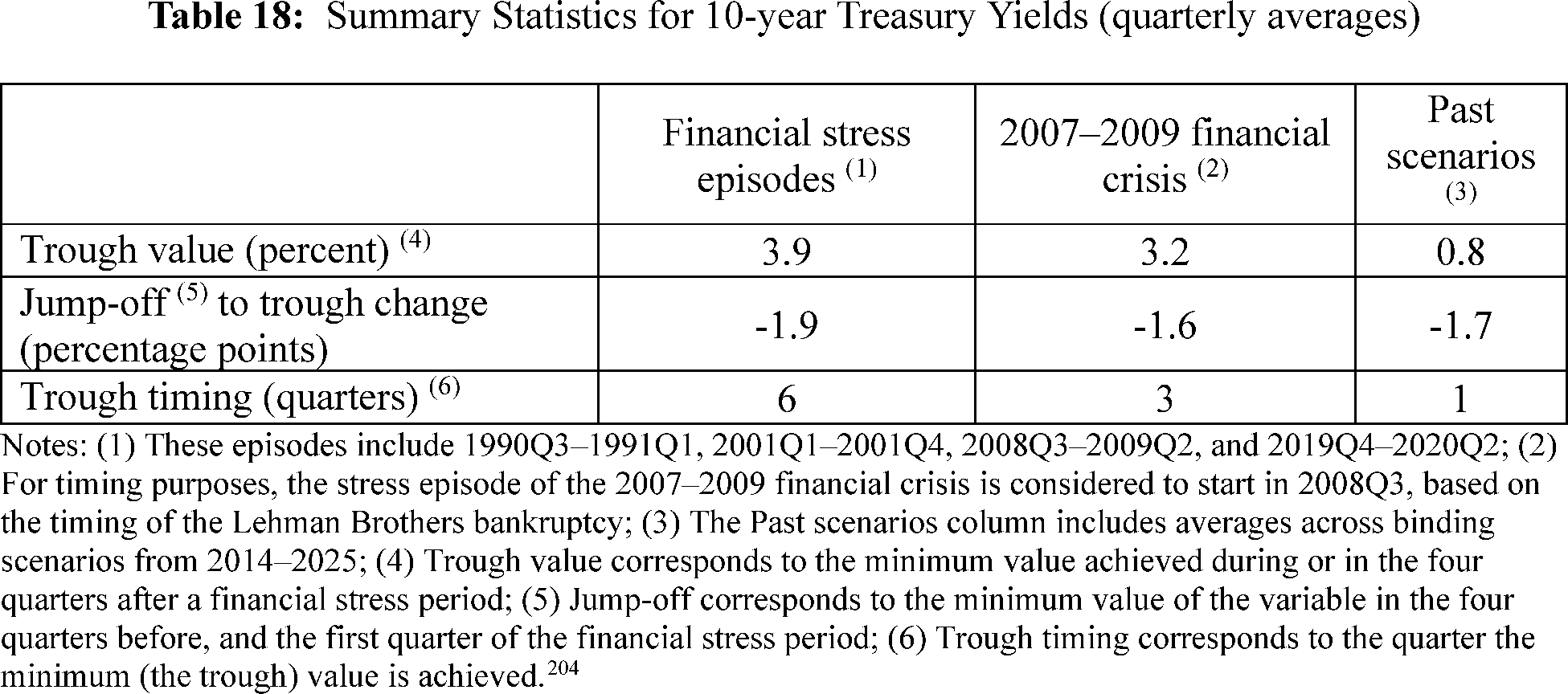

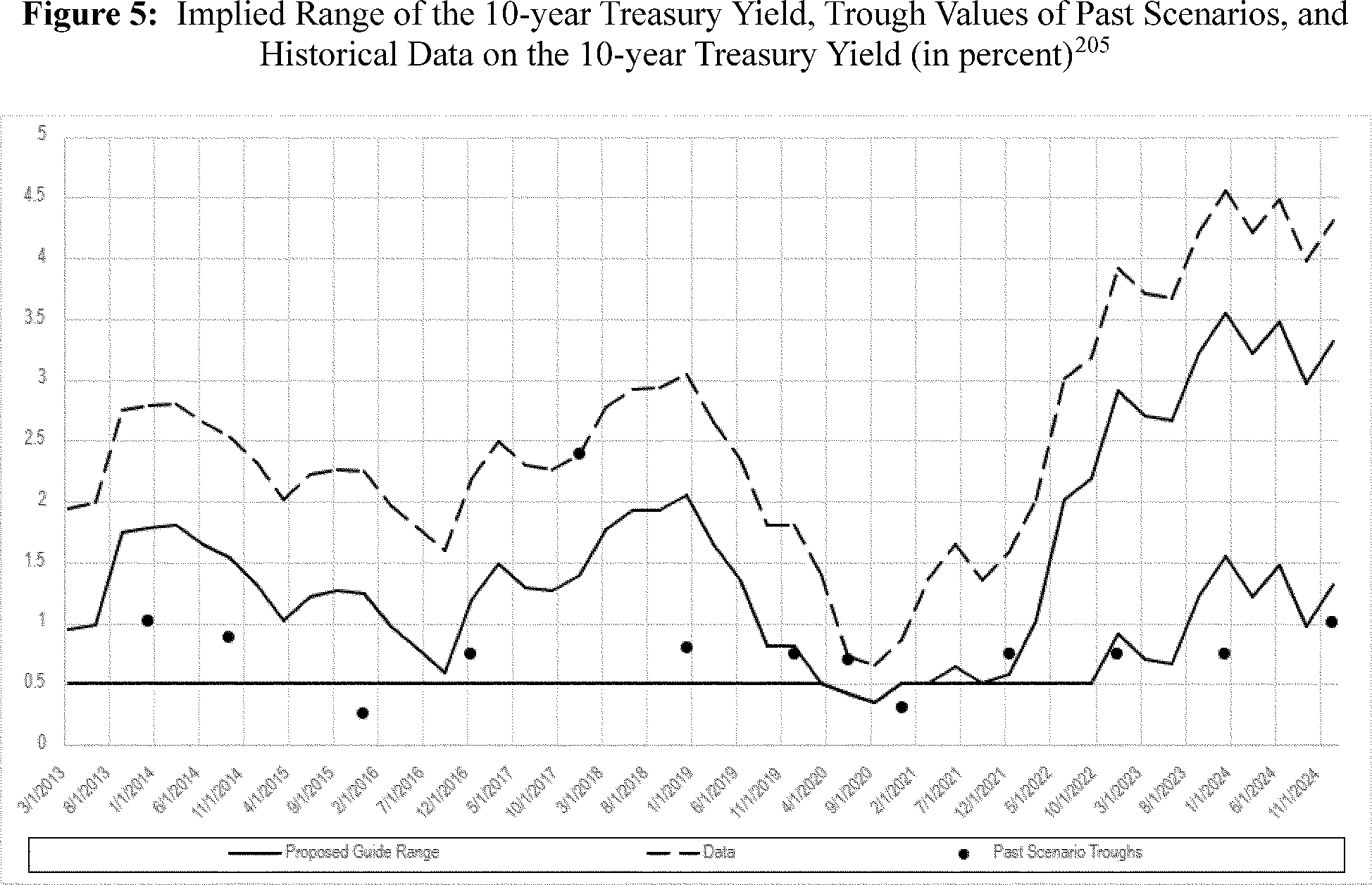

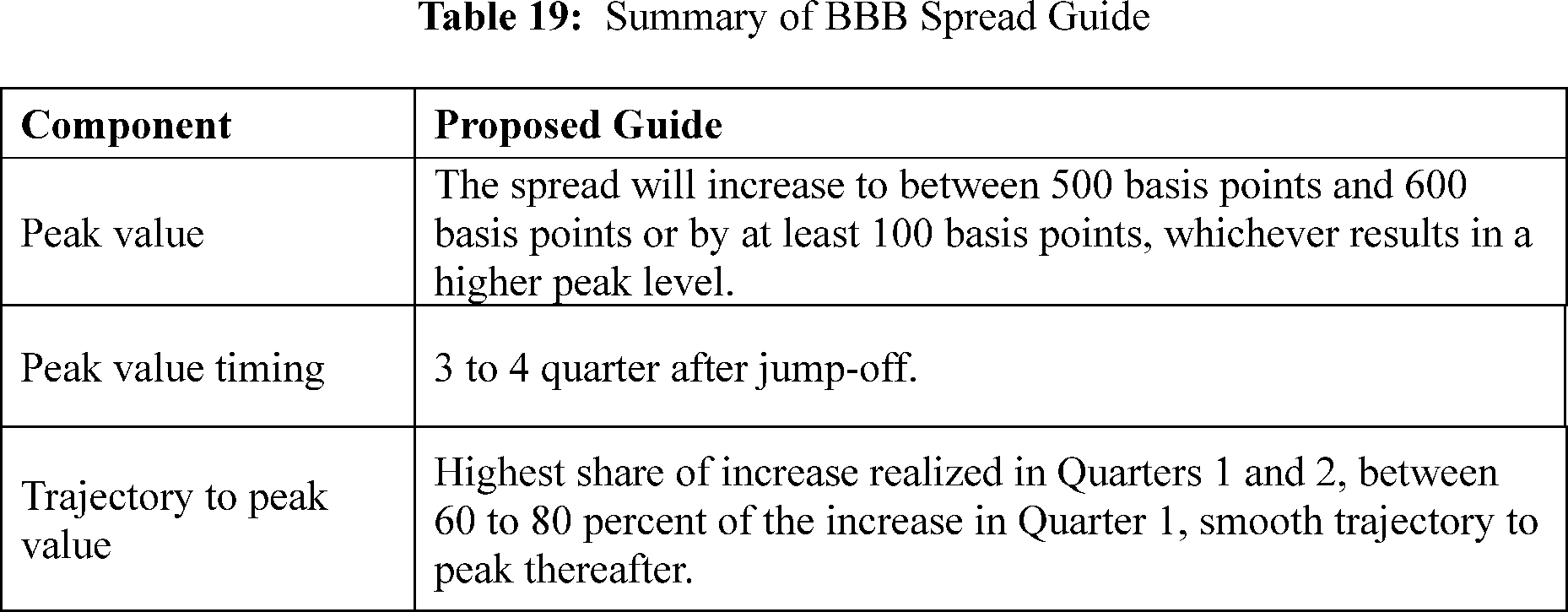

Federal Reserve System

Enhanced Transparency and Public Accountability of the Supervisory Stress Test Models and Scenarios; Modifications to the Capital Planning and Stress Capital Buffer Requirement Rule, Enhanced Prudential Standards Rule, and Regulation LL

November 18, 2025

Summary

The Federal Reserve is proposing changes to its supervisory stress testing framework to increase transparency, accountability, and public participation in the model design process. The proposal includes new procedures for publishing model documentation and stress test scenarios for public comment, along with adjustments to FR Y-14A/Q/M data collection and stress testing policy statements.

AI-generated summary · May 24, 2026. Verify with your compliance counsel before acting.

How this was generated

We record the exact prompt, model, and output for every AI response so it can be audited for accuracy.

Document headings vary by document type but may contain the following:

- the agency or agencies that issued and signed a document

- the number of the CFR title and the number of each part the document amends, proposes to amend, or is directly related to

- the agency docket number / agency internal file number

- the RIN which identifies each regulatory action listed in the Unified Agenda of Federal Regulatory and Deregulatory Actions

See the Document Drafting Handbook for more details.

Federal Reserve System

- 12 CFR Parts 225, 238, and 252

- [Regulations Y, LL, and YY; Docket No. R-1873]

- RIN 7100-AH05

AGENCY:

Board of Governors of the Federal Reserve System (Board).

ACTION:

Notice of Proposed Rulemaking.

SUMMARY:

The Board is inviting public comment on the models used to conduct the Board's supervisory stress test, changes to those models to be implemented in the 2026 stress test, and proposed changes to enhance the transparency and public accountability of the Board's stress testing framework (the proposal). The proposal would amend the Policy Statement on the Scenario Design Framework for Stress Testing, including to implement guides for additional scenario variables, and the Stress Testing Policy Statement. The proposal would also codify an enhanced disclosure process under which the Board would annually publish comprehensive documentation on the stress test models, invite public comment on any material changes that the Board seeks to make to those models, and annually publish the stress test scenarios for comment. Lastly, the proposal would make changes to the FR Y-14A/Q/M to remove items that are no longer needed to conduct the supervisory stress test and to collect additional data to support the stress test models and improve risk capture.

DATES:

Comments must be received on or before January 22, 2026.

ADDRESSES:

You may submit comments, identified by Docket No. R-1873 and RIN 7100-AH05, by any of the following methods:

- Agency website: https://www.federalreserve.gov/apps/proposals/. Follow the instructions for submitting comments, including attachments. Preferred Method.

- Mail: Benjamin W. McDonough, Deputy Secretary, Board of Governors of the Federal Reserve System, 20th Street and Constitution Avenue NW, Washington, DC 20551.

- Hand Delivery/Courier: Same as mailing address.

- Other Means: publiccomments@frb.gov. You must include the docket number in the subject line of the message.

Comments received are subject to public disclosure. In general, comments received will be made available on the Board's website at https://www.federalreserve.gov/apps/proposals/ without change and will not be modified to remove personal or business information including confidential, contact, or other identifying information. Comments should not include any information such as confidential information that would be not appropriate for public disclosure. Public comments may also be viewed electronically or in person in Room M-4365A, 2001 C St. NW, Washington, DC 20551, between 9 a.m. and 5 p.m. during Federal business weekdays.

FOR FURTHER INFORMATION CONTACT:

Doriana Ruffino, Assistant Director, (202) 452-5235, Hillel Kipnis, Assistant Director, (202) 452-2924, John Simone, Lead Financial Institution Policy Analyst, (202) 245-4256, Ben Ranish, Principal Economist, (202) 973-6964, Nathan Palmer, Senior Economist, (202) 785-6089, and Theo Pistner, Financial Institution and Policy Analyst II, (202) 941-1825, Division of Supervision and Regulation; William Bassett, Senior Associate Director, (202) 736-5644, Bora Durdu, Deputy Associate Director, (202) 452-3755, Elena Afanasyeva, Principal Economist, (202) 736-1971, Levent Altinoglu, Principal Economist, (202) 721-4503, and Sam Jerow, Senior Financial Analyst, (202) 245-4299, Division of Financial Stability; Asad Kudiya, Associate General Counsel, (202) 360-6887, Julie Anthony, Senior Special Counsel, (202) 658-9400, Jonah Kind, Senior Counsel, (202) 452-2045, Brian Kesten, Senior Counsel, (202) 843-4079, Katherine Di Lucido, Senior Attorney, (202) 253-5994, Legal Division. Board of Governors of the Federal Reserve System, 20th Street and Constitution Avenue NW, Washington, DC 20551. For users of TDD-TYY, please call 711 from any telephone, anywhere in the United States.

SUPPLEMENTARY INFORMATION:

Table of Contents

I. Introduction

II. Background on Stress Testing Framework, Stress Test Models, and Scenario Design Framework

A. Stress Testing Framework

B. Prior Supervisory Stress Disclosures and Policy Statements

C. Supervisory Stress Test Modeling Framework

D. Stress Test Models

E. Summary of the Proposal

F. Purpose of the Proposal

III. Overview of the Stress Test Modeling Framework

A. Supervisory Stress Test Models

B. Supervisory Stress Test Scenarios

C. Data Used in Stress Testing

IV. Enhanced Disclosure Process

A. Annual Disclosure of Models

B. Model Changes

C. Material Model Changes

D. Annual Disclosure of Scenarios

E. Stress Capital Buffer Requirement Reconsideration Process

V. Revisions to the Stress Testing Policy Statement

A. Future Supervisory Stress Test Results Disclosures

B. Other Revisions to the Stress Testing Policy Statement

VI. Other Revisions to the Stress Testing and Capital Plan Rules

A. Stress Test Jump-Off Date Change

B. Global Market Shock Date

C. Amendment to the Dividend Add-On Component Calculation

VII. Revisions to the FR Y-14A/Q/M

VIII. Proposed Changes to the Stress Test Modeling Framework

A. Proposed Changes to Stress Test Models

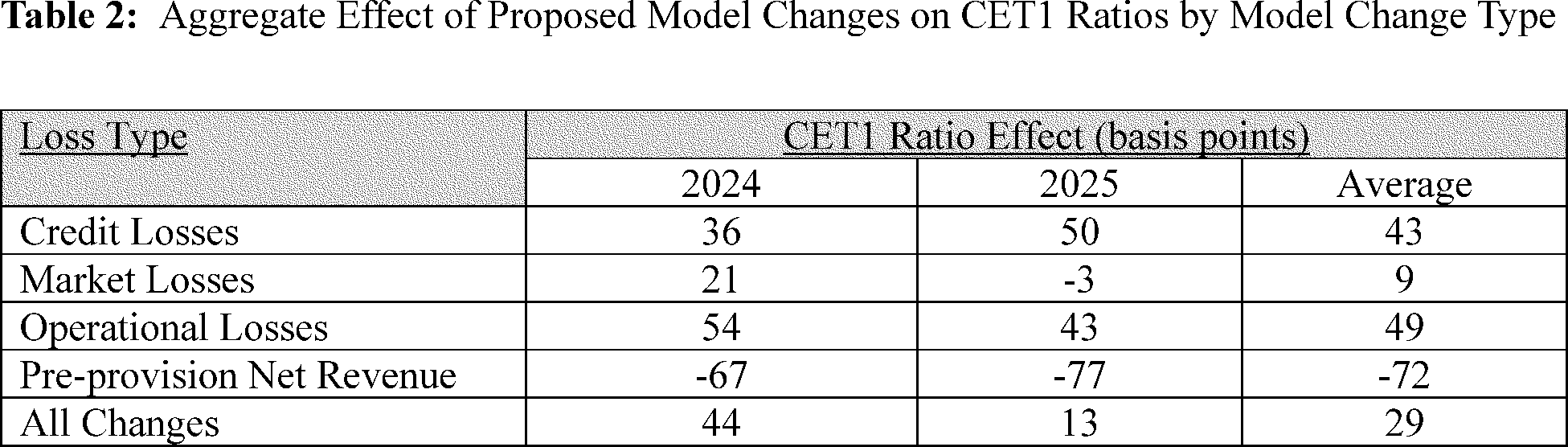

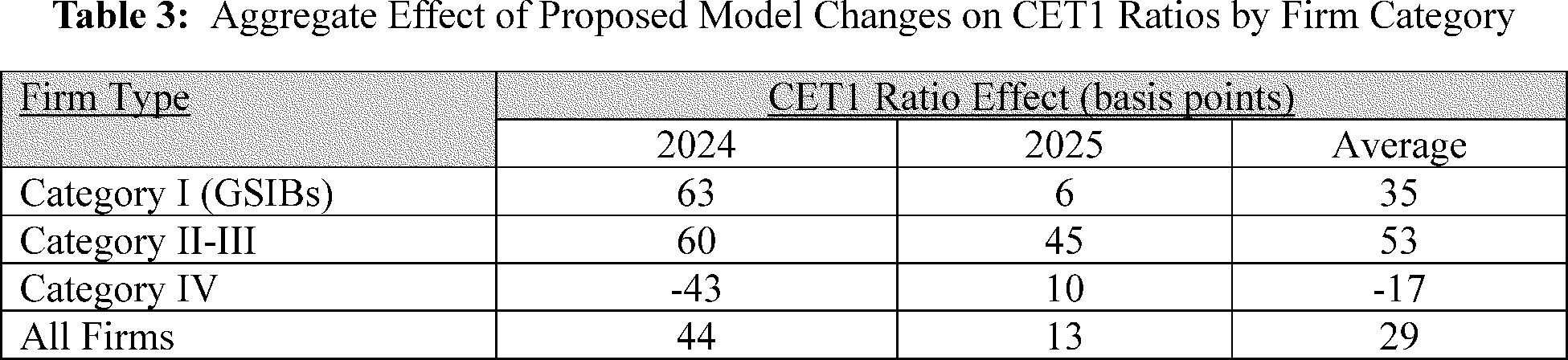

B. Analysis of Proposed Model Changes

IX. Proposed Changes to the Scenario Design Policy Statement

A. Changes to the Background and Overview and Scope Sections

B. Changes to the Content of the Stress Test Scenarios Section

C. Approach for Formulating Macroeconomic Assumptions in the Baseline Scenario

D. Scenario Narrative: Refinement to the Recession Approach

E. Changes to Construction of Certain Variables in the Severely Adverse Scenario

F. Scenario Design Principles Derived From Stress Testing Literature: Severity, Credibility, and Procyclicality

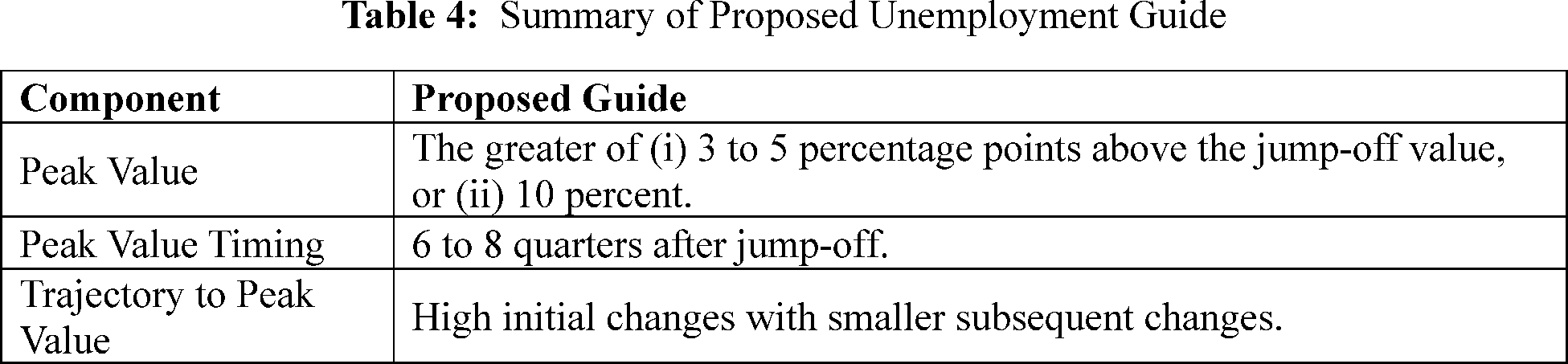

G. Description of Variable Guides in the Severely Adverse Scenario

H. Global Market Shock

X. Economic Analysis

XI. Administrative Law Matters

A. Paperwork Reduction Act Analysis

B. Regulatory Flexibility Act Analysis

C. Plain Language

D. Providing Accountability Through Transparency Act of 2023

I. Introduction

In December 2024, the Board announced that it would propose significant changes to improve the transparency of the supervisory stress test and reduce the volatility of resulting capital requirements.[1] The Board noted it planned to propose changes to disclose and seek public comment on the models that determine the ( printed page 51857) hypothetical losses and revenue of banks under stress and ensure that the public can comment on the hypothetical scenarios used annually for the test, before the scenarios are finalized. With this proposal, the Board is inviting public comment on the comprehensive model documentation for the 2026 stress test, as well as proposed changes to the models relative to the 2025 stress test. The comprehensive model documentation is available at https://www.federalreserve.gov/supervisionreg/dfa-stress-tests-2026.htm. The Board is inviting comment on the proposed scenarios for the 2026 stress test through a separate notice.

This proposal seeks to improve the transparency and public accountability of the supervisory stress test, while ensuring that the stress test remains an effective tool for understanding and assessing risk and retaining appropriate risk sensitivity and risk capture in capital requirements.

The Board periodically reviews its regulations, including transparency efforts surrounding its regulations, to ensure they continue to achieve their goals in an effective and efficient manner. In addition to the changes discussed herein, the Board is also considering the effectiveness of its regulatory capital and capital planning requirements for large firms to ensure they remain cohesive and effective, maintain the resilience of the banking sector, and minimize any unnecessary burden. If appropriate, the Board will make changes to its rules through the public notice and comment process.

Question 1: The Board seeks comment on all aspects of the proposal. What, if any, other elements of the supervisory stress test framework should the Board consider amending to improve the transparency, public accountability, and effectiveness of the supervisory stress test? For example, the Board could instead transliterate the models used to conduct the stress test and codify these transliterations in its regulations. What would be the advantages and disadvantages of this approach or other approaches the Board could consider?

II. Background on Stress Testing Framework, Stress Test Models, and Scenario Design Framework

A. Stress Testing Framework

Congress enacted the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) in the wake of the 2007-09 financial crisis.[2] Section 165 of the Dodd-Frank Act, as amended by section 401 of the Economic Growth, Regulatory Relief, and Consumer Protection Act,[3] requires the Board to establish enhanced prudential standards for nonbank financial companies supervised by the Board and bank holding companies with $250 billion or more in total consolidated assets.[4] The purpose of these enhanced prudential standards is to prevent or mitigate risks to the financial stability of the United States that could arise from the material financial distress or failure, or ongoing activities, of large, interconnected financial institutions.

Section 165(i)(1) of the Dodd-Frank Act requires the Board to conduct an annual supervisory stress test of nonbank financial companies supervised by the Board and bank holding companies with $250 billion or more in total consolidated assets to evaluate whether the firm has the capital, on a total consolidated basis, necessary to absorb losses as a result of adverse economic conditions.[5] Section 401(e) of the Economic Growth, Regulatory Relief, and Consumer Protection Act requires the Board to conduct periodic stress tests for bank holding companies with total consolidated assets between $100 billion and $250 billion.[6] Section 165(i)(1) of the Dodd-Frank Act requires the Board to publish a summary of the supervisory stress test results.[7] In 2012, the Board adopted a final rule implementing the stress test requirements established in the Dodd-Frank Act.[8]

The Dodd-Frank Act also requires bank holding companies with $250 billion or more in total consolidated assets, as well as nonbank financial companies supervised by the Board, to conduct company-run stress tests on a periodic basis.[9] Under the Board's rules, firms subject to Category I, II, or III standards must conduct company-run stress tests.[10] Company-run stress tests provide forward-looking information to supervisors to assist in their overall assessments of a firm's capital adequacy, help to better identify downside risks and the potential impact of adverse outcomes on the firm`s capital adequacy, and assist in achieving the financial stability goals of the Dodd-Frank Act. Further, the company-run stress tests help improve firms' stress testing practices with respect to their own internal assessments of capital adequacy and overall capital planning.

Each June, the Board publishes the results of its annual supervisory stress test, including each firm's projected capital ratios, pre-tax net income, losses, revenues, and expenses, under hypothetical, severely adverse economic and financial conditions.[11] These disclosures provide the public with valuable information about each firm's financial condition and the ability of ( printed page 51858) each firm to absorb losses considering a stressful economic environment.

Following the 2007-09 financial crisis, the Board also made changes to its capital rule to address weaknesses observed during the crisis.[12] These changes included the establishment of a minimum common equity tier 1 capital requirement and a fixed capital conservation buffer equal to 2.5 percent of risk-weighted assets.[13] Large firms also became subject to a countercyclical capital buffer requirement, and the largest and most systemically important firms—global systemically important bank holding companies, or GSIBs—became subject to an additional capital buffer based on a measure of their systemic risk, the GSIB surcharge.[14] In 2020, the Board adopted the stress capital buffer requirement for certain firms.[15] Because a firm's stress capital buffer requirement is informed by the firm's performance under the hypothetical economic conditions modeled by the supervisory stress test, each firm's stress capital buffer requirement is tailored to its risk profile.

Supervisory stress testing and stronger capital requirements have significantly improved the resilience of the U.S. banking system. Since 2009, the common equity capital ratios of firms subject to the test have more than doubled, with common equity capital of such firms increasing by over $1 trillion.[16] Since 2020, the supervisory stress test results have also informed a firm's stress capital buffer requirement. Greater transparency would allow firms to better understand the capital requirements associated with investment and expansion of different business lines and would facilitate more effective long-term capital planning. This, in turn, could enhance firms' ability to supply credit to households and businesses, ultimately supporting economic growth and financial stability.

B. Prior Supervisory Stress Disclosures and Policy Statements

In addition to the annual stress test results disclosure, the Board has historically published some information about the supervisory stress test scenarios and models.

Scenarios

The Board's stress test rules provide that the Board will notify firms, by no later than February 15 of each year, of the scenarios that the Board will apply to conduct its annual supervisory stress test and that firms must use to conduct their company-run stress tests.[17] The Board also provides a narrative description of the scenarios no later than February 15 of each calendar year.[18]

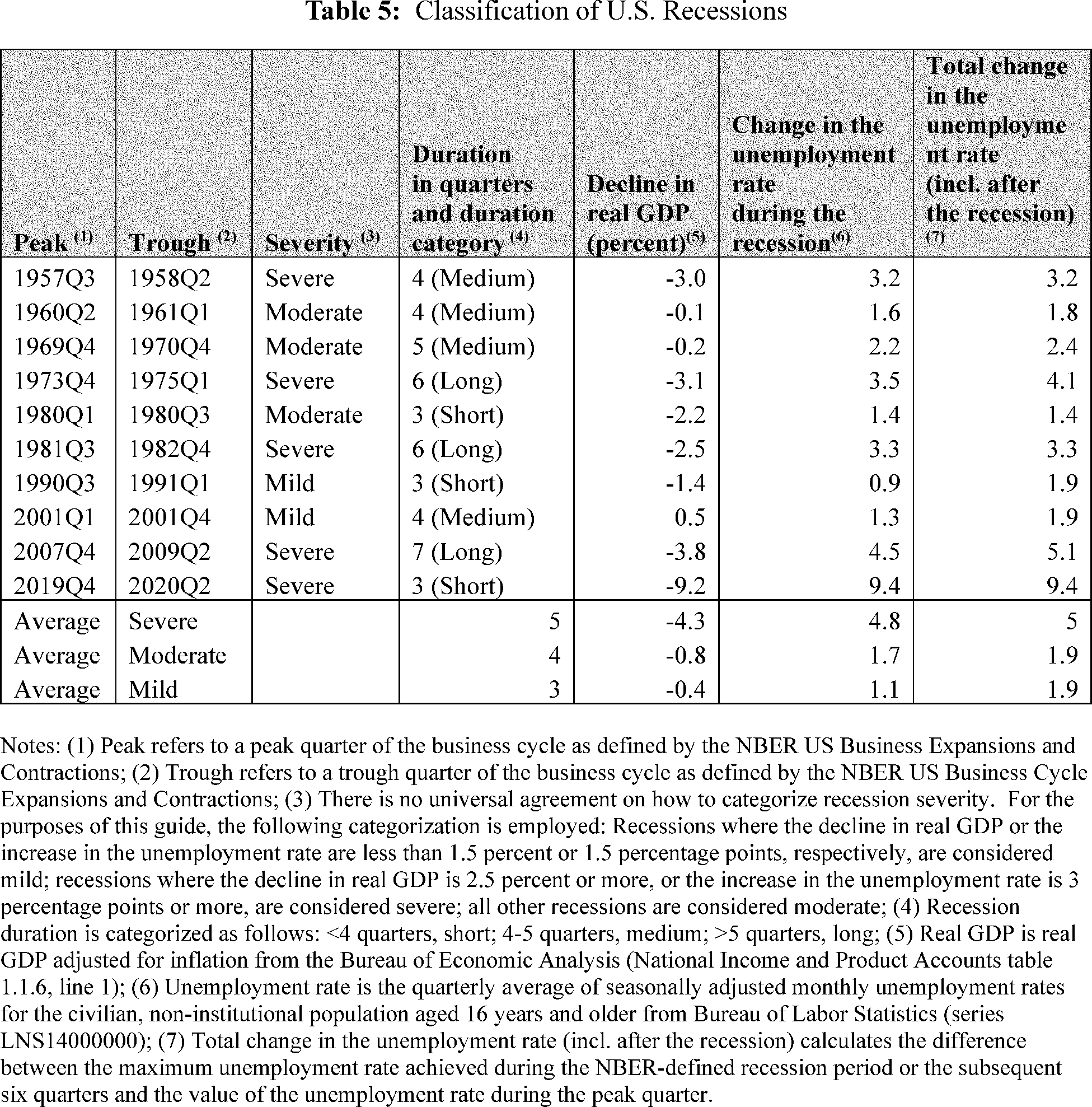

In 2013, the Board increased the transparency of the scenarios by finalizing the Policy Statement on the Scenario Design Framework for Stress Testing (Scenario Design Policy Statement), which articulated the Board's approach to scenario design for the supervisory and company-run stress tests, outlining the characteristics of the stress test scenarios, and explaining the considerations and procedures that underlie the formulation of these scenarios.[19] The Scenario Design Policy Statement also described the baseline and severely adverse scenarios, the Board's approach for developing these two macroeconomic scenarios, and the approach for developing any additional components of the stress test scenarios. The Scenario Design Policy Statement explained that the severely adverse scenario is designed to reflect conditions that have characterized post-war U.S. recessions (the recession approach). Historically, recessions have typically featured increases in the unemployment rate, contractions in aggregate incomes and economic activity, and declines in inflation and interest rates.

In the 2013 Scenario Design Policy Statement, the Board explained that, in light of the typical co-movement of measures of economic activity during economic downturns, such as the unemployment rate and gross domestic product, the Board would first specify a path for the unemployment rate and then develops paths for other measures of activity broadly consistent with the course of the unemployment rate in developing the severely adverse scenario. The 2013 Scenario Design Policy Statement also stated that economic variables included in the scenarios may change over time, and that the Board may augment the recession approach with certain salient risks, which would involve incorporating features that address aspects of the current economic or financial market environment that represent higher-than-normal risks to the condition of the banking system.

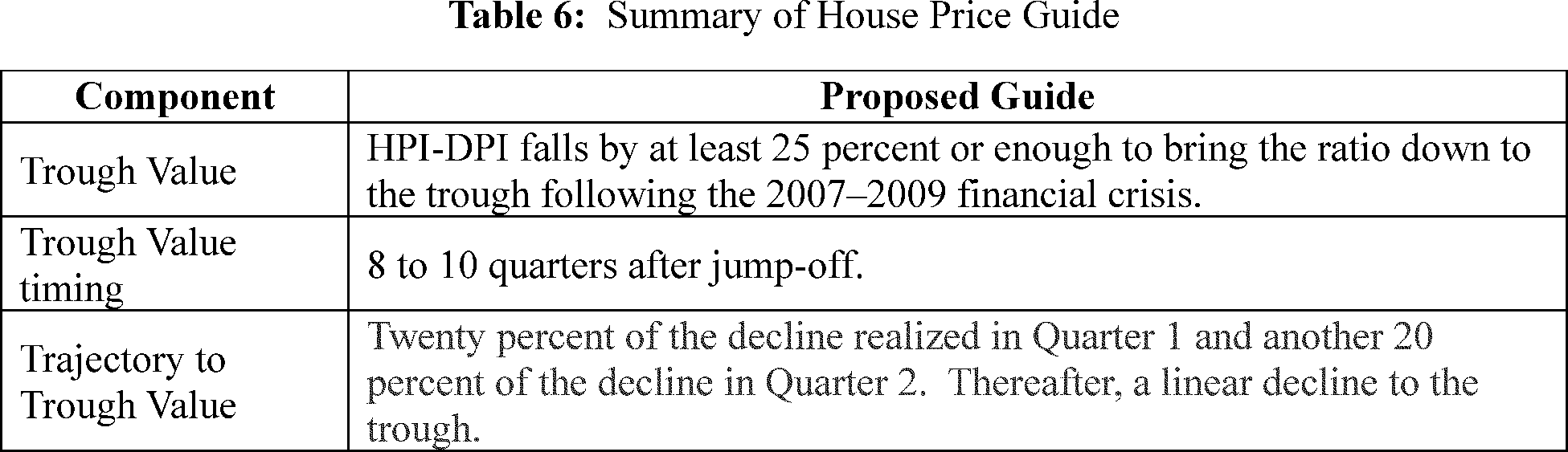

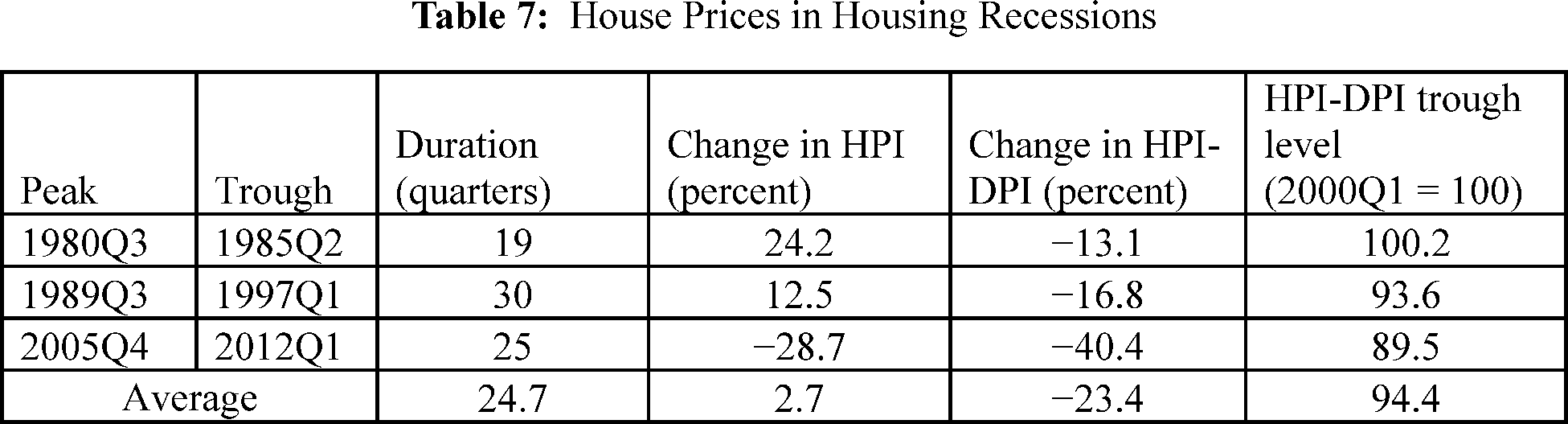

In 2019, the Board updated the Scenario Design Policy Statement, which increased the transparency and predictability of the scenarios by allowing for a smaller-than-usual increase in unemployment if the stress test were to occur during an economic downturn, a change that would pass through to reduced severity of other key scenario variables due to the deference given to historical correlations. The 2019 update also introduced a formula with countercyclical features to guide the evolution of the ratio of housing prices to disposable income in the scenario, which provided more predictability in the way that the stress test would treat business lines affected by changes in house prices. However, the Board believes that the design of scenarios could be made more transparent and predictable by providing additional guides for certain macroeconomic variables, and by disclosing additional detailed information on the methodology used to create the global market shock component of the severely adverse scenario, as described below.

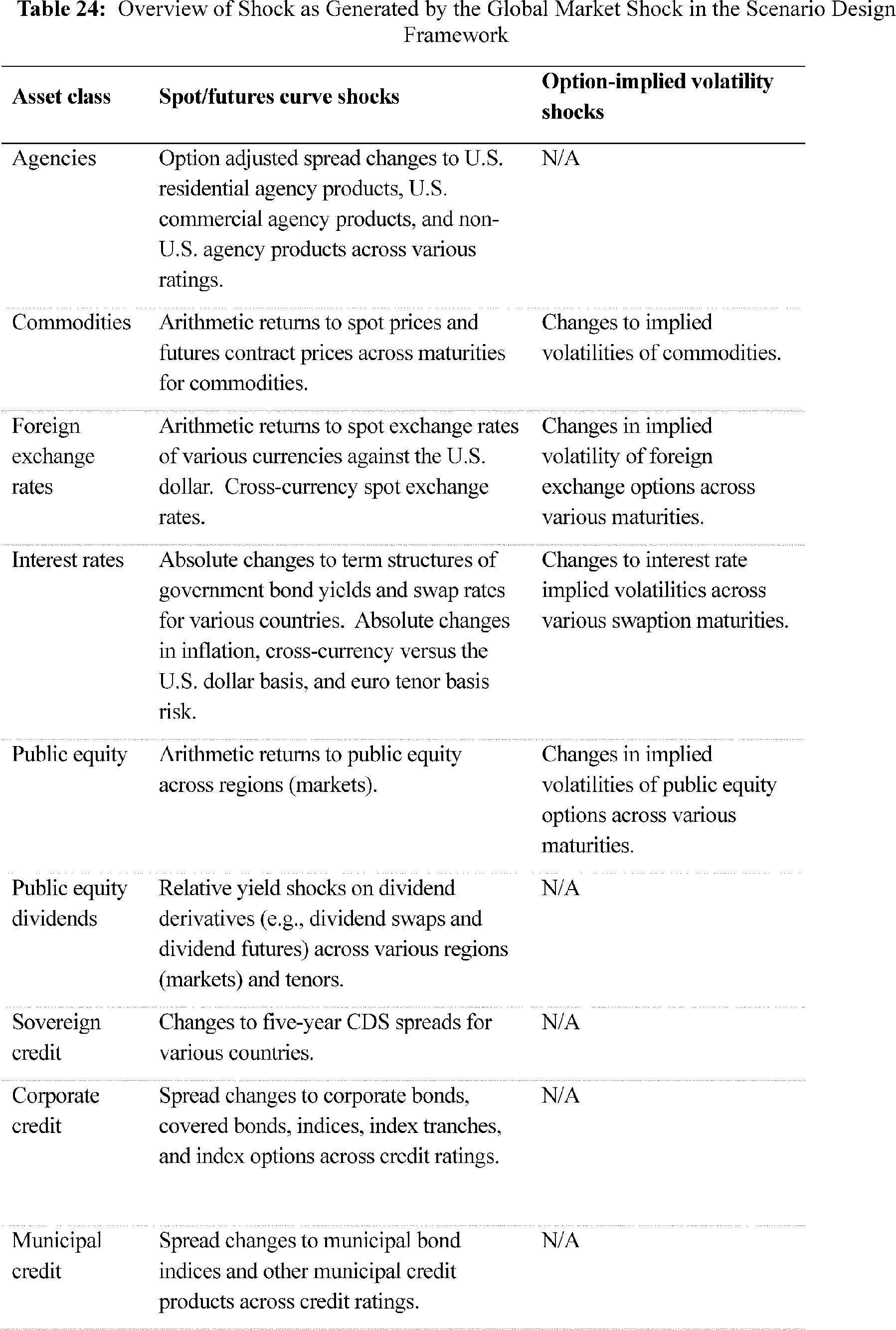

a. Trading and Counterparty Components

For a subset of firms, the severely adverse scenario also includes two additional components: the global market shock component and the largest counterparty default component.[20] The global market shock component is a set of hypothetical shocks to a large set of risk factors reflecting general market distress and heightened uncertainty. A firm with significant trading activity must consider the global market shock component as part of its severely adverse scenario and recognize associated losses in the first quarter of the projection horizon.[21] The global ( printed page 51859) market shock component is applied to asset positions held by the firms on a given as-of date.[22] In addition, for certain large and highly interconnected firms, the same global market shock component is applied to counterparty exposures under the largest counterparty default component.[23] The largest counterparty default component is intended to assess the potential losses and capital impact associated with the default of the largest counterparty of each applicable firm, and the as-of date aligns with that of the global market shock component.

The design and specification of the global market shock component differs from the design and specification of the severely adverse scenario in several respects. First, in alignment with U.S. generally accepted accounting principles (U.S. GAAP), profits and losses from trading and counterparty credit positions are measured in mark-to-market accounting terms in the global market shock, while revenues and losses from traditional banking activities, as generated under macroeconomic scenarios, are generally measured using the accrual accounting method. Second, the timing of loss recognition differs between the global market shock and the severely adverse macroeconomic scenario. The global market shock affects the mark-to-market value of trading positions and counterparty credit losses in the first quarter of the severely adverse scenario. This timing is based on an observation that market dislocations can happen rapidly and unpredictably at any time under stressed conditions. In addition, the severely adverse scenario is applied as of December 31 of each year (the jump-off date), whereas the global market shock as-of date changes every year (within the window specified in the Board's stress test rules) and does not necessarily coincide with the year-end. This timing is also based on a scenario assumption that market dislocations can happen rapidly and unpredictably at any time during the scenario horizon. Recognizing the global market shock in the first quarter helps ensure that potential losses from trading and counterparty exposures are incorporated into firms' capital ratios in each quarter of the severely adverse scenario.

Models

Prior to 2019, the annual stress test results disclosure document contained an appendix describing the Board's supervisory stress test models.[24] In 2019, the Board increased the transparency of the supervisory stress test models by finalizing the Stress Testing Policy Statement [25] and the Enhanced Disclosure of the Models Used in the Federal Reserve's Supervisory Stress Test (Enhanced Model Disclosure).[26] The Stress Testing Policy Statement describes the Board's policies and procedures that guide the development, implementation, and validation of the models.[27] The Stress Testing Policy Statement also describes the Board's principles for stress test model design, namely that the system of models used in the supervisory stress test should result in projections that are (1) independent of firm projections; (2) forward-looking in that they project future losses and revenue; (3) consistent and comparable across firms; (4) generated from simple approaches, where appropriate; (5) robust and stable; (6) conservative; and (7) able to capture the effect of severe economic stress. The Board has developed stress test models in accordance with these principles, which are the foundation for the stress test modeling decisions described in the comprehensive documentation of the supervisory stress test models that the Board is publishing in conjunction with this proposal.

The Enhanced Model Disclosure supplemented prior public descriptions of the stress test models by providing some information about their structure and by including a list of key variables that influence the results of each model.[28] However, the Board believes more detailed information, beyond what is in the current Enhanced Model Disclosure, would improve the ability of firms to accurately assess how changes in their business activities might impact their supervisory stress test results and, relatedly, their stress capital buffer requirements and overall capital requirements.

C. Supervisory Stress Test Modeling Framework

The Board's stress test models take macroeconomic variables from the Board's severely adverse scenario and firm data as inputs to produce each firm's projected capital ratios over a nine-quarter horizon. The projected common equity tier 1 capital ratio is used to inform each firm's stress capital buffer requirement, which becomes part of a firm's capital conservation buffer.

The stress test models are intended to capture how a firm's regulatory capital would be affected by the macroeconomic and financial conditions described in the stress test scenarios, given the characteristics of the firm's business model and balance sheet composition. The Board uses a variety of statistical modeling techniques to produce the stress test results, including multivariate regression, which uses relationships in historical data to produce projections of a variable (such as a loss given default). These models are represented by a set of formulas and coefficients that produce the projections.

The Board estimates the effect of the severely adverse scenario on the regulatory capital ratios of firms by projecting revenues, expenses, and losses for each firm over a nine-quarter projection horizon (projection horizon). The projection horizon spans nine quarters to ensure that the firms can continue to provide credit and serve as financial intermediaries despite several quarters of adverse economic conditions, as well as to promote the forward-looking nature of capital planning by firms.

Projected net income, adjusted for the effect of taxes, is combined with assumptions regarding capital actions and other changes to regulatory capital to produce post-stress capital ratios. The Board's approach to modeling supervisory stress test results, including the calculation of post-stress capital ratios, is generally in alignment with U.S. GAAP and the regulatory capital framework.[29] However, the stress test models may deviate from U.S. GAAP and the regulatory capital framework, as circumstances warrant.

The Board established the Stress Testing Policy Statement modeling principles to ensure that the models are well suited for their purpose in the regulatory framework. In some cases, the Board's adherence to the principles limits modeling choices and results in certain common limitations across similarly constructed component ( printed page 51860) models. For instance, consistent with the principles of independence, consistency and comparability, and simplicity, models are not designed to capture all firm-specific nuances, future strategic initiatives, or planned capital actions. Additionally, models may be limited by their reliance on historic relationships and by the nature of the data captured in firms' regulatory reports. Detailed assumptions and limitations for the models are discussed in the comprehensive documentation, which is available at https://www.federalreserve.gov/supervisionreg/dfa-stress-tests-2026.htm.

Under the Stress Testing Policy Statement, the Board's projections also assume that a firm's balance sheet remains unchanged throughout the projection horizon.[30] This assumption seeks to help ensure that a firm cannot “shrink to health” and that it remains sufficiently capitalized to accommodate credit demand in a severe downturn.

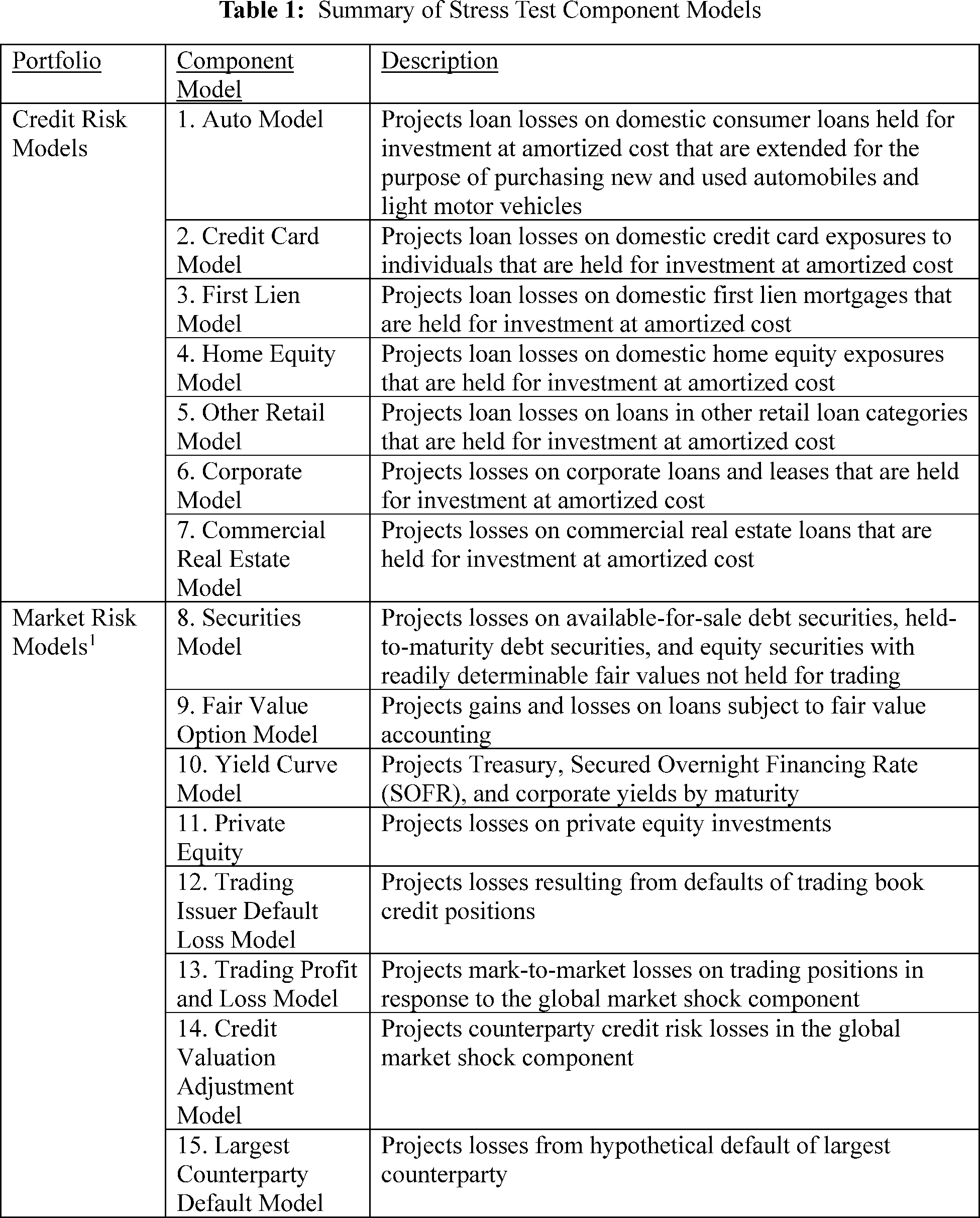

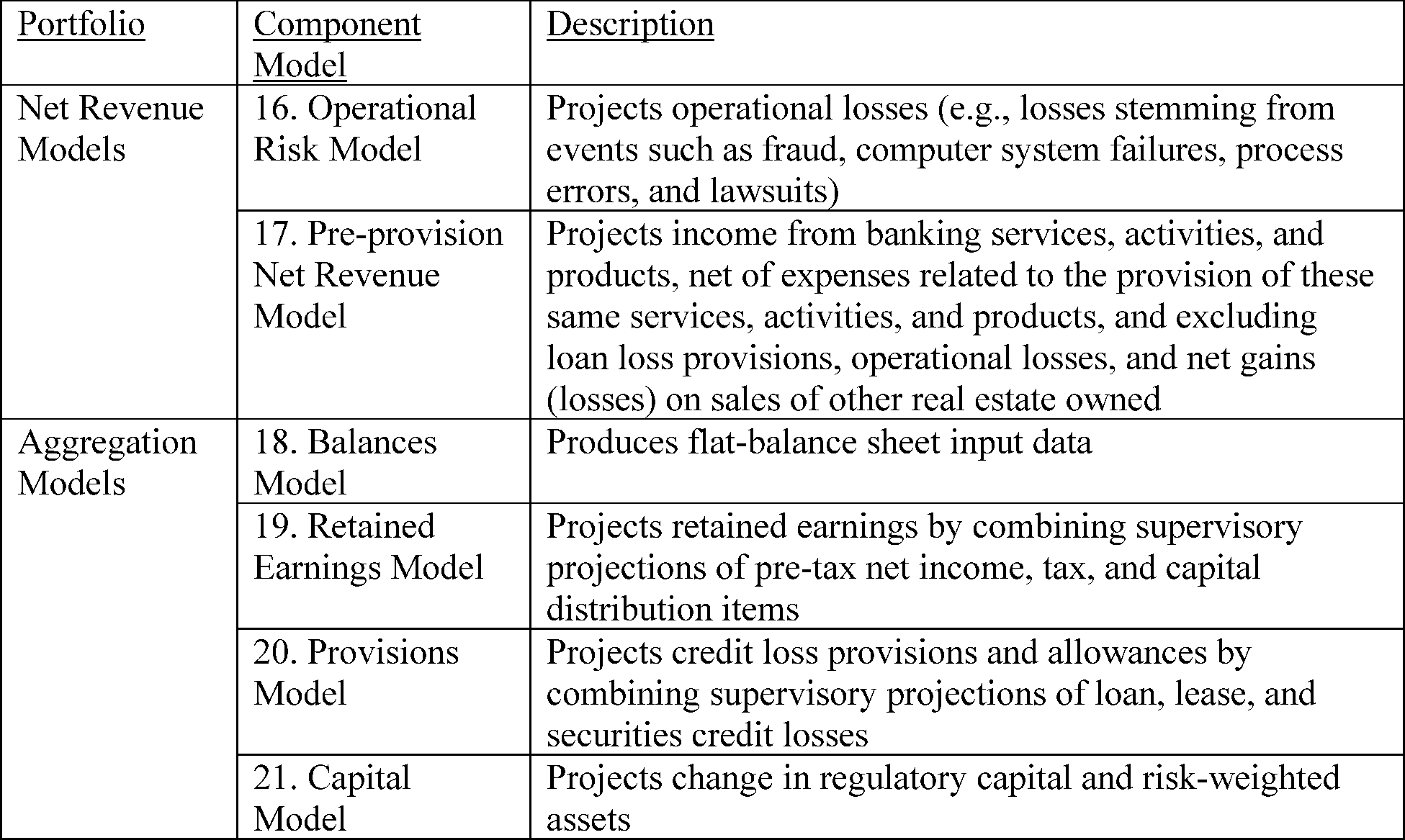

D. Stress Test Models

The Board's stress test models comprise twenty-one component models that, when aggregated, produce projected regulatory capital ratios for each firm (see Table 1 below). The models can be grouped into four categories: credit risk, market risk, net revenue, and aggregation. Credit risk models capture losses associated with retail and wholesale loans that are held at amortized cost. Market risk models capture losses associated with trading and counterparty exposures, securities, and other assets held at fair value. Net revenue models capture income and expenses, including those related to operational risk, earned or incurred by a firm. Positive pre-provision net revenue offsets credit and market risk losses in the calculation of a firm's pre-tax net income. Aggregation models calculate a firm's pre-tax net income, which is then adjusted for other elements such as taxes and regulatory capital deductions to arrive at the projection of a firm's regulatory capital, which is used to calculate a firm's projected capital ratios. Additional detail about these component models is provided in Section III.A of this Supplementary Information and the comprehensive model documentation available at https://www.federalreserve.gov/supervisionreg/dfa-stress-tests-2026.htm.[31]

( printed page 51861) ( printed page 51862){kind=link}

{kind=link}

E. Summary of the Proposal

The Board is publishing comprehensive documentation on the stress test models on the Board's website, at https://www.federalreserve.gov/supervisionreg/dfa-stress-tests-2026.htm. This model documentation contains information on the models that together produce the results of the supervisory stress test. The model documentation includes the equations, variables, and coefficients used in each model (where applicable); assumptions and limitations of each model; rationales for modeling decisions; and discussions of alternative models. Section VIII.A of this Supplementary Information summarizes changes to the models, relative to the 2025 stress test, that the Board plans to implement in the 2026 stress test cycle; section VIII.B of this Supplementary Information contains an analysis of the potential effects of these proposed model changes. Detailed documentation on these changes is also provided on the Board's website, at https://www.federalreserve.gov/supervisionreg/dfa-stress-tests-2026.htm. As part of this proposal, the Board is inviting public comment on the stress test models and these changes.

In addition, the Board is proposing to codify an enhanced disclosure process that would build on the previous efforts that the Board has made to increase the transparency and public accountability of the supervisory stress test. Under this enhanced disclosure process, the Board would annually publish comprehensive model documentation on the stress test models, invite public comment on any material changes that the Board seeks to make to those models, and annually publish the stress test scenarios for comment. The Board would also commit to responding to substantive public comments on any material model changes before implementing them. The proposal would revise the Stress Testing Policy Statement to align with this enhanced disclosure process, as well as to amend the Board's general policy related to disclosing additional information directly to a firm about that firm's supervisory stress test results. To accommodate the annual comment process on the scenarios, the proposal would shift the jump-off date of the supervisory and company-run stress tests from December 31 to September 30.

Additionally, this proposal would amend the Scenario Design Policy Statement in several ways. The Board would include in the Scenario Design Policy Statement detailed descriptions of additional guides that are used to inform the Board's choice of the values of the scenario variables along their scenario paths. The guides are designed to balance the competing objectives of predictability and transparency, on the one hand, with the severity and relevance of the macroeconomic and financial market scenarios, on the other hand. Most of the proposed guides also incorporate features similar to the range of options in the existing unemployment guide or the automatic adjustment of the house price path to current housing market conditions in the existing house price guide. This approach would allow the Board to continue to adjust the severity of those variables as necessary to avoid inducing greater procyclicality in the financial system and macroeconomy.

Similarly, the Board is proposing to incorporate additional information into the Scenario Design Policy Statement about the framework used to create the global market shock component of the severely adverse scenario. This information includes, but is not limited to, details on the logic underlying the severity of the shocks and a description of the processes used to generate the shock values. The Board is also proposing to update the global market shock methodology to simplify the scenario and better align certain elements of the global market shock with the nature of an “instantaneous” shock. The proposal would also make revisions to the stress test rules to improve the risk capture of the supervisory stress test by widening the ( printed page 51863) as-of date window for the global market shock.

Finally, the proposal would make changes to the FR Y-14A/Q/M reports to remove items and documentation requirements that are no longer needed to conduct the supervisory stress test, as well as to collect additional data to improve risk capture.

F. Purpose of the Proposal

The purpose of this proposal is to provide the public with more information about the stress test models and scenarios and to help ensure that the public has an opportunity to comment on the models and scenarios. While the Board has increased the transparency of the stress test models over time, disclosing additional information about the stress test models and their underlying methodologies will further increase transparency and improve public accountability.

Publishing detailed descriptions of the stress test models for comment, as well as committing to future enhanced disclosures, has benefits. First, the increase in transparency would increase public accountability and instill confidence in the fairness of the supervisory stress tests. Second, the disclosure process would create a new mechanism for obtaining feedback from the public, including academics, financial analysts, and firms, on the design and specifications of the models, which should lead to model improvements. Third, a firm would have a better sense of how its risk profile would factor into its stress capital buffer requirement, which would reduce the likelihood of unanticipated stress test results and allow for better capital and business planning by firms. Finally, the public disclosure of additional information about supervisory stress tests should strengthen market discipline, because investors, counterparties, and rating agencies would be able to better assess a firm's risk profile.[33] The costs and benefits of this proposal are described more thoroughly in Section X of this Supplementary Information.

With respect to the proposed amendments to the Scenario Design Policy Statement, this proposal also builds on the contents of the current Scenario Design Policy Statement and would amend it to provide additional transparency, public accountability, and predictability in the variable paths. The changes would support the Board in developing scenarios, inviting comment on those scenarios, incorporating input from commenters, and maintaining the current schedule for release of the final scenarios. Despite the increased predictability in the scenarios, the new framework would remain flexible enough to suitably assess whether firms can maintain an adequate amount of loss-absorbing capital to stay above minimum regulatory requirements and continue financial intermediation during periods of stress, as well as adjust features that might add to existing procyclicality in the financial system, as appropriate. In practice, the scenarios resulting from the revised framework are expected to remain consistent with the current Scenario Design Policy Statement and should not result, on average over a typical business cycle, in materially different scenarios than would have been designed previously.

Additionally, the proposal would simplify the design of the global market shock component and incorporate additional information on the development process into the Scenario Design Policy Statement, which outlines the Board's approaches to designing market shocks, including important considerations for scenario design, possible approaches to developing scenarios, and a development strategy for implementing the preferred approach. Taken together, these changes would improve transparency, public accountability, and predictability of the supervisory scenarios, while ensuring the supervisory stress test's ability to capture changes in the risks in the financial industry over time.

III. Overview of the Stress Test Modeling Framework

As summarized in Section II.D of this Supplementary Information, the Board estimates the effect of the scenarios on the regulatory capital ratios of firms participating in the stress test by projecting net income and other components of regulatory capital for each firm over a nine-quarter projection horizon. To do so, the Board uses twenty-one component models, the macroeconomic variables from the Board's severely adverse scenario, and firm data. This section provides an overview of the component models the Board used to run the 2025 supervisory stress test. See Table 1 in Section II.D of this Supplementary Information.

A. Supervisory Stress Test Models

The Board calculates projected pre-tax net income by combining projections of pre-provision net revenue,[34] provisions for credit losses,[35] and other gains or losses.[36] Each component of pre-tax net income is described below.

Pre-Provision Net Revenue

Pre-provision net revenue is defined as net interest income (interest income minus interest expense) plus noninterest income minus noninterest expense. Consistent with U.S. GAAP, these projections include projected losses due to operational risk events and expenses related to the disposition of other real estate owned.[37] The Board projects most components of pre-provision net revenue using models that relate specific revenue and non-provision-related expenses to the characteristics of firms and to macroeconomic variables. These include eight components of interest income, seven components of interest expense, six components of noninterest income, and three components of noninterest expense. The Board separately projects losses from operational risk and other real estate owned expenses. Operational risk is defined as “the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events.” [38] Other real estate owned expenses are expenses related to the disposition of real estate owned properties and stem from losses on first-lien mortgages.

Loan Losses and Provisions on Loans Measured at Amortized Cost

The Board typically projects losses using one of two modeling approaches: the expected-loss approach or the net charge-off approach. Generally, under the expected loss approach, expected losses are estimated by projecting the probability of default, loss given default, and exposure at default for each quarter of the projection horizon. Expected losses in each quarter are the product of these three components. Under the net ( printed page 51864) charge-off approach, losses are projected using historical behavior of net charge-offs as a function of macroeconomic and financial market conditions and loan portfolio characteristics.[39]

The Board estimates losses for loans measured at amortized cost separately for different categories of loans, based on the type of obligor, collateral, and loan structure. The individual loan types modeled can broadly be divided into (1) retail loans, including various types of residential mortgages, credit cards, student loans, auto loans, small business loans, and other consumer loans; and (2) wholesale loans, such as commercial and industrial loans and commercial real estate loans. For most loan types, losses in quarter t are estimated as the product of the projected probability of default in quarter t, the loss given default in quarter t, and exposure at default in quarter t.

The probability of default component measures the likelihood that a borrower enters default status during a given quarter t. The other two components capture the lender's net loss on the loan if the borrower enters default. The loss given default component measures the percentage of the loan balance that the lender will not be able to recover after the borrower enters default, and the exposure at default component measures the total expected outstanding loan balance at the time of default.[40]

The Board's definition of default, for stress test modeling purposes, may vary for different types of loans and may differ from general industry definitions or classifications. The Board generally models probability of default as a function of loan characteristics and economic conditions. The Board typically models loss given default based on historical data, and modeling approaches vary for different types of loans. For certain loan types, the Board models loss given default as a function of borrower, collateral, or loan characteristics and the macroeconomic variables from the supervisory scenarios. For other loan types, the Board assumes loss given default is a fixed percentage of the loan balance for all loans in a category. The approach to modeling exposure at default also varies by loan type and depends on whether the loan is a term loan or a line of credit.

For certain retail loan categories, projections capture the historical behavior of net charge-offs as a function of macroeconomic and financial market conditions and loan portfolio characteristics. The Board then uses these stress test models to project future charge-offs consistent with the evolution of macroeconomic conditions under the severely adverse scenario. To project losses, the projected net charge-off rate is applied to projected loan balances.

Losses on loans are then projected to flow into net income through provisions for loan and lease losses (for simplicity, provisions for loan losses). Provisions for loan losses reflect funds set aside to cover loan losses that a firm expects to incur in a predetermined future window. Provisions for loan losses feed into the allowance for loan losses, which serves as a contra asset on a firm's balance sheet. The charged-off amount of a loan reduces the outstanding balance of the loan while also reducing the allowance for loan losses (that is, charge-offs do not reduce a firm's total assets). Generally, provisions for loan losses for each projected quarter in the supervisory stress test equal projected losses on loans for the quarter plus the change in the allowance for loan losses needed to cover the subsequent four quarters of expected loan losses. This calculation incorporates the allowance for loan losses established by the firm as of the jump-off date of the stress test exercise.

Current Expected Credit Losses Framework

On January 1, 2020, most large and mid-sized U.S. banks adopted the Current Expected Credit Losses (CECL) standard for calculating allowances.[41] CECL superseded the incurred loss accounting standard, which was a backward-looking measure that enabled firms to calculate allowances based on historical loss data and current economic conditions. CECL, by contrast, is a forward-looking measure that requires firms to estimate lifetime losses based on reasonable estimates of future economic conditions. In October 2024, the Board announced that it would continue to evaluate future enhancements to the supervisory stress test approach for the incorporation of CECL.[42]

The Board is not proposing to implement CECL into the supervisory stress testing framework as a part of this proposal. The allowance calculation framework currently used in the supervisory stress test is already forward-looking: it projects loan loss provisions four quarters ahead. This approach aligns with the Board's modeling principle of simplicity as it requires fewer assumptions than would be required to determine provisions under CECL. In addition, in aggregate, the cumulative loan loss provisions under the supervisory severely adverse scenario are similar to provision projections submitted by the firms that have adopted CECL. Should the Board decide to implement CECL into the supervisory stress testing framework, it would seek public comment prior to implementation, as it would likely be a material model change as defined in this proposal.

Question 2: What factors should the Board consider when determining whether to implement CECL into the supervisory stress testing framework and why?

Question 3: What would be the advantages and disadvantages of incorporating CECL into the supervisory stress testing framework?

Losses on Loans Measured on a Fair Value Basis

Certain loans are accounted for on a fair value basis instead of on an amortized cost basis. If a loan is accounted for using the fair value option, it is marked to market, and the accounting value of the loan changes as a function of changes in market risk factors and fundamentals. Similarly, loans that are held for sale are accounted for at the lower of cost or market value. The stress test models for these asset classes project gains and losses over the nine-quarter projection horizon, net of any hedges, using the scenario-specific path of interest rates and credit spreads. The Board uses different models to estimate gains and losses on wholesale loans and retail loans that are accounted for on a fair value basis since these loans have different risk characteristics. However, these models all generally project gains and losses over the nine-quarter projection horizon, net of hedges, by applying the scenario-specific interest rate and credit spread shocks to loan yields.

Losses on Securities

A firm's balance sheet typically contains holdings of two types of securities related to investment activities: available-for-sale and held-to- ( printed page 51865) maturity. Available-for-sale and held-to-maturity securities are generally held at fair value and amortized cost, respectively, on a firm's balance sheet. The Board estimates two types of losses on securities related to investment activities.[43]

For debt securities classified as available-for-sale, projected fluctuations in the fair value of the securities due to changes in interest rates and other factors will result in unrealized gains or losses that are recognized in capital for some firms through other comprehensive income. Under U.S. GAAP, unrealized gains and losses on available-for-sale debt securities are reflected in accumulated other comprehensive income and do not flow through net income.[44] Under the regulatory capital rule, accumulated other comprehensive income must be incorporated into common equity tier 1 capital for certain firms. Unrealized gains and losses are calculated as the difference between each security's fair value and its amortized cost. The amortized cost of each available-for-sale debt security is equivalent to the purchase price of the debt security, which is periodically adjusted if the debt security was purchased at a price other than par or face value, has a principal repayment, or has an impairment recognized in earnings.[45]

Credit losses on available-for-sale and held-to-maturity securities may be also recorded. Except for certain government-backed obligations, both available-for-sale and held-to-maturity securities are at risk of incurring credit losses.[46] The stress test models project security-level credit losses, using as an input the projected fair value for each security over the nine-quarter projection horizon under the severely adverse scenario. Credit losses on securities are included in the projection of provisions.

Projected other comprehensive income gains or losses from available-for-sale debt securities are computed directly from the projected change in fair value, taking into account credit losses and applicable interest-rate hedges on securities. All debt securities held in the available-for-sale portfolio are subject to other comprehensive income losses.

Losses on Private Equity Exposures

The Board projects the value of private equity investments in response to the severely adverse scenario of the supervisory stress test.[47] The Private Equity Model assigns losses and recoveries based on changes in fair value, recognized in net income for all positions, regardless of their individual accounting elections. While U.S. GAAP allows for private equity to be carried under a variety of accounting measures, the different accounting methods are generally not reflective of fundamental risk differences—fair value is typically realized upon the orderly sale of a given private equity investment, irrespective of its accounting treatment during the holding period.[48]

Losses on Trading Exposures

The trading stress test models cover a wide range of a firm's exposure to asset classes such as public equity, foreign exchange, interest rates, commodities, securitized products, traded credit (for example, municipal securities, auction rate securities, corporate credit, and sovereign credit), and other fair-value assets. Loss projections are constructed by applying the market risk factor movements specified in the global market shock component [49] to market values of firm-provided positions and risk factor sensitivities.[50] The global market shock only applies to a subset of firms, as described in Section II.B.a of this Supplementary Information. In addition, the global market shock component is applied to firm counterparty exposures to generate losses due to changes in credit valuation adjustment, which is a change to the market value of an exposure (for example, a derivative) to account for the risk that the counterparty defaults on its obligation. Trading and credit valuation adjustment losses are calculated only for firms subject to the global market shock component. In contrast to the nine-quarter evolution of losses for other parts of the supervisory stress test, and as previously described, these losses are estimated and applied in the first quarter of the projection horizon. This timing is based on the observation that market dislocations can happen rapidly and unpredictably any time under stress conditions. It also ensures that potential losses from trading and counterparty exposures are incorporated into a firm's capital ratio at all points in the projection horizon.

The Board separately estimates the risk of losses arising from the default of issuers of debt securities held for trading. These losses account for concentration risk in corporate, sovereign, agency, and municipal credit positions. In contrast to the trading losses described above, these losses are applied in each of the nine quarters of the projection horizon to capture the risk that several quarters of stressful economic conditions may cause additional issuers of debt securities to default, which aligns with the Board's principle of conservatism from the Stress Testing Policy Statement.

Largest Counterparty Default Losses

The largest counterparty default component is applied to firms with substantial trading or custodial operations. This component captures the risk of loss due to the unexpected default of the counterparty whose default on derivatives and securities financing transactions, with exposures revalued by applying the global market shock component, would generate the largest stressed losses for a firm. Consistent with the Board's modeling principles and with the losses associated with the global market shock component, losses associated with the largest counterparty default component are recognized in the first quarter of the projection horizon.

Balance Projections and the Calculation of Regulatory Capital Ratios

As described above, the Board assumes that a firm takes actions to maintain its current level of assets, including its investment securities, trading assets, and loans, over the ( printed page 51866) projection horizon. The Board also assumes that a firm's risk-weighted assets and leverage ratio denominators remain unchanged over the projection horizon, except that the Board will account for changes primarily related to the calculation of regulatory capital or due to changes to the Board's regulations.[51]

The Board includes five regulatory capital ratios in the supervisory stress test: (1) common equity tier 1 risk-based capital, (2) tier 1 risk-based capital, (3) total risk-based capital, (4) tier 1 leverage, and (5) supplementary leverage. A firm's post-stress regulatory capital ratios are projected in accordance with the Board's regulatory capital rule using the Board's projections of pre-tax net income and other scenario-dependent components of the regulatory capital ratios. Pre-tax net income and the other scenario-dependent components of the regulatory capital ratios are combined with additional information, including assumptions about taxes and capital distributions, to project post-stress measures of regulatory capital. In those calculations, the Board adjusts pre-tax net income to account for taxes and other components of net income, such as income attributable to minority interests, to arrive at after-tax net income. The Board calculates the change in equity capital over the projection horizon by combining projected after-tax net income with changes in other comprehensive income, assumed capital distributions, and other components of equity capital. The path of regulatory capital measures over the projection horizon is calculated by combining the projected change in equity capital with the firm's starting capital position and accounting for other adjustments to regulatory capital specified in the Board's regulatory capital framework.[52] The denominator of each firm's risk-based capital ratios is based on a firm's standardized approach for calculating risk-weighted assets on the jump-off date of the supervisory stress test, and may change for each quarter of the projection horizon to account for adjustments specified in the capital rule (for example, adjustments due to the thresholds for deducting certain deferred tax assets).

B. Supervisory Stress Test Scenarios

The Board conducts the supervisory stress test using two scenarios—the baseline and severely adverse. The severely adverse scenario describes a hypothetical set of conditions designed to assess the strength and resilience of firms in a severely adverse economic environment and includes 28 variables that are disclosed by the Board each year prior to the supervisory stress test. Some variables describe economic developments within the United States while others describe developments in foreign countries.[53] These variables serve as an input to the calculation of supervisory stress test results for all firms. As discussed above, for a subset of firms, the severely adverse scenario also includes two additional components: the global market shock component and the largest counterparty default component. The scenarios and associated components are developed solely for supervisory stress testing purposes and do not represent economic forecasts of the Board.

Geographic Variation of Macroeconomic Variables

While the Board projects the paths of macroeconomic variables at the national level, the Board uses regional-level (that is, state- and/or county-level) macroeconomic variables in the stress test models to project losses on certain loans held for investment at amortized cost.[54] In general, model outputs are demonstrably impacted by the macroeconomic environment, as both probability of default and loss given default increase during periods of economic stress. Importantly, the macroeconomic environment can also vary notably across geography, in addition to across time. For instance, during the 2007-2009 crisis period, housing prices fell more sharply in certain geographies compared to others. Accordingly, historical loss rates in many loan categories were higher during this period in geographies where housing prices fell more sharply.

Therefore, to account for the impacts of different macroeconomic environments across geographies on historical loan performance, the Board calibrates model parameters in certain stress test models using regional macroeconomic variables as opposed to national macroeconomic variables. For example, the unemployment rate used in an applicable model may be the state level unemployment rate, while the house price index values used in the model may be the county-level house price indices or, in the case of loans in counties where a house price index is not projected, a state-level house price index.[55] Analysis performed by the Board demonstrates that a certain model's statistical fit and sensitivity to the macroeconomic environment may perform better when using regional-level variables compared to when using only national-level variables. The use of regional-level variables is described in each applicable model section of the comprehensive model documentation.

However, because the severely adverse scenario only includes national-level variable paths, the Board derives the paths of regional-level variables from the paths of national-level variables. The Board employs a simple approach to calculating the paths of regional-level variables in that these variables have the same percentage change (in the case of an index variable) or level change (in the case of non-index variables) as the national-level variables, but the starting points are the regional-level values, not the national-level values. For example, the projected path of the house price index is assumed to have the same percentage change in a given quarter as the percentage change of the national house price index,[56] and the projected path of unemployment rate is assumed to have the same level change in a given quarter as the level change of the national unemployment rate.[57] The use of percentage changes for home price indices and level changes for unemployment rates avoids accentuating differences in the macroeconomic environment observed immediately prior to the beginning of the scenario, which could lead to large discrepancies in projected variable paths across geographies during the severely adverse scenario.

These simple, uniform policies for allocating changes to the national ( printed page 51867) macroeconomic environment at the regional level ensure that loans to borrowers in certain geographies are not unduly favored or penalized. While it is plausible that certain geographies may experience more volatility than others in terms of the macroeconomic environment, the Board does not estimate such volatility to differentiate scenarios across geography, to avoid making assumptions about the severity of a hypothetical recession across different regions.

The Board also uses historical regional data to produce model projections. While the regional scenarios are projected based on the national path, the Board retains variation in the historical regional macroeconomic variables.[58] The Board may also use historical regional macroeconomic variables in the models to calculate the appreciation in house prices since origination (which may be needed to calculate loan-to-value ratios), or the Board may use regional macroeconomic variables to calculate year-over-year changes in the variables. Alternatively, the Board could replace all historical values with their national equivalent when projecting losses, thus applying a truly uniform treatment across geographies. While this alternative would have the benefit of maximizing geographic consistency, it would ignore meaningful variation in the historical environment and thereby reduce the predictive power of the model. For instance, if a given geography has had higher house price appreciation since its origination date compared to the national average, without incorporating these historical values into the macroeconomic data used to project losses the model would understate the level of equity the borrower has as of the beginning of the projection period. The Board has therefore developed this hybrid approach to estimating losses in the supervisory stress test, in which it applies a uniform treatment to projected values of macroeconomic variables across geographies, while also retaining historical differences across geographies. This methodology allows for the incorporation of all available historical data needed to produce accurate projections, while avoiding the need to make assumptions about which geographies will have more or less severe macroeconomic paths during a hypothetical recession. Further discussion of how the Board's models account for geographic variation in variables, including a proposed change to the Board's modeling approach, is included in the comprehensive model documentation, available at https://www.federalreserve.gov/supervisionreg/dfa-stress-tests-2026.htm.

Question 4: What are the advantages and disadvantages of the Board's treatment of regional (i.e., state and county) macroeconomic variables in the credit risk models?

Question 5: What alternatives should the Board consider to the approach outlined above for defining state and county macroeconomic variables based on the national variables included in the scenarios? What would be the advantages and disadvantages of these alternatives?

Auxiliary Variables

In addition to the 28 variables that the Board discloses each year, the Board also generates paths for a limited number of other variables that are used in the supervisory stress test. These variables, known as auxiliary variables, are not disclosed by the Board because their paths are based on the paths of the 28 disclosed variables (that is, the paths are contingent upon movements in the 28 disclosed variables). For example, the path of Mexico's gross domestic product (GDP) growth rate is a function of the GDP growth rate paths of other country blocs that are disclosed. Some models use these auxiliary variables, as described in the applicable model sections of the comprehensive model documentation available at https://www.federalreserve.gov/supervisionreg/dfa-stress-tests-2026.htm.[59]

C. Data Used in Stress Testing

Input Data

The Board generally develops and implements the models with data it collects on regulatory reports as well as proprietary third-party industry data. Most of the data used in the supervisory stress test projections are collected through the Capital Assessments and Stress Testing regulatory report (FR Y-14), which includes a set of annual (FR Y-14A), quarterly (FRY-14Q), and monthly (FRY-14M) schedules.[60]

A firm must submit detailed loan and securities information for all material portfolios on the FR Y-14Q and FR Y-14M. The definition of a material portfolio for purposes of FR Y-14 reporting is based on a firm's size and complexity.[61] Portfolio categories are defined in the FR Y-14M and FR Y-14Q reporting instructions. Each firm has the option to submit the relevant data schedule for a given portfolio that does not meet the materiality threshold as defined in the instructions. If a firm does not submit data on its immaterial portfolio(s), the Board will assign to that portfolio the median loss rate estimated across the set of firms with material portfolios. This loss assumption adheres to the principle of simplicity, as well as the principle of consistency and comparability, from the Stress Testing Policy Statement.

While each firm is responsible for ensuring the completeness and accuracy of data provided in the FR Y-14 reports, the Board makes efforts to validate firm-reported data and requests resubmissions of data where errors are identified. If data quality remains deficient after resubmission, the Board applies conservative assumptions to a particular portfolio or to specific data, depending on the severity of deficiencies. For example, if the Board deems the quality of a firm's submitted data too deficient to produce a stress test model estimate for a particular portfolio, then the Board assigns a high loss rate (for example, 90th percentile) or a conservative pre-provision net revenue rate (for example, 10th percentile) to the portfolio balances based on supervisory stress test projections of portfolio losses or pre-provision net revenue for other firms.[62] If data that are direct inputs to stress test models are missing or reported erroneously but the problem is isolated in such a way that the existing supervisory framework can still be used, the Board assigns a conservative value (for example, 10th or 90th percentile) to the specific data based on all available data reported by firms. These assumptions are consistent with the Board's principle of conservatism and policies on the treatment of immaterial portfolios and missing or erroneous ( printed page 51868) data, as described in the Stress Testing Policy Statement.

Additionally, certain stress test model projections rely on data from the Consolidated Financial Statements for Holding Companies regulatory report (FR Y-9C), which contains consolidated income statement and balance sheet information for each firm subject to the stress test. The FR Y-9C also includes off-balance sheet items and other supporting schedules, such as the components of risk-weighted assets and regulatory capital, that may be used in the stress test models.

In limited circumstances, the Board also uses data provided by third parties in the development and execution of the supervisory stress test. The comprehensive model documentation identifies these instances. The scenario data discussed above is also an input into the stress test projections.

Data Preparation and Adjustments

a. Data Preparation

The data inputs the Board uses may not be initially suitable for use in the stress test models. In these cases, the Board takes several steps to prepare the data for use in the stress test models. The specific steps for each model are discussed in the applicable model descriptions within the comprehensive model documentation, though generally data are prepared for use in the models for two purposes: to remove outliers from the sample and to seasonally adjust the data. These adjustments help ensure that the model results are reasonable.

The Board may remove outliers or data that are not applicable to the model from the sample to facilitate more usable results. For example, if a commercial real estate loan has a unusually high loan-to-value (LTV) ratio (over 150 percent at origination), then data for that loan are not included in the Commercial Real Estate Model because its inclusion may produce unreliable results. Additionally, if first lien mortgages are insured by the Federal Housing Administration or Department of Veterans Affairs, then they are excluded from the First Lien Model because these loans would not generate losses in the supervisory stress test, as they are assumed to be fully insured by the U.S. government. In both examples, the model output is more sensible and more reflective of a firm's risk profile because of these adjustments.

The Board also may seasonally adjust data, where appropriate. For example, the vacancy rate of hotel commercial real estate exposures may fluctuate on a seasonal cycle, with the vacancy rate moving higher or lower in certain months based on a somewhat predictable pattern. Because the vacancy rate can be an important variable for calculating losses on hotel commercial real estate loans, this rate is seasonally adjusted to ensure that the Commercial Real Estate Model produces more stable results.

These types of data preparation steps help ensure that the Board's models produce more reasonable results and that they align with the principles in the Stress Testing Policy Statement in that they generate consistent and robust projections. The Board therefore expects to continue to use these data preparation steps, where appropriate, as they are integral to the supervisory stress test process.

b. Data Adjustments

Data inputs are integral to generating the output of the stress test models, which is a key component of a firm's stress capital buffer requirement. The Board's Stress Testing Policy Statement notes that the Board does not use data submitted by one or some of the firms unless comparable data can be collected from all the firms that have material exposure in a given area when generating supervisory stress test projections.[63] However, situations may arise where adjustments to a firm's data would make the results more reasonable, and therefore better calibrate a firm's stress capital buffer requirement to its risk profile. The Board expects to continue to make these adjustments going forward, where appropriate. Examples of when the Board may apply these adjustments are described below.

For example, the Board may apply a data adjustment where there is missing or deficient firm-provided data, or where a firm uses divestiture accounting. As described above, if the Board deems the quality of a firm's submitted data too deficient to produce a stress test model estimate for a particular portfolio, then the Board assigns a conservative loss rate (for example, 90th percentile) or a conservative pre-provision net revenue rate (for example, 10th percentile) to the portfolio balances based on supervisory stress test projections of portfolio losses or pre-provision net revenue for other firms. If data that are direct inputs to stress test models are missing or reported erroneously but the problem is isolated in such a way that the existing supervisory framework can still be used, the Board assigns a conservative value to the specific data based on all available data reported by firms.

Additionally, when a firm sells assets or businesses, it may use divestiture accounting in its financial statements until the sale is consummated. Under divestiture accounting, a firm may list divested assets as discontinued operations, classify them as held for sale or available for sale instead of held for investment or held to maturity, and report revenues as income from discontinued operations. The accounting classification can be important for the supervisory stress test as it may determine which model stresses the assets or income. For example, in the 2025 supervisory stress test, the Board adjusted certain input data that had been reclassified due to divestiture accounting to improve projections of loan losses and related income to ensure consistent treatment across firms with similar risks.

IV. Enhanced Disclosure Process

The Board is proposing to codify an enhanced disclosure process under which the Board would annually publish comprehensive documentation on the stress test models, invite public comment on any material changes that the Board seeks to make to those models, and annually publish the stress test scenarios for comment.

A. Annual Disclosure of Models

Under the proposal, the Board would annually publish comprehensive documentation on the stress test models, similar to the comprehensive documentation the Board is publishing with this proposal at https://www.federalreserve.gov/supervisionreg/dfa-stress-tests-2026.htm. The Board would be required to publish this comprehensive documentation by May 15 of the year in which the stress test is performed, and the models described in the documentation would be used to produce the stress test results disclosed by the Board by June 30 of that year. In addition, the Board would seek public comment, and respond to such public comment, on any material changes to the models before implementing those changes in a stress test. Material model changes are discussed in more detail in Section IV.B of this Supplementary Information. To implement this enhanced disclosure process, the Board is proposing to revise Regulations YY and LL, as well as the Stress Testing Policy Statement.

For example, if the Board did not seek to make any material model changes to its stress test models for the 2027 supervisory stress test, then it would publish the comprehensive model documentation used in the 2027 stress test cycle by May 15, 2027. This ( printed page 51869) documentation would identify any changes (relative to the models used in the 2026 stress test), including technical, non-material changes to the models to improve performance. This process would allow the public to review the changes, as well as comprehensive documentation on the models used in the 2027 stress test cycle, before the release of the stress test results.

As an alternative example, if the Board sought to implement a material model change (as discussed in Section IV.B of this Supplementary Information) in the 2027 supervisory stress test, then the Board would seek comment on the proposed change, consider and respond to public feedback, and, then implement, defer, or reject the material model change for the 2027 stress test cycle. If the Board sought to implement the material model change in the 2027 stress test, the Board would republish updated model documentation before or simultaneously with the annual publication of comprehensive model documentation ( i.e., by May 15, 2027). This process for material model changes would increase the transparency of the Board's stress testing model framework and ensure that the public has the opportunity to comment on material model changes before they are used in the next stress test cycle.

Question 6: How else could the Board enhance the transparency and public accountability of its stress test models? For instance, what additional information regarding the stress test models, if any, should the Board provide, and why?

Question 7: How else could the Board facilitate public participation in model development? For example, the Board could invite comment on all model changes, rather than only material model changes, before implementing them in the stress test. Under such an approach, the Board could make an exception for technical or other types of ministerial changes. Such a process would limit the Board's flexibility to revise models due to unforeseen events and circumstances. What are the advantages and disadvantages of this expanded approach or other approaches to facilitate public participation in model development? How should the Board balance transparency and public accountability with model dynamism and operational burden?

Question 8: What are the advantages and disadvantages of inviting public comment, and committing to responding to comments, on material model changes before the Board implements them in the subsequent stress test?

Question 9: What are the advantages and disadvantages of publishing the comprehensive model documentation by May 15 of each stress test cycle? For example, does this timeline provide enough time for the public to review any changes made by the Board to confirm they are not material? Should the Board consider publishing the comprehensive model documentation earlier at an earlier date, such as April 5, or a later date, such as June 30? What would be the advantages or disadvantages of publishing the comprehensive model documentation earlier or later?

Question 10: The Board is not currently publishing the results of its internal model validation process. What would be the advantages and disadvantages of publishing these results or providing more information about its internal model validation process?

B. Model Changes

The proposed rule would define a “model change” to mean “the introduction of a new model or a conceptual change to an existing model.” [64] Conceptual changes to existing models would include changes to model assumptions, incorporation of a new statistical technique to estimate loss, or the addition or deletion of any model components or sub-components that currently inform a firm's stress capital buffer requirement.

Model changes would not include changes resulting from updates or adjustments to input data, such as firm data, third-party vendor data, and scenario data, including any re-estimation based on this data, as well as changes related to the mechanical implementation of federal, state, or local laws that are directly embedded in a stress test model ( e.g., the federal statutory tax rate).[65] As is current practice, the Board would continue to implement model changes related to changes in accounting definitions or regulatory capital rules and model parameter re-estimation based on newly available data with immediate effect. These types of adjustments would not be considered model changes since they do not substantively change the form of the stress test models as described in the documentation. For example, the Board re-estimates many of its models with updated data each year when it runs the supervisory stress test. This re-estimation may result in changes to the statistical coefficients produced by some of the models, even though the Board has made no conceptual changes to the models. Under the proposed definition of model change, such re-estimation would not be viewed as a model change because the resulting changes stem solely from updated data and not from a conceptual change to the models. In contrast, the introduction or revision of a legal requirement that causes a conceptual change to a model could be considered a model change, and the Board would seek public comment before implementing such a change if it met the proposed definition of a material model change.

Question 11: What other types of changes to the supervisory stress testing framework could the Board consider including in the definition of “model change”? What are the advantages and disadvantages of broadening or narrowing the definition of “model change”? For example, should the Board define “model changes” to include changes that result from new or updated input data, or changes that result from using a new, third-party data source?

C. Material Model Changes

Each year, the Board refines and enhances its stress test models to reflect advances in modeling techniques, respond to model validation findings, incorporate richer and more detailed data, or identify more stable models or models with improved performance, particularly under stressful economic conditions. These changes may include re-specification of models based on performance testing, benchmarking, and other targeted changes used to produce projections.[66] This process is an important aspect of the modeling framework to help ensure that the stress test models capture changes in borrower and lender behavior and bank business practices. These model changes also help ensure that the models are able to remain dynamic ( i.e., can be enhanced to capture emerging risks), produce ( printed page 51870) reasonable results, identify salient risks at firms, and maintain an optimal level of robustness and stability.

In addition, the Board must sometimes make changes to its stress test models while it is running the stress test in response to unforeseen events or circumstances to ensure that model output is reasonable. For example, during the COVID-19 pandemic, the vacancy rates for hotel properties were unprecedented and the Board made certain adjustments to yield sensible commercial real estate loan losses in the model output. Without making these in-cycle changes, the results of the stress test would have been irrational and led to stress capital buffer requirements that were not commensurate with applicable firms' risk profile.