Treasury Department

Permitted Payment Stablecoin Issuer Customer Identification Program

June 22, 2026

Summary

FinCEN and federal banking agencies propose requiring permitted payment stablecoin issuers (PPSIs) to establish customer identification programs (CIPs) under the Bank Secrecy Act, as mandated by the GENIUS Act. The rule would mandate risk-based identity verification, recordkeeping, and government-list checks for customers in primary market transactions, with compliance due 12 months after a final rule.

Document headings vary by document type but may contain the following:

- the agency or agencies that issued and signed a document

- the number of the CFR title and the number of each part the document amends, proposes to amend, or is directly related to

- the agency docket number / agency internal file number

- the RIN which identifies each regulatory action listed in the Unified Agenda of Federal Regulatory and Deregulatory Actions

See the Document Drafting Handbook for more details.

Department of the Treasury

Financial Crimes Enforcement Network

- 31 CFR Part 1033

- RIN 1506-AB74

AGENCY:

Financial Crimes Enforcement Network and Office of the Comptroller of the Currency, Treasury; Board of Governors of the Federal Reserve System; Federal Deposit Insurance Corporation; National Credit Union Administration.

ACTION:

Joint proposed rule.

SUMMARY:

The Financial Crimes Enforcement Network (FinCEN), together with the Office of the Comptroller of the Currency (OCC), the Board of Governors of the Federal Reserve System (Board), the Federal Deposit Insurance Corporation (FDIC), and the National Credit Union Administration (NCUA) are jointly issuing this proposed rule to implement certain provisions of the Guiding and Establishing National and Innovation for U.S. Stablecoins Act (GENIUS Act). Specifically, this rulemaking implements the GENIUS Act's directives to treat permitted payment stablecoin issuers as financial institutions under the Bank Secrecy Act and to require issuers to maintain an effective customer identification program.

DATES:

Comments must be received by August 21, 2026.

ADDRESSES:

Comments should be directed to:

FinCEN: Comments must be submitted in one of the following two ways (please choose only one of the ways listed):

- Electronically athttps://www.regulations.gov. Follow the “Submit a comment” instructions under Docket FINCEN-2026-0101. If you are reading this document on federalregister.gov, you may use the green “SUBMIT A PUBLIC COMMENT” button beneath this rulemaking's title to submit a comment to the regulations.gov docket.

- You may mail written comments to the following address: Regulatory and Strategic Affairs Division, Financial Crimes Enforcement Network, P.O. Box 39, Vienna, VA 22183. Mailed comments must be received by the close of the comment period.

Do not include any personally identifiable information (such as name, address, or other contact information) or confidential business information that you do not want publicly disclosed. All comments are public records; they are publicly displayed exactly as received, and will not be deleted, modified, or redacted. Comments may be submitted anonymously.

Follow the search instructions on https://www.regulations.gov to view public comments.

OCC: Commenters are encouraged to submit comments through the Federal eRulemaking Portal. Please use the title “Permitted Payment Stablecoin Issuer Customer Identification Program” and “RIN 1557-AF53” to facilitate the organization and distribution of the comments. You may submit comments by any of the following methods:

- Federal eRulemaking Portal—Regulations.gov: Go to https://regulations.gov. Enter Docket ID OCC-2026-0331 in the Search Box and click “Search.” Public comments can be submitted via the “Comment” box below the displayed document information or by clicking on the document title and then clicking the “Comment” box on the top-left side of the screen. For help with submitting effective comments please click on “Commenter's Checklist.” For assistance with the regulations.gov site, please call 1-866-498-2945 (toll free) Monday-Friday, 9 a.m.-5 p.m. ET, or email regulationshelpdesk@gsa.gov.

- Mail: Chief Counsel's Office, Attention: Comment Processing, Office of the Comptroller of the Currency, 400 7th Street SW, Suite 1E-216, Washington, DC 20219.

- Hand Delivery/Courier: 400 7th Street SW, Suite 1E-216, Washington, DC 20219.

Instructions: You must include “OCC” as the agency name and Docket ID OCC-2026-0331 in your comment. In general, the OCC will enter all comments received into the docket and publish the comments on the regulations.gov website without change, including any business or personal information provided such as name and address information, email addresses, or phone numbers. Comments received, including attachments and other supporting materials, are part of the public record and subject to public disclosure. Do not include any information in your comment or supporting materials that you consider confidential or inappropriate for public disclosure.

You may review comments and other related materials that pertain to this action by the following method:

- Viewing Comments Electronically—Regulations.gov: Go to https://regulations.gov. Enter Docket ID OCC-2026-0331 in the Search Box and click “Search.” Click on the “Documents” tab and then the document's title. After clicking the document's title, click the “Document Comments” tab. Comments can be viewed and filtered by clicking on the “Sort By” drop-down on the right side of the screen or the “Refine Results” options on the left side of the screen. Supporting materials can be viewed by clicking on the “Documents” tab. Click on the “Sort By” drop-down on the right side of the screen or the “Refine Documents Results” options on the left side of the screen checking the “Supporting & Related Material” checkbox. For assistance with the regulations.gov site, please call 1-866-498-2945 (toll free) Monday-Friday, 9 a.m.-5 p.m. ET, or email regulationshelpdesk@gsa.gov.

The docket may be viewed after the close of the comment period in the same manner as during the comment period.

Board: You may submit comments, identified by Docket No. R-1885 and RIN 7100-AH18, by any of the following methods:

- Agency Website: https://www.federalreserve.gov. Follow the instructions for submitting comments at https://www.federalreserve.gov/generalinfo/foia/ProposedRegs.cfm.

- Email: regs.comments@federalreserve.gov. Include docket and RIN numbers in the subject line of the message.

- Fax: (202) 452-3819 or (202) 452-3102.

- Mail: Benjamin W. McDonough, Secretary, Board of Governors of the Federal Reserve System, 20th Street and Constitution Avenue NW, Washington, DC 20551.

- Instructions: All public comments are available from the Board's website at https://www.federalreserve.gov/generalinfo/foia/ProposedRegs.cfm as submitted. Accordingly, comments will not be edited to remove any identifying or contact information. Public comments may also be viewed electronically or on paper in Room M-4365A, 2001 C Street NW, Washington, DC 20551, between 9 a.m. and 5 p.m. during Federal business weekdays. For security reasons, the Board requires that visitors make an appointment to inspect comments. You may do so by calling (202) 452-3684. Upon arrival, visitors will be required to present valid government-issued photo identification and to submit to security screening in order to inspect and photocopy comments. For users of TTY-TRS, please call 711 from any telephone, anywhere in the United States.

FDIC: You may submit comments, identified by RIN 3064-AG28, by any of the following methods: ( printed page 37235)

- FDIC Website: https://www.fdic.gov/federal-register-publications. Follow instructions for submitting comments on the agency website.

- Email: Comments@fdic.gov. Include RIN 3064-AG28 in the subject line of the message.

- Mail: Jennifer M. Jones, Deputy Executive Secretary, Attention: Comments—RIN 3064-AG28, Federal Deposit Insurance Corporation, 550 17th Street NW, Washington, DC 20429.

- Hand Delivery to FDIC: Comments may be hand-delivered to the guard station at the rear of the 550 17th Street NW building (located on F Street) on business days between 7 a.m. and 5 p.m.

- Public Inspection: Comments received, including any personal information provided, may be posted without change to https://www.fdic.gov/federal-register-publications. Commenters should submit only information that the commenter wishes to make available publicly. The FDIC may review, redact, or refrain from posting all or any portion of any comment that it may deem to be inappropriate for publication, such as irrelevant or obscene material. The FDIC may post only a single representative example of identical or substantially identical comments, and in such cases will generally identify the number of identical or substantially identical comments represented by the posted example. All comments that have been redacted, as well as those that have not been posted, that contain comments on the merits of the proposed rule will be retained in the public comment file and will be considered as required under all applicable laws. All comments may be accessible under the Freedom of Information Act.

NCUA: You may submit comments, identified by RIN 3133-AG09, by any of the following methods (please send comments by one method only):

- Federal eRulemaking Portal: https://www.regulations.gov. The docket number for this proposed rule is NCUA-2026-0793. Follow the instructions for submitting comments. A plain language summary of the proposed rule is also available on the docket website.

- Mail: Address to Melane Conyers-Ausbrooks, Secretary of the Board, National Credit Union Administration, 1775 Duke Street, Alexandria, Virginia 22314-3428.

- Hand Delivery/Courier: Same as mailing address.

- Public inspection: You may view all public comments on the Federal eRulemaking Portal at https://www.regulations.gov, as submitted, except for those we cannot post for technical reasons. The NCUA will not edit or remove any identifying or contact information from the public comments submitted. If you are unable to access public comments on the internet, you may contact the NCUA for alternative access by calling (703) 518-6540 or emailing OGCMail@ncua.gov.

FOR FURTHER INFORMATION CONTACT:

FinCEN: The FinCEN Regulatory Support Section by submitting an inquiry at www.fincen.gov/contact.

OCC: Kenneth Kohrs, BSA/AML Lead Expert, Office of the Chief National Bank Examiner; Jina Cheon, Assistant Director, Melissa Lisenbee, Counsel, or Henry Barkhausen, Counsel, Bank Advisory Group, Chief Counsel's Office, (202) 649-5490, Office of the Comptroller of the Currency, 400 7th Street SW, Washington, DC 20219. If you are deaf, hard of hearing, or have a speech disability, please dial 7-1-1 to access telecommunications relay services.

Board: Division of Supervision and Regulation, Lara Lylozian, Deputy Associate Director, (202) 815-9088, Lee Davis, Lead BSA/AML Policy Analyst, (202) 740-8219, lee.h.davis@frb.gov, Legal Division, Jason Gonzalez, Deputy Associate General Counsel, (202) 452-3275, jason.a.gonzalez@frb.gov, Bernard Kim, Special Counsel, (202) 452-3083, Bernard.g.kim@frb.gov.

FDIC: Patricia Colohan, Deputy Director, (202) 898-7283, PColohan@fdic.gov, Division of Risk Management Supervision; Chase Lubbock, Associate Director, (703) 254-0802, clubbock@fdic.gov, Division of Risk Management Supervision; Christy Cornell-Pape, Acting Chief, Financial Crimes, (415) 808-8090, ACornell-Pape@fdic.gov, Division of Risk Management Supervision; Deborah Tobolowsky, Counsel, (571) 309-2415, dtobolowsky@fdic.gov, Legal Division; Chantal Hernandez, Counsel, (202) 898-7388, chhernandez@fdic.gov, Legal Division; Thomas Krepp, Senior Attorney, (678) 916-2265, tkrepp@fdic.gov, Legal Division; Lea Pfeifer, Senior Attorney, (972) 761-8244, lpfeifer@fdic.gov, Legal Division; Maryann Bullion Mitchell, Senior Attorney, (571) 858-8239, mbullionmitchell@fdic.gov, Legal Division; Nicholas Kazmerski, Counsel, (571) 309-3136, nkazmerski@fdic.gov, Legal Division.

NCUA: Michael Dondarski, Associate Director, Office of Examination & Insurance, (703) 772- 4751, mdondarski@ncua.gov; Janell Portare, Director, Fraud and Anti-Money Laundering Division, Office of Examination & Insurance, (703) 548-2752, jportare@ncua.gov; Gira Bose, Senior Staff Attorney, Office of General Counsel, (703) 518-6540, gbose@ncua.gov.

SUPPLEMENTARY INFORMATION:

I. Introduction

This proposal implements the GENIUS Act's directives to treat permitted payment stablecoin issuers (PPSIs) as financial institutions for purposes of the Bank Secrecy Act (BSA) and to require such issuers to maintain an “effective customer identification program, including identification and verification of account holders.” [1] This notice of proposed rulemaking (NPRM) is being issued jointly by FinCEN, along with the OCC, Board, FDIC, and NCUA (each an “Agency” and collectively “the Agencies”) as applied to the PPSIs that each Agency supervises.[2] The proposal would also apply to PPSIs that opt for state supervision under the GENIUS Act.[3]

Separately, FinCEN issued a rulemaking proposing changes to its existing regulations to effectuate the GENIUS Act's direction to apply BSA obligations to PPSIs. These changes include creation of a new part in chapter X applicable to PPSIs, proposed part 1033, into which this proposed rule would be incorporated.[4]

II. Background and Authority

The GENIUS Act provides a comprehensive framework for the regulation of payment stablecoins.[5] The GENIUS Act requires that a PPSI “be treated as a financial institution for purposes of the Bank Secrecy Act, and ( printed page 37236) as such, shall be subject to all Federal laws applicable to a financial institution located in the United States relating to economic sanctions, prevention of money laundering, customer identification, and due diligence.” [6] In addition to this clear, general directive, the GENIUS Act specifies that a PPSI's obligations include “maintenance of an effective customer identification program, including identification and verification of account holders with the permitted payment stablecoin issuer.” [7]

The Bank Secrecy Act, or “BSA,” is the common name for a collection of statutory authorities designed to, among other things, safeguard the national security of the United States by combating money laundering, the financing of terrorism, and other illicit finance activity.[8] The Secretary of the Treasury has delegated the authority to implement, administer, and enforce the BSA and its associated regulations to the Director of FinCEN.[9] The BSA requires the Secretary of the Treasury to prescribe “minimum standards” for financial institutions regarding “the identity of the customer that shall apply in connection with the opening of an account,” commonly referred to as customer identification programs (CIPs).[10] Under the BSA, these minimum standards the Secretary of the Treasury prescribes must include reasonable procedures for: (1) verifying the identity of any person seeking to open an account to the extent reasonable and practicable; (2) maintaining records of the information used to verify a person's identity, including name, address, and other identifying information; and (3) determining whether the person appears on any lists of known or suspected terrorists or terrorist organizations provided to the financial institution by any government agency.[11] In prescribing regulations related to these minimum standards, the BSA directs the Secretary of the Treasury to “take into consideration the various types of accounts maintained by various types of financial institutions, the various methods of opening accounts, and the various types of identifying information available.” [12] For financial institutions engaging in financial activity described in section 4(k) of the Bank Holding Company Act of 1956, such regulations must be jointly prescribed by the Secretary of the Treasury and the appropriate Federal functional regulator.[13]

FinCEN, jointly with the appropriate Federal functional regulators, has issued implementing regulations imposing CIP obligations on various types of financial institutions under the BSA, including banks,[14] brokers or dealers in securities,[15] mutual funds,[16] and futures commission merchants and introducing brokers.[17] In contrast, money transmitters do not have a CIP obligation, but they are required to, for certain activity, verify an individual's identity.[18] Stablecoin issuers are presently subject to BSA obligations as financial institutions and, more specifically, as money transmitters under FinCEN's regulations, which are a type of money services business (MSB).[19]

The GENIUS Act directs the Secretary of the Treasury to issue regulations, tailored to the size and complexity of the PPSI, to implement the GENIUS Act's treatment of PPSIs as financial institutions for purposes of the BSA, including the requirement that PPSIs maintain effective customer identification programs.[20] The GENIUS Act also directs the Secretary of the Treasury and each primary Federal payment stablecoin regulator—the OCC, Board, FDIC, and NCUA—to issue regulations through appropriate notice and comment rulemaking and to coordinate, as appropriate, to carry out the Act.[21] FinCEN and the Agencies are issuing a single, joint rule, ensuring consistent and uniform application of CIP requirements to all PPSIs subject to each Agency's jurisdiction.[22]

III. GENIUS Act Implementation

Treasury issued an advance notice of proposed rulemaking (ANPRM) in September 2025 seeking public comment on potential Treasury regulations implementing the GENIUS Act, including those imposing BSA, anti-money laundering, and sanctions compliance program obligations.[23] In ( printed page 37237) response to this ANPRM, Treasury received approximately 450 timely comments from a variety of stakeholders, including banks and credit unions, stablecoin issuers, digital asset exchanges, analytics companies, law firms, trade associations, non-governmental organizations, technology firms, academics, and members of the public. In crafting this proposal, Treasury reviewed and considered the pertinent comments, including those related to illicit finance topics.

This NPRM represents one piece of the comprehensive regulatory framework for PPSIs set out in the GENIUS Act.[24] In a separate rulemaking, FinCEN has proposed a rule to implement the GENIUS Act's directive to apply anti-money laundering obligations to PPSIs (referred to as “PPSI AML/CFT NPRM”), including program, reporting, and recordkeeping obligations, among others.[25] The PPSI AML/CFT NPRM proposes adding several new definitions arising from the GENIUS Act to chapter X, which are here used to describe this proposed rule. These definitions include “digital asset,” [26] “distributed ledger,” [27] “payment stablecoin,” [28] “permitted payment stablecoin issuer,” [29] “primary Federal payment stablecoin regulator,” [30] “Federal qualified payment stablecoin issuer,” [31] “State payment stablecoin regulator,” [32] and “State qualified payment stablecoin issuer.” [33] Generally speaking, the proposed definitions in the PPSI AML/CFT NPRM track the language the GENIUS Act uses to define those terms, with a few proposed technical modifications that are intended to be non-substantive.

IV. Overview of Stablecoins and Issuers

The GENIUS Act only governs a subcategory of stablecoins, namely “payment stablecoins” as defined by the GENIUS Act, and a subcategory of actors in the payment stablecoin ecosystem, most critically for this rulemaking, PPSIs.[34] Thus, under the GENIUS Act, not all stablecoins are payment stablecoins and not all stablecoin issuers will be eligible to be PPSIs. Because the GENIUS Act framework is not yet in place, however, it is not determined which specific stablecoins will be payment stablecoins and which specific stablecoin issuers will be PPSIs. An understanding of the stablecoin ecosystem, uses of stablecoins, and risks associated with stablecoins generally informs the parameters of the proposed rule, including the rationale behind certain proposed obligations.

A. Stablecoins and Their Uses

Stablecoins are a blockchain-based [35] digital asset [36] designed to maintain a stable value relative to an underlying asset, most often—but not always—a fiat currency.[37] Most stablecoin issuers use smart contracts [38] to issue stablecoins, enable or prohibit subsequent transactions in the stablecoin, and redeem stablecoins. The smart contracts underlying most stablecoins maintain a ledger of the number of stablecoins “owned by a set of accounts where each account is owned by a blockchain address” or wallet.[39]

The liquidity and stability of stablecoins relative to other digital assets and rapid settlement of stablecoins make them appealing to illicit actors as well as legitimate users.[40] Currently, most legitimate users primarily rely on stablecoins to store value or facilitate trades in other digital assets. Payment stablecoins have the potential, however, to become a more widely adopted form of payment.[41] Illicit actors have increasingly used stablecoins to facilitate transactions and store proceeds.[42] The U.S. government has linked stablecoins to a range of illicit activities, including money laundering, and bad actors, including scammers and fraudsters; [43] Democratic People's Republic of Korea information technology workers, cybercriminal groups, and related money laundering ( printed page 37238) networks; [44] drug traffickers; [45] terrorist groups; [46] and sanctions evasion and money laundering networks,[47] among others.

B. Issuers and Interactions With Users

Most stablecoins backed by financial assets, including fiat currency, have centralized control, meaning that one company, or a group of companies, are responsible for governance functions, including defining and ensuring compliance with standards related to the issuance, purchase, redemption, custody, and transfer of the stablecoin.

Currently, many stablecoin issuers generally interact directly with a small number of larger companies—which are often institutional participants in the trading of digital assets ( i.e., digital asset exchanges).[48] Those companies, in turn, interact with a larger and more diverse group of users. Many stablecoin issuers predominantly offer issue and redemption services to financial institutions, including digital asset exchanges that may be regulated under the BSA as MSBs.[49] Generally, once an issuer issues stablecoins to such financial institutions, those financial institutions put the stablecoins into broader circulation to other users, such as individual retail users.[50]

Due to the use of smart contracts underlying stablecoin transactions and how users interact with stablecoin issuers, the ecosystem can, broadly speaking, be divided into two components, the primary market and the secondary market. For purposes of this rulemaking, FinCEN and the Agencies will use the term “primary market” to generally describe a PPSI interacting directly with a user or holder of a payment stablecoin, such as when a PPSI engages in issuing, converting, redeeming, repurchasing, burning, and reissuing payment stablecoins, as well as providing associated services, such as providing custodial services.[51] FinCEN and the Agencies will use the term “secondary market” to describe payment stablecoin activity that does not directly involve the PPSI as a party to the transaction other than via a smart contract. For example, secondary market activity could include an individual purchasing payment stablecoins from intermediaries, an individual sending a payment stablecoin from a self-hosted wallet to a vendor to purchase goods, an individual exchanging payment stablecoins for another digital asset via a digital asset exchange, or person-to-person transactions in payment stablecoins.

V. Section-by-Section Analysis

As required by the GENIUS Act, this rulemaking proposes a CIP obligation for accounts maintained by PPSIs.[52] Obligations under this proposal are comparable to existing CIP requirements for other financial institutions, such as banks, brokers-dealers, mutual funds, and futures commission merchants and introducing brokers in commodities. PPSIs likely will frequently interact with financial institutions that are already subject to CIP requirements, and in some cases, PPSIs will be subsidiaries of insured depository institutions with CIP requirements.[53] Subjecting PPSIs to CIP requirements similar to such institutions is expected to increase the effectiveness and efficiency of CIP programs and facilitate the ability of PPSIs and other financial institutions with CIP requirements to rely on another institution's performance of any procedure related to a CIP, with the recommended safeguards contained in proposed 31 CFR 1033.220(a)(6).

In crafting this proposal, FinCEN and the Agencies have considered the statutory factors articulated in the BSA, specifically the various types of accounts PPSIs may maintain, the various methods of opening accounts, and the various types of identifying information available.[54] Most notably, FinCEN and the Agencies recognize that these factors may vary significantly by the size and complexity of the PPSI, the activities in which it engages, and the types of customers it has. Accordingly, rather than prescribe a one-size-fits-all approach, FinCEN and the Agencies direct that a PPSI's CIP should address the types of accounts it intends to maintain, how it allows those accounts to be opened, and the types of identifying information available. In defining “account,” as noted below, the proposal takes into consideration the range of activities in which a PPSI can engage and the types of accounts that a PPSI may maintain.

Relatedly, as mentioned above, the GENIUS Act directs the Secretary to tailor BSA obligations to the size and complexity of an issuer.[55] This proposal meets that requirement by proposing regulatory text that requires a PPSI to tailor its CIP to that PPSI's size and type of business, as well as take into consideration the PPSI's risk based on its unique business—including the types of accounts it has, how those accounts are opened, and the identifying information available. Other policy options to tailor for size and complexity were considered including, for example, a CIP obligation that would fluctuate solely based on the size of an issuer. FinCEN and the Agencies have preliminarily assessed, however, that such an approach, however, could harm national security by providing weaker points of entry to the financial system, but request comment on its approach. This CIP proposal necessarily results in tailored obligations, which comports with the GENIUS Act, mitigates the risk of weaker points of entry, and best ( printed page 37239) protects the U.S. financial system from illicit activity.

A. Proposed 31 CFR 1033.100—Definitions

FinCEN and the Agencies propose promulgating in § 1033.100 three new definitions with respect to the proposed CIP obligation—account, customer, and digital asset service provider.[56] The definitions are proposed for purposes of this CIP rulemaking and would only apply to the CIP obligation unless otherwise expressly noted.[57]

The definitions discussed in this proposal are designed to clarify that a PPSI's CIP obligation extends to direct relationships, i.e., primary market activity, and does not extend to activity where the only interaction is with a PPSI's smart contract. Consistent with the BSA, the CIP requirements for other types of financial institutions extend to where an institution has some sort of formal relationship with an individual or entity.[58] Based on the language in section 4(a)(5) of the GENIUS Act, and the analysis undertaken by FinCEN and the Agencies of the stablecoin ecosystem, FinCEN and the Agencies assess that the term “customer” in section 4(a)(5) related to “customer identification program” pertains to circumstances where the “customer” and a PPSI have a direct interaction and relationship. Put differently, the term “customer” is not meant to apply where a transfer is the result of third parties and a payment stablecoin user's only interaction with the PPSI is through a smart contract.

Moreover, interaction with a smart contract does not currently result in a PPSI acquiring the kind of information needed to verify an identity. Imposing an obligation where any payment stablecoin transfer could, for purposes of a CIP obligation, result in a customer and account relationship with a PPSI would essentially impose on PPSIs a global obligation to collect and verify identifying information of individual users. FinCEN and the Agencies assess that such a CIP obligation would be nearly impossible for PPSIs to implement and could potentially cripple the industry. FinCEN and the Agencies, however, seek comment on this approach and their assessment of the difficulties of such a globally applicable CIP obligation.

1. Proposed 31 CFR 1033.100(a)—Account

FinCEN and the Agencies propose adding the definition of “account” at § 1033.100(a). The proposed definition resembles how “account” is defined in other CIP rules, but contains unique provisions that reflect the kinds of activities in which PPSIs can engage. It also considers, as the BSA requires, the types of accounts PPSIs may maintain.

The proposed text defines an “account” in paragraph (a)(1) as a formal relationship between a PPSI and a customer, established to provide or engage in services, dealings, or other financial transactions. The “formal relationship” language mimics most other CIP rules promulgated under the BSA.[59] FinCEN and the Agencies are proposing carrying this language over to the PPSI CIP to promote consistency, efficiency, and the ability of institutions to rely on each other for CIP procedures (subject safeguards). FinCEN and the Agencies request comment, however, on whether the formal relationship language is sufficiently clear.

Similar to the definition of “account” for other financial institutions subject to CIP requirements, the proposed definition of account contains an illustrative list of activities that may fall within “services, dealings, or other financial transactions.” [60] The proposed examples are based on the GENIUS Act's provision limiting PPSI activities, including the GENIUS Act rule of construction that clarifies a PPSI can engage in digital asset service provider activities or activities incidental thereto to the extent where those activities are consistent with all other Federal and State laws and authorized by the appropriate primary Federal or State payment stablecoin regulator.[61] As proposed, the illustrative list would include: (i) issuing or redeeming a payment stablecoin; (ii) managing related reserves, including purchasing, selling, and holding reserve assets or providing custodial services for reserve assets; (iii) providing custodial or safekeeping services for payment stablecoins, required reserves, or private keys of payment stablecoins; (iv) other activities that directly support activities in paragraphs (a)(1)(i), (ii), and (iii); or (v) providing services of a digital asset service provider that are authorized by the primary Federal payment stablecoin regulator or the State payment stablecoin regulator, as applicable, consistent with all other Federal and State laws, provided that the claims of payment stablecoin holders rank senior to any potential claims of non-stablecoin creditors with respect to the reserve assets, consistent with section 11 of the GENIUS Act. FinCEN and the Agencies assess that providing such examples promotes clarity while leaving room for innovations in the industry that could create new, but similar, relationships between a PPSI and a person that involves a formal relationship and could fall under the “account” definition.

Unlike with other types of financial institutions with CIP requirements, an individual with no established relationship with a PPSI could hold a PPSI's product, specifically a payment stablecoin, and then seek to engage directly with a PPSI for a financial service. For example, an individual who has no established relationship with the PPSI could acquire a payment stablecoin from, for example, an exchange, and seek to redeem it with the PPSI. That redemption could establish an account with the PPSI and make the individual a customer. FinCEN requests comment on whether the CIP proposal should be refined or clarified to account for such activity.

The proposed definition also provides instances where activity does not form an account relationship. Two of these ( printed page 37240) subparagraphs are intended to make clear that purely secondary market payment stablecoin activity does not form a formal relationship between a PPSI and a payment stablecoin user or holder. That list provides that the term “account” does not include a product or service where a formal relationship is not established with a person, such as payment stablecoin activity that does not directly involve the PPSI as a party to the transaction other than via a smart contract. It also specifies that ownership or control of a PPSI's payment stablecoins alone, without other indicators of a formal relationship, does not constitute an account.

Consistent with other CIP rules, the proposed text further provides that the term “account” does not include an account that the PPSI acquires through an acquisition, merger, purchase of assets, or assumption of liabilities from a financial institution regulated by a Federal functional regulator or a bank regulated by a State bank regulator or an account opened for the purpose of participating in an employee benefit plan established under the Employee Retirement Income Security Act of 1974.

2. Proposed 31 CFR 1033.100(b)—Customer

FinCEN and the Agencies propose adding the definition of “customer” at § 1033.100(b) for the purposes of a PPSI's CIP obligation. The proposal would define customer as (i) a person that opens a new account; and (ii) an individual who opens a new account for: (A) an individual who lacks legal capacity, such as a minor; or (B) an entity that is not a legal person, such as a civic club.

The proposed definition also provides that the term “customer” does not include: (i) a financial institution regulated by a Federal functional regulator or a bank regulated by a State bank regulator; (ii) a person described in § 1020.315(b)(2) through (4) of 31 CFR chapter X; (iii) a person that has an existing account with the PPSI, provided the PPSI has a reasonable belief that it knows the true identity of the person; or (iv) a person acquiring or redeeming a payment stablecoin from a means other than directly from or directly to the PPSI. The final provision promotes FinCEN and the Agencies' determination that transfers of payment stablecoins on the secondary market do not make a party to the transfer a customer of a PPSI.

3. Proposed 31 CFR 1033.100(c)—Digital Asset Service Provider

FinCEN and the Agencies propose adding a definition of “digital asset service provider” at § 1033.100(c) for the purposes of a PPSI's CIP obligations because the term is used in the proposed definition of “account.” As discussed, the GENIUS Act expressly reserves the ability of a PPSI to engage in the digital asset service provider activities, where such activities are authorized by the appropriate primary Federal payment stablecoin regulator or State payment stablecoin regulator.[62] To help ensure such activities are appropriately included in activities that could create an account relationship with a PPSI, FinCEN and the Agencies propose defining “digital asset service provider” for CIP purposes.

The proposed definition of “digital asset service provider” is consistent with the definition provided in the GENIUS Act, with certain modifications in light of preexisting FinCEN regulatory definitions.[63] Under the proposed rule, the term “digital asset service provider” would mean an individual, partnership, company, corporation, association, trust, estate, cooperative organization, or other business entity, incorporated or unincorporated that, for compensation or profit, engages in business in the United States (including on behalf of customers or users in the United States) of: (A) exchanging digital assets for monetary value, meaning a national currency or deposit denominated in a national currency; (B) exchanging digital assets for other digital assets; (C) transferring digital assets to a third party; (D) acting as a digital asset custodian; or (E) participating in financial services relating to digital asset issuance. The proposed definition also provides that the term “digital asset service provider” does not include: (i) a distributed ledger protocol; (ii) developing, operating, or engaging in the business of developing distributed ledger protocols or self-custodial software interfaces; (iii) an immutable and self-custodial software interface; (iv) developing, operating, or engaging in the business of validating transaction or operating a distributed ledger; or (v) participating in a liquidity pool or other similar mechanism for the provisioning of liquidity for peer-to-peer transactions. The proposed definition of digital asset service provider will also state the meaning of “distributed ledger protocol,” as defined by 12 U.S.C. 5901(9).

This proposed definition modifies the GENIUS Act language in three respects. None of the changes are intended to substantively change the meaning of the GENIUS Act definition of digital asset service provider.

First, the proposed definition modifies the GENIUS Act definition of digital asset service provider by replacing the statutory term “person” in that definition with the text the GENIUS Act uses to define “person” in 12 U.S.C. 5901(24).[64] This change is proposed because the term “person” is already defined in FinCEN regulations at 31 CFR 1010.100(mm) [65] and differs from the GENIUS Act definition of “person.” [66] FinCEN's regulatory definition of person includes Indian Tribes as defined in the Indian Gaming Regulatory Act, which the GENIUS Act definition of person does not include. Further, FinCEN's regulatory definition also does not characterize the entities that comprise the category as “business” entities, as the GENIUS Act definition does. To ensure the definition of “digital asset service provider” for PPSIs accurately applies to the “persons” that Congress intended, as evidenced by the GENIUS Act definition of the term, FinCEN and the Agencies propose incorporating the GENIUS Act definition of person into the regulatory definition of “digital asset service provider.”

Second, the proposed definition of “digital asset service provider” incorporates the GENIUS Act definition of “monetary value” as provided in 12 U.S.C. 5901(17).[67] FinCEN has two similar terms, “monetary instruments” and “currency,” that are already defined in its regulations at 31 CFR 1010.100(dd) [68] and 31 CFR ( printed page 37241) 1010.100(m).[69] To avoid confusion between the existing definitions and the definition in the GENIUS Act, FinCEN and the Agencies propose including the GENIUS Act definition of “monetary value” within the definition of “digital asset service provider.”

Third, and finally, the proposed definition of “digital asset service provider” also incorporates the GENIUS Act definition “distributed ledger protocol” as provided in 12 U.S.C. 5901(9).[70] The term “distributed ledger protocol” is not otherwise used in the proposed regulation, so FinCEN and the Agencies propose including the term and its definition within the definition of “digital asset service provider.”

B. Proposed 31 CFR 1033.220—Customer Identification Program

1. Proposed 31 CFR 1033.220(a) and (a)(1)—Minimum Requirements

Proposed § 1033.220(a) would establish the minimum standards for a CIP. Proposed § 1033.220(a)(1) would require a PPSI to establish and maintain a written CIP. The CIP would be required to be appropriate for a PPSI's size and business.

As with the CIP rule for banks and other financial institutions with CIP obligations, a PPSI's CIP would be required to be a part of the PPSI's anti-money laundering and countering the financing of terrorism (AML/CFT) program. As discussed in the PPSI AML/CFT NPRM, FinCEN and the Agencies recognize the value of enterprise-wide compliance efforts. Where a PPSI is a subsidiary of an insured depository institution, FinCEN and the Agencies anticipate that the enterprise may elect to extend a single AML/CFT program to both entities and that doing so would be permissible so long as a comprehensive AML/CFT program is reasonably designed to identify and mitigate the risks posed by the different aspects of each entity's business and activities and satisfies each of the risk-based AML/CFT program and other applicable BSA and GENIUS Act requirements to which the PPSI or parent is subject. Likewise, an enterprise may elect to implement an enterprise-wide CIP rather than maintain separate CIPs for a parent and subsidiary. In doing so, however, the enterprise-wide CIP would need to account for the legal and regulatory obligations of both the parent and subsidiary. Relatedly, where a PPSI is also a national trust bank, the entity could create a single CIP covering all the entity's regulatory obligations.

2. Proposed 31 CFR 1033.220(a)(2)—Identity Verification Procedures

Proposed § 1033.220(a)(2) would impose obligations related to identity verification procedures, effectuating 31 U.S.C. 5318( l)(2)(A). It would require that the CIP include risk-based procedures for verifying the identity of each customer to the extent reasonable and practicable. The procedures must enable the PPSI to form a reasonable belief that it knows the identity of each customer. The procedures must be based on the PPSI's assessment of the relevant risks, including those presented by the various types of accounts maintained by the PPSI, the various methods of opening accounts provided by the PPSI, the various types of identifying information available, and the PPSI's size, location, and customer base.

As with existing CIP rules, the rule proposes to include the term “risk-based” as a descriptor of these procedures.[71] The identity verification procedures would need to be based on the PPSI's assessment of the relevant risks, and take into consideration the types of accounts the PPSI maintains, the different methods of opening accounts, and the types of identifying information available.[72] Ultimately the procedures must enable the PPSI to form a reasonable belief that it knows the true identity of the customer.[73] A risk-based framework reflects the fact that variations in customer relationships can present varying levels of risks.[74]

i. Proposed 31 CFR 1033.220(a)(2)(i)—Customer Information Required

Proposed § 1033.220(a)(2)(i) would specify identifying information that a CIP must account for in procedures for opening an account. The proposed rule would require a PPSI to obtain from each customer the following information prior to opening an account: (1) name; (2) date of birth, for an individual; or date of formation, for a person that is not an individual; (3) address (a residential and mailing address for individuals, or the principal place of business, local office, or other physical address and mailing address for a person other than an individual); and (4) an identification number.

The proposed rule would require that a PPSI collect a residential or business street address for an individual. If the individual does not have a residential or business street address, the individual may provide an Army Post Office or a Fleet Post Office box number or the residential or business street address of a next of kin or another contact individual. If the customer is a corporation, partnership or trust, it must provide the address of its principal place of business, local office, or other physical location. A Post Office (PO) box is not an acceptable type of address for the purposes of the proposed rule. Similarly, although some virtual offices or commercial mail receiving agencies provide an address for an entity or individual to use, similar to a PO box, the address provided is not an actual place of business or residence for the entity or individual and does not evidence a physical location for the customer.[75] Accordingly, such addresses are not acceptable physical locations for purposes of the proposed rule.

The proposed rule would also require collection of an identification number. For U.S. persons this would be a taxpayer identification number. For non-U.S. persons the identification number could be one or more of the following: a taxpayer identification number, passport number and country of issuance, alien identification card number, or number and country of issuance of any other government-issued document evidencing nationality or residence and bearing a photograph or similar safeguard. For a non-U.S. person that is not an individual and that does not have an identification number, the PPSI must request alternative ( printed page 37242) government-issued documentation certifying the existence of the person.

The proposed rule provides an exception for persons applying for a taxpayer identification number. However, the exception would require that the CIP include procedures for confirming that the application for a taxpayer identification number was filed, as well as obtaining the taxpayer identification number within a reasonable period of time after the account is opened.

ii. Proposed 31 CFR 1033.220(a)(2)(ii)—Customer Verification

Proposed § 1033.220(a)(2)(ii) relates to CIP procedures for verifying the identity of a customer using the information the PPSI has collected. The proposed rule would require that the CIP contains procedures for verifying the identity of each new customer within a reasonable period of time after the customer's account is opened. The procedures must describe when the PPSI will use documents, non-documentary methods, or a combination of both methods.

FinCEN and the Agencies recognize the interest in leveraging verifiable credentials and digital identity as part of account opening procedures.[76] Over 20 years ago when the bank CIP final rule was promulgated, FinCEN and staff of the Board, FDIC, NCUA, OCC, and the Office of Thrift Supervision (OTS) recognized in guidance that an “electronic credential” was one method that an institution could use to form a reasonable belief that it knows the true identity of its customer.[77] Since that time, digital identity tools have become more commonplace and more sophisticated. Notably, however, there are a variety of digital identity tools and applications currently in existence, as well as a significant number under development. These tools vary in how they operate and in their trustworthiness.[78]

FinCEN and the Agencies propose that technological variation and innovation are best accounted for by maintaining the flexibility in the proposal relating to how a PPSI verifies a customer's identity. This flexibility will enable individual PPSIs to assess its comfort level with the trustworthiness of various tools and take into consideration variation in tools and differences in risk. FinCEN and the Agencies expect that PPSIs would treat different digital identity tools differently. For example, a mobile ID or driver's license issued by a state could constitute an “unexpired government-issued identification evidencing nationality or residence and bearing a photograph or similar safeguard” under proposed § 1033.220(a)(2)(ii)(A). A digital identity credential offered by a non-governmental entity that enables a person to prove that they are who they claim to be without revealing information other than that fact could, if appropriate as part of a risk-based procedure, be a non-documentary verification method. Accordingly, FinCEN and the Agencies are not proposing regulatory text related to verifiable credentials and digital identities, but request comment on this approach.

a. Proposed 31 CFR 1033.220(a)(2)(ii)(A)—Verification Through Documents

The proposed rule states that if the PPSI is relying on documents to verify a customer's identity, then the CIP must contain procedures that set forth the documents that the PPSI will use. For an individual, the PPSI could use an unexpired government-issued identification evidencing nationality or residence that contains a photograph or similar safeguard, such as a driver's license or passport. For a person other than an individual, such as a corporation, partnership, or trust, the document must show the existence of the entity, such as certified articles of incorporation, a government-issued business license, a partnership agreement, or a trust instrument.

b. Proposed 31 CFR 1033.220(a)(2)(ii)(B)—Verification Through Non-Documentary Methods

For a PPSI relying on non-documentary methods to verify a customer's identity, the proposed rule would require the CIP to contain procedures that set forth the non-documentary methods the PPSI will use. These methods may include contacting a customer; independently verifying the customer's identity through the comparison of information provided with respect to the customer with information obtained from a consumer reporting agency, public database, or other source; checking references with other financial institutions; or obtaining a financial statement.

Under the proposed rule, the PPSI's non-documentary procedures would be required to address situations where an individual is unable to present an unexpired government-issued identification document that bears a photograph or similar safeguard; the PPSI is not familiar with the documents presented; the account is opened without obtaining documents; the customer opens the account without meeting in person; or the PPSI is otherwise presented with circumstances that increase the risk that the PPSI will be unable to verify the true identity of a customer through documents.

c. Proposed 31 CFR 1033.220(a)(2)(ii)(C)—Additional Verification for Certain Customers

Proposed § 1033.220(a)(2)(ii)(C) would require that a PPSI's CIP address situations where, based on the PPSI's risk assessment of a new account opened by a customer that is not an individual, the PPSI will obtain information about individuals with authority or control over such account to verify the customer's identity. This verification method would apply only when the PPSI cannot verify the true identity of a customer that is not an individual through either documentary or non-documentary methods.

iii. Proposed 31 CFR 1033.220(a)(2)(iii)—Lack of Verification

FinCEN and the Agencies believe that, while the majority of customers may be verified through documentary and non-documentary methods, there may be instances where this is not possible. Proposed § 1033.220(a)(2)(iii) relates to CIP procedures in which the PPSI cannot form a reasonable belief that it knows the true identity of a customer. Under the proposed rule, these procedures would be required to describe: (1) when the PPSI should not open an account; (2) the terms under which a customer may use an account while the PPSI attempts to verify the customer's identity; (3) when the PPSI should close an account after attempts to verify a customer's identity fail; and (4) when the PPSI should file a Suspicious Activity Report in accordance with applicable law and regulation. ( printed page 37243)

3. Proposed 31 CFR 1033.220(a)(3)—Records

The proposed rule in § 1033.220(a)(3) states that the CIP must include procedures for making and maintaining a record of all information obtained by the PPSI through the CIP, effectuating 31 U.S.C. 5318( l)(2)(B). At a minimum, proposed § 1033.220(a)(3)(i) would require that the record include: (1) all identifying information about a customer obtained under the CIP; (2) a description of any document relied on to verify the identity of the customer under the CIP, noting the type of document, any identification number contained in the document, the place of issuance, and if any, the date of issuance and expiration date; (3) a description of the methods and results of any measures undertaken to verify the identity of a customer; and (4) a description of the resolution of each substantive discrepancy discovered when verifying the identifying information obtained.

Additionally, the proposed rule states that a PPSI must retain the identifying information about a customer obtained under § 1033.220(a)(3)(i)(A) for five years after the date the account is closed and the information regarding the verification of a customer's identity records collected under § 1033.220(a)(3)(i)(B), (C), and (D) for five years after the record is made.

4. Proposed 31 CFR 1033.220(a)(4)—Comparison With Government Lists

Proposed § 1033.220(a)(4) would require a PPSI's CIP to include reasonable procedures for determining whether a customer appears on any list of known or suspected terrorists or terrorist organizations issued by any Federal government agency and designated as such by Treasury in consultation with the Federal functional regulators, effectuating 31 U.S.C. 5318( l)(2)(C). The procedures would have to require the PPSI to make such a determination within a reasonable period of time after the account is opened, or earlier if required by another Federal law or regulation or Federal directive issued in connection with the applicable list. The procedures also would have to require the PPSI to follow all Federal directives issued in connection with such lists.

Because Treasury and the Federal functional regulators have not yet designated any such lists, the proposed rule cannot be more specific with respect to the lists PPSIs must check in order to comply with this provision. Accordingly, PPSIs would not have an affirmative duty under this proposed regulation to seek out all lists of known or suspected terrorists or terrorist organizations compiled by the Federal government. Instead, PPSIs would receive separate notification regarding the lists that must be consulted for purposes of this provision.

Many PPSIs already have procedures in place for determining whether customers' names appear on some Federal lists, including lists that identify known terrorists and terrorist organizations. For example, under current law, there are substantive legal requirements associated with lists circulated by Treasury's Office of Foreign Assets Control (OFAC). Failure to comply with these requirements may result in criminal or civil penalties.

5. Proposed 31 CFR 1033.220(a)(5)—Customer Notice

The proposed rule states in § 1033.220(a)(5) that the CIP must include procedures for providing customers with adequate notice that the PPSI is requesting information to verify their identities. Under the proposed rule, notice would be considered adequate if the PPSI generally described the identification requirements of this section and provided such notice in a manner reasonably designed to ensure that a prospective customer is able to view the notice, or is otherwise given notice, before opening an account. For example, depending upon the manner in which the account is opened, a PPSI may post a notice on its website, include the notice in its account applications, or use any other form of oral or written notice. The proposed rule provides a sample notice.

6. Proposed 31 CFR 1033.220(a)(6)—Reliance on Another Financial Institution

Proposed § 1033.220(a)(6) would provide that a PPSI's CIP may include procedures specifying when a PPSI may rely on another Federally regulated financial institution's performance of a procedure with respect to any PPSI customer that is opening or has opened an account. Such reliance would have to be reasonable under the circumstances, and the other financial institution on which the PPSI seeks to rely would have to be subject to an AML/CFT program with CIP requirements, as well as regulated by a Federal functional regulator.[79] Additionally, the institutions would have to have a contract requiring the institution on which the PPSI seeks to rely to certify annually to the PPSI that it has implemented an AML/CFT program and will perform (or its agent will perform) the specified requirements of the PPSI's CIP. Critically, this proposed provision would not change a PPSI's CIP obligation, and the PPSI would remain responsible for its compliance.

This proposal is consistent with other CIP requirements under the BSA, including the bank CIP regulation where, critically, some banks—but not all banks—are overseen by a Federal functional regulator.[80] It does, however, create a disparity between PPSIs that fall under a primary Federal payment stablecoin regulator and a State payment stablecoin regulator.[81] A State qualified payment stablecoin issuer would be able to rely on, for example, a procedure performed by a PPSI that is a subsidiary of an insured depository institution. But a PPSI that is a subsidiary of a Federally regulated depository institution, would not be able to rely on a procedure performed by a State qualified payment stablecoin issuer because such issuers are not overseen by a Federal functional regulator.

While the proposal would not permit a PPSI to rely on another entity to perform a CIP procedure unless such an entity is another Federally regulated financial institution, it should not be construed as restricting appropriate use of third parties to perform a service related to a PPSI's CIP on the PPSI's behalf.[82] In such cases, however, the CIP obligation would remain with the PPSI.

C. Proposed 31 CFR 1033.220(b)—Exemptions

Proposed § 1033.220(b) would provide that the appropriate Federal functional regulator, with the concurrence of the Secretary, may by order or regulation, exempt any PPSI or any type of account from the ( printed page 37244) requirements of this section. It also provides that the Secretary, with the concurrence of the Federal functional regulator, may exempt any PPSI or any type of account from the requirements of this section.

In issuing such exemptions, the Federal functional regulator and the Secretary would consider whether the exemption is consistent with the purposes of the BSA and with safety and soundness, as well as in the public interest. It would also permit the Federal functional regulator and Secretary to consider other necessary and appropriate factors. Given that the GENIUS Act identifies the OCC, Board, FDIC, and NCUA as a primary Federal payment stablecoin regulator for PPSIs under their respective jurisdictions, in this proposed rule, FinCEN and the Agencies retain “Federal functional regulator” consistent with its use in the BSA CIP exemption provision, providing the Secretary of the Treasury and the Federal functional regulator joint authority to issue an exemption.[83]

D. Proposed 31 CFR 1033.220(c)—Other Requirements Unaffected

Proposed § 1033.220(c) clarifies that nothing in § 1033.220 relieves a PPSI of its obligation to comply with any other provision of chapter X, including provisions concerning information that must be obtained, verified, or maintained in connection with any account or transaction, including requirements to have the technological capability to comply with and to comply with the terms of any lawful order.[84]

E. Compliance Date

FinCEN and the Agencies propose that the rule would be effective 12 months after issuance of the final rule to allow sufficient time for PPSIs to review and implement the requirements of the proposed rule.

VI. Request for Comments

FinCEN and the Agencies seek comments on all aspects of the proposed rule and specifically seek comments on the following topics. For all responses, commenters are encouraged to provide the basis for any conclusions drawn in their comments.

1. Should any CIP requirement be extended to secondary market activity? If yes, in what circumstances? What would be the benefits and drawbacks of doing so?

2. Should FinCEN and the Agencies refine or clarify its definitions of account, customer, or digital asset service provider? Are additional definitions needed?

3. Should FinCEN and the Agencies retain “formal relationship” as part of the definition of account? What are the hallmarks of a “formal relationship” between a PPSI and a user? Should FinCEN and the Agencies provide examples or attributes of a formal relationship in guidance? Would other concepts be a better foundation for the account definition, such as a contractual or business relationship, and why?

4. Should the proposed rule be clarified or refined to account for situations where a customer's only desired relationship with a PPSI is to redeem a payment stablecoin?

5. Should the regulatory text explicitly discuss digital identity solutions or verifiable credentials? How could it best do so given the range of tools available on the market?

6. What are the benefits and risks of using digital identity solutions or verifiable credentials as part of verifying customers' identities?

7. What is the expected likelihood that a PPSI would rely on another PPSI's CIP or the CIP of another Federal functionally regulated financial institution's CIP?

8. What, if anything, could be changed to make the proposed rule more conducive to industry innovation? Explain how any changes would positively or negatively impact PPSIs expected operations and illicit finance risk to the U.S. financial system.

VII. Executive Order 14294

Section 5 of Executive Order 14294 directs that all future notices of proposed rulemaking (NPRMs) and final rules published in the Federal Register , the violation of which may constitute criminal regulatory offenses, should include a statement identifying that the rule or proposed rule is a criminal regulatory offense and the authorizing statute.[85] Executive Order 14294 directs agencies to draft this statement in consultation with the Department of Justice.

Executive Order 14294 further directs that the regulatory text of all NPRMs and final rules with criminal consequences published in the Federal Register after May 9, 2025 should explicitly state a mens rea requirement for each element of a criminal regulatory offense, accompanied by citations to the relevant provisions of the authorizing statute.

Willful violations of the proposed regulations set forth in this proposed rule, if finalized, may be subject to criminal penalties pursuant to 31 U.S.C. 5322 and regulations promulgated in 31 CFR chapter X. The statutory authority for criminal liability requires a mens rea of willfulness as an element pursuant to 31 U.S.C. 5322(a) and 31 U.S.C. 5322(b). FinCEN's existing regulation, 31 CFR 1010.840, that sets out criminal penalties for violations of regulations promulgated in 31 CFR chapter X also includes a mens rea of willfulness. The Department of Justice was consulted in drafting this statement.

VIII. Regulatory Impact Analysis

FinCEN and the Agencies have analyzed the proposed rule as required under E.O. 12866,[86] E.O. 13563,[87] E.O. 14192,[88] the Regulatory Flexibility Act (RFA),[89] the Unfunded Mandates Reform Act of 1995 (UMRA),[90] the Paperwork Reduction Act (PRA),[91] the Riegle Community Development and Regulatory Improvement Act of 1994,[92] the Gramm-Leach-Bliley Act,[93] and the Providing Accountability Through Transparency Act of 2023.[94]

The Office of Information and Regulatory Affairs in the Office of Management and Budget (OMB) has determined this proposed rule to be a “significant regulatory action” under section 3(f) of E.O. 12866. FinCEN and the Agencies have included an Initial Regulatory Flexibility Analysis (IRFA) pursuant to the RFA as the proposed rule may have a significant economic impact on a substantial number of certain types of potentially affected small entities.[95] Pursuant to analysis ( printed page 37245) required by UMRA, FinCEN and the Agencies conclude it is unlikely that the proposed rule, if implemented, would result in a novel annual expenditure of more than $193 million by State, local, and Tribal governments or by the private sector.[96]

As described above,[97] the proposed rule would implement the GENIUS Act's directives to treat PPSIs as financial institutions for purposes of the BSA and to require such issuers to maintain an “effective customer identification program, including identification and verification of the identity of account holders.” [98] It includes proposed requirements for a PPSI to establish and maintain a written CIP; maintain risk-based procedures for verifying the identity of each customer to the extent reasonable and practicable; maintain certain records; and compare the customers' identity with government lists. The proposal would also require a PPSI to include procedures for customer notice related to verifying identity, allows reliance on another financial institution's CIP under certain circumstances, and outlines the ability of FinCEN and the Agencies to issue exemptions related to the CIP requirement.

In issuing this proposal, FinCEN and the Agencies contemplate a number of benefits for PPSIs, regulators, other compliance examiners, law enforcement and national security agencies, and the general public. Such benefits include CIPs that effectively contribute to the detection and deterrence of money laundering and terrorist financing, support broader BSA policy goals, and help ensure that CIPs for PPSIs are consistent with those required for other financial institution types with CIP requirements, which should promote efficiencies and reduce opportunities for regulatory arbitrage.

This regulatory impact analysis (RIA) begins by describing the broad economic analysis FinCEN and the Agencies undertook to inform their expectations of the proposed rule's economic impact and burden.[99] This is followed by pieces of additional and, in some cases, more specifically tailored analysis as required by E.O.s 12866, 13563, and 14192; [100] the RFA; [101] the UMRA; [102] and the PRA.[103] Requests for comments related to the RIA—regarding specific findings, assumptions, or expectations, or with respect to the analysis in its entirety—can be found in the final subsection.[104] These requests for comments have been previewed throughout the RIA.

A. Assessment of Impact

Consistent with best practices in regulatory economic analysis, FinCEN and the Agencies' assessment of impact begins with an overview of broad economic considerations, identifying, among other things, the need for the policy intervention.[105] Next, FinCEN and the Agencies (1) establish baseline estimates of the number of covered PPSIs and other entities, including insured depository institutions, that could be affected by the proposed rule, and (2) describe the current regulatory requirements and background practices against which the proposed rule would introduce changes.[106] The analysis then briefly reviews elements of the proposed rule that most directly inform how foreseeable economic impacts would flow from how PPSIs and their respective regulators would engage in activities not expected to otherwise be undertaken in order to comply.[107] Next, the RIA presents the anticipated benefits and estimated costs to the respective affected parties that would be associated with the proposed CIP obligations.[108] Finally, the assessment concludes with a brief discussion of alternative policies FinCEN and the Agencies considered and could have proposed, including an evaluation of the relative economic merits of each against the expected value of the rule as proposed.[109]

1. Broad Economic Considerations

In performing its assessment of impact, FinCEN and the Agencies took into consideration certain fundamental economic problems that the proposed rule is expected to address as well as the general social and economic costs that may ensue from an AML/CFT and CIP regime for PPSIs that is ineffective. Because this NPRM is being issued pursuant to statutory obligations,[110] the necessity for FinCEN and the Agencies to independently identify and articulate fundamental economic problems that the proposed rule is intended to address, as the basis for regulatory action,[111] is attenuated because at best this activity would complement the problem identification already performed by Congress.[112] Nevertheless, FinCEN and the Agencies have remained mindful of these animating considerations as well as the general social and economic costs that may ensue from an ineffective AML/CFT regime.[113]

FinCEN and the Agencies expect that the proposed rulemaking would meaningfully alleviate certain underlying economic problems that could otherwise impair the effective administration of the BSA and potentially distort affected markets. These include potential problems that flow from the incidence of both positive and negative externalities in connection with customer identification activity and the potential for regulatory arbitrage in the absence of uniform minimum standards for financial institutions' CIPs.[114]

The expected benefits of the proposed rule, as discussed below,[115] are therefore linked by the extent to which the proposed requirements would address these fundamental economic problems.

2. Institutional Baseline and Affected Parties

In proposing this rule, FinCEN and the Agencies considered the ( printed page 37246) incremental impacts of the proposed CIP requirements relative to the current state of the affected markets and their participants.[116] This baseline analysis of the parties that would be affected by the proposed rule, their current CIP-like obligations and activities, and the costs and/or benefits associated with those activities satisfies analytical best practices by describing the alternative of not pursuing the proposed, or any other, novel regulatory action.[117] In each case, the RIA has attempted to identify the incremental expected economic effects of each component of the proposal as precisely as practicable against this baseline. Nevertheless, in certain cases, FinCEN and the Agencies can only make qualitative assessments.

As a first step in the process of isolating these anticipated marginal effects, FinCEN and the Agencies assessed the regulatory and market landscape facing the current stablecoin issuers, and potential future PPSIs, that would be affected by the proposed rule, including an estimate of the expected near-term number of potential PPSIs, their existing regulatory requirements, and the burden they either would or currently face in connection with the compliance activities the proposed rule would require. FinCEN and the Agencies also briefly discuss other categories of persons and entities ( i.e., regulators, compliance examiners, law enforcement and national security agencies, and certain members of the general public) that are expected to be directly affected by the proposed rule.

i. Regulatory Baseline

As discussed in section II, stablecoin issuers are already subject to BSA obligations as MSBs, specifically, money transmitters. As MSBs, stablecoin issuers are currently subject to a range of BSA obligations. MSBs are required to, for instance, (i) establish and maintain written AML programs [118] that include policies, procedures, and internal controls to verify customer identification; [119] (ii) file currency transaction reports; [120] (iii) file Suspicious Activity Reports (SARs); [121] and (iv) maintain certain records, including those relating to certain transmittals of funds.[122] MSBs are required to register with FinCEN [123] and are subject to examination for BSA compliance by the Internal Revenue Service (IRS).[124]

While MSBs are not subject to as many customer identification requirements as other types of financial institutions under the BSA, the BSA does require them to maintain policies, procedures, and internal controls to verify customer identification [125] and to collect identification information for transmittals of funds over $3,000—including the name, address, and identification document of an individual requesting transmission [126] —and for transactions in currency of more than $10,000.[127]

ii. Baseline of Expected Affected Parties

FinCEN and the Agencies have identified four distinct populations expected to be directly affected, to varying degree, by the proposed rule, namely: (1) PPSIs, (2) customers of PPSIs, (3) certain other financial institutions, and (4) other less directly affected parties, including regulators (including examiners working for or under the authority of those regulators) and law enforcement and national security agencies. To the extent that economic impact on additional key, directly affected subpopulations of the general public should be considered, FinCEN and the Agencies invite comments, data, studies, or reports that would enhance its ability to identify and quantify such effects.

a. PPSIs

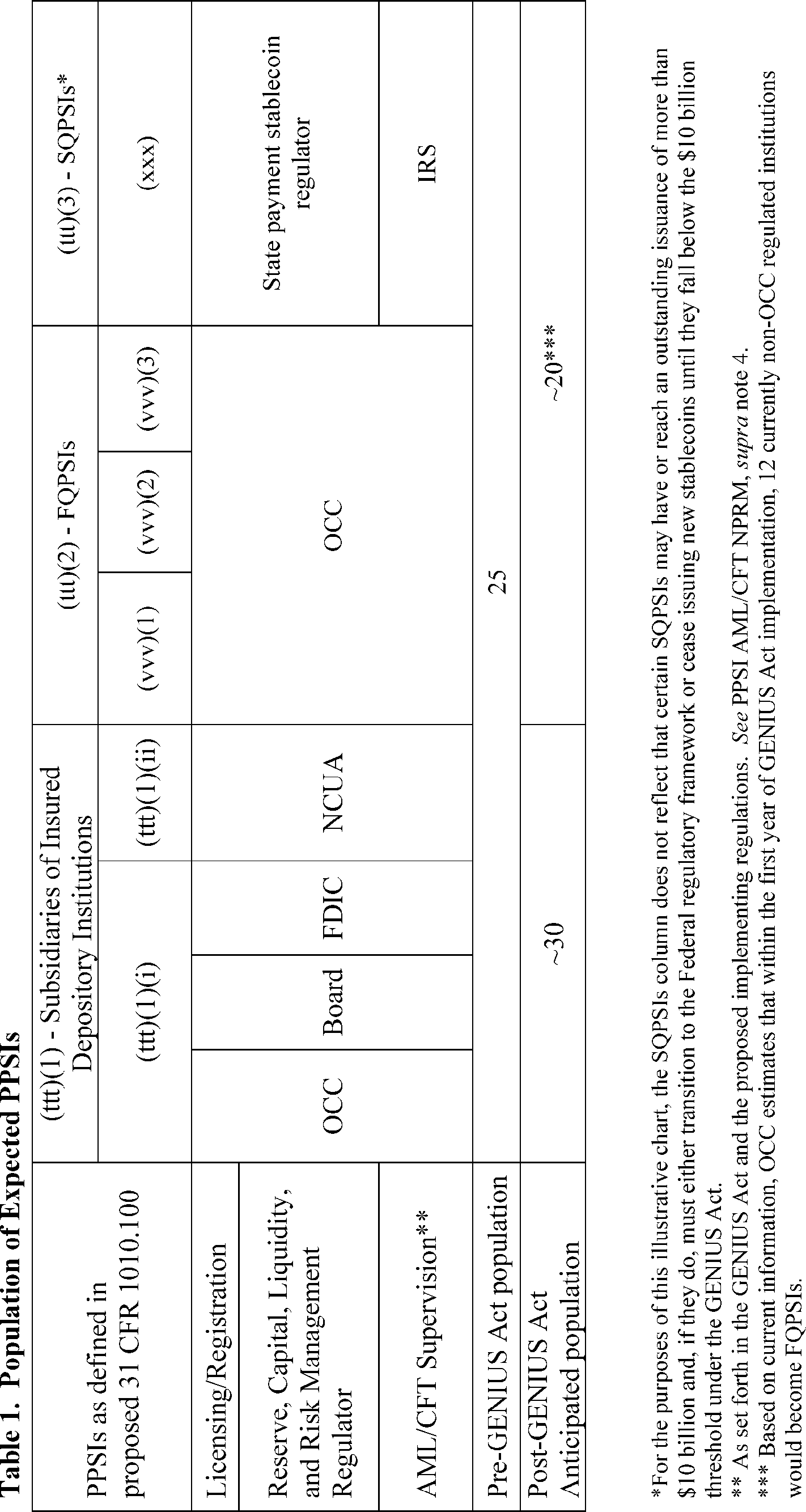

FinCEN and the Agencies have conducted independent research with a view to estimating the number of potential PPSIs that would exist in the near-term future.[128] Taking each of those independent exercises into consideration, the proposed rule could be expected to apply to approximately 50 PPSIs in each of the first three years of the GENIUS Act being effective. Table 1 illustrates the anticipated distribution of these potential PPSIs as organized by types as categorized in the GENIUS Act's definition of “permitted payment stablecoin issuer” [129] and proposed definition § 1010.100(ttt). That proposed definition contains three subtypes of PPSIs, specifically those that are subsidiaries of insured depository institutions or credit unions that have been approved to issue payment stablecoins by a primary Federal payment stablecoin regulator (collectively “subsidiaries of insured depository institutions”); Federal qualified payment stablecoin issuers (FQPSIs); and State qualified payment stablecoin issuers (SQPSIs).[130] As explained in proposed § 1010.100(vvv), a FQPSI is an entity approved by the OCC under 12 U.S.C. 5903 to issue payment stablecoins and is either—(1) a nonbank entity, (2) an uninsured national bank, or (3) a Federal branch.[131]

FinCEN expects that of the 50 anticipated PPSIs, approximately 60 percent should be subsidiaries of insured depository institutions and 40 percent not.[132 133] Because FinCEN has not identified, with more certainty than not, currently operating stablecoin issuers that it expects will become SQPSIs within the PPSI regulatory framework (as defined in proposed § 1010.100(ttt)(3) and § 1010.100(xxx)), the population used in this analysis does not further distinguish its estimate for these types of potential future PPSIs from other non-IDI subsidiary expected future PPSIs.[134] Because these projections represent best-effort estimates based on limited information, ( printed page 37247) the public is strongly encouraged to provide additional comments, data, and other information that could enhance the accuracy and precision of these estimates.

( printed page 37248){kind=link}

b. Customers of PPSIs

FinCEN and the Agencies expect the general public to be affected by the proposed rule, with certain subpopulations affected more directly than others. In particular, FinCEN and the Agencies considered customers of PPSIs, as the term “customer” is proposed to be defined in this rulemaking. Although estimated payment stablecoin users number in the hundreds of millions, a substantially smaller number (in the hundreds of thousands) are likely to interact with PPSIs in the primary market. Many of these customers are large financial institutions and most large stablecoin issuers set significant financial requirements for primary market participants that exclude retail-level participation. In terms of volume, most primary market activity can be attributed to these large entities. Most primary market activity, as measured in transaction volume, is attributable to these large entities. However, some issuers have increasingly adopted wider-facing mint/redeem models that seek to include smaller investors and businesses.

To estimate the number of expected primary market customers a future PPSI might interact with, FinCEN examined current on-chain minting and redemption activity as observable from publicly available data. Almost all the stablecoin products meeting the GENIUS Act's definitional criteria for future payment stablecoins that FinCEN reviewed had fewer than 1,000 primary market customers in a given year, which is consistent with prior expectations of high institutional barriers. However, a small number of the stablecoins reviewed had significantly more primary market contact (with over 250,000 customers) in a given year. In the sample of issuers FinCEN reviewed, the average number of an issuer's primary market customers was approximately 17,000, but this value appeared to be driven by extreme outliers. The truncated average was approximately 1,000, and the median value was 100.[135]

Based on this analysis, FinCEN estimate that the “average” PPSI would have approximately 1,000 primary market customers that it interacts with directly, including issuing and redeeming payment stablecoins and engaging in digital asset service provider activities where those activities are authorized by the appropriate primary Federal or the State payment stablecoin regulator and consistent with all other Federal and State laws. However, some PPSIs are expected to have substantially more or substantially less customers than this estimate. In total, FinCEN does not expect the total number of unique primary market PPSI customers to exceed 300,000. However, FinCEN estimates that a substantial portion of these customers may be affiliates of a single counterparty or associated with non-U.S. entities.[136] FinCEN estimates that the number of customers that are U.S. businesses is likely no more than 10,000. As described earlier, these businesses belong to several categories, including digital asset exchanges, specialized digital asset commodities traders, and other types of investment- and securities-related businesses. Besides digital asset exchanges, FinCEN expects most of a PPSI's other customers are likely to be financial institutions.[137]