Treasury Department

Regulatory Capital Rule: Modifications to the Enhanced Supplementary Leverage Ratio Standards for U.S. Global Systemically Important Bank Holding Companies and Their Subsidiary Depository Institutions; Total Loss-Absorbing Capacity and Long-Term Debt Requirements for U.S. Global Systemically Important Bank Holding Companies

December 1, 2025 · Effective April 1, 2026

Summary

This final rule adjusts the enhanced supplementary leverage ratio (eSLR) standards for U.S. global systemically important bank holding companies (GSIBs) and certain subsidiary depository institutions. The amendments aim to ensure leverage standards serve as a backstop rather than a primary constraint, alongside technical updates to loss-absorbing capacity requirements and capital reporting frameworks.

AI-generated summary · May 24, 2026. Verify with your compliance counsel before acting.

How this was generated

We record the exact prompt, model, and output for every AI response so it can be audited for accuracy.

Document headings vary by document type but may contain the following:

- the agency or agencies that issued and signed a document

- the number of the CFR title and the number of each part the document amends, proposes to amend, or is directly related to

- the agency docket number / agency internal file number

- the RIN which identifies each regulatory action listed in the Unified Agenda of Federal Regulatory and Deregulatory Actions

See the Document Drafting Handbook for more details.

Department of the Treasury

Office of the Comptroller of the Currency

- 12 CFR Parts 3 and 6

- [Docket ID OCC—2025-0006]

- RIN 1557-AF31

Federal Reserve System

- 12 CFR Parts 208, 217, and 252

- [Regulations H, Q, and YY; Docket No. R-1867]

- RIN 7100-AG96

Federal Deposit Insurance Corporation

- 12 CFR Part 324

- RIN 3064-AG11

AGENCY:

Office of the Comptroller of the Currency, Treasury; the Board of Governors of the Federal Reserve System; and the Federal Deposit Insurance Corporation.

ACTION:

Final rule.

SUMMARY:

The Office of the Comptroller of the Currency (OCC), Board of Governors of the Federal Reserve System (Board), and Federal Deposit Insurance Corporation (FDIC) are adopting a final rule to modify the enhanced supplementary leverage ratio standards applicable to U.S. bank holding companies identified as global systemically important bank holding companies (GSIBs), their subsidiary depository institutions that are Board- or FDIC-regulated, and national banks and Federal savings associations that are subsidiaries of a U.S. top-tier bank holding company with total consolidated assets of more than $700 billion or assets under custody of more than $10 trillion (together with Board- and FDIC-regulated subsidiary depository institutions of GSIBs, covered depository institutions). These modifications are intended to help ensure that the enhanced supplementary leverage ratio standards serve as a backstop to risk-based capital requirements rather than a frequently binding constraint, thus reducing potential disincentives for GSIBs and covered depository institutions to participate in low-risk, low-return activities. The Board is also finalizing conforming amendments to its total loss-absorbing capacity and long-term debt requirements. In addition, the Board is making conforming amendments to relevant regulatory reporting forms, and the Board and FDIC are making final certain technical corrections to the capital rule and the prompt corrective action framework. Banking organizations subject to the final rule may elect to early adopt the final rule as of January 1, 2026.

DATES:

The final rule is effective April 1, 2026.

FOR FURTHER INFORMATION CONTACT:

OCC: Venus Fan, Risk Expert, Benjamin Pegg, Technical Expert, Capital Policy, (202) 649-6370; Carl Kaminski, Assistant Director, Ron Shimabukuro, Senior Counsel, Scott Burnett, Counsel, Chief Counsel's Office, (202) 649-5490, Office of the Comptroller of the Currency, 400 7th Street SW, Washington, DC 20219. If you are deaf, hard of hearing, or have a speech disability, please dial 7-1-1 to access telecommunications relay services.

Board: Juan Climent, Deputy Associate Director, (202) 872-7526; Brian Chernoff, Manager, (202) 731-8914; Missaka Nuwan Warusawitharana, Manager, (202) 452-3461; Akos Horvath, Principal Economist, (202) 452-3048; Nadya Zeltser, Lead Financial Institution Policy Analyst, (202) 452-3164; Anthony Sarver, Senior Financial Institution Policy Analyst, (202) 475-6317, Division of Supervision and Regulation; or Jay Schwarz, Deputy Associate General Counsel, (202) 731-8852; Mark Buresh, Senior Special Counsel, (202) 499-0261; Ryan Rossner, Counsel, (202) 430-1368; Isabel Echarte, Senior Attorney, (202) 945-2412, Legal Division, Board of Governors of the Federal Reserve System, 20th and C Streets NW, Washington, DC 20551. For the hearing impaired only, Telecommunication Device for the Deaf (TDD), (202) 263-4869.

FDIC: Benedetto Bosco, Chief, Capital Policy Section; Michael Maloney, Senior Policy Analyst; Kyle McCormick, Senior Policy Analyst; Keith Bergstresser, Senior Policy Analyst; Eric Schatten, Senior Policy Analyst; Soo Jeong Kim, Policy Analyst; Matthew Park, Financial Analyst; Capital Markets and Accounting Policy Branch, Division of Risk Management Supervision; Catherine Wood, Counsel; Merritt Pardini, Counsel; Kevin Zhao, Senior Attorney; Nicholas Soyer, Attorney, Legal Division; regulatorycapital@fdic.gov, (202) 898-6888; Federal Deposit Insurance Corporation, 550 17th Street NW, Washington, DC 20429.

SUPPLEMENTARY INFORMATION:

Table of Contents

I. Introduction

A. Overview of Leverage Capital Requirements for Large Banking Organizations

B. Objective of Rulemaking

C. Overview of the Proposed Rule and Summary of Comments

D. Overview of the Final Rule

II. Final Rule

A. Changes to the Enhanced Supplementary Leverage Ratio Standards

1. Proposed Calibration and Comments Received

2. Calibration of the Holding Company Standard

3. Calibration of the Depository Institution Standard

4. Modification to the Form of the Depository Institution Standard

B. Amendments to Total Loss-Absorbing Capacity and Long-Term Debt Requirements

C. Applicability Thresholds of the eSLR Standard for OCC-Supervised Institutions

D. Comments on Other Potential Modifications to the Supplementary Leverage Ratio Requirement and Other Elements of the Agencies' Regulatory Framework

E. Technical Corrections

III. Effective Date

IV. Economic Analysis

A. Introduction

B. Baseline

1. Role of Banking Organizations as Investors in U.S. Treasury Securities

2. Treasury Securities Held by Banking Organizations Subject to Category I to III Standards

C. Policy Change

D. Reasonable Alternatives

E. Changes in the Supplementary Leverage Ratio and Tier 1 Capital Requirements

F. Benefits

G. Costs

H. Additional Comments on the Economic Analysis

1. Requests To Consider Potential Future Developments

2. Requests To Consider Potential Interaction Effects

3. Requests To Consider Further Benefits and Costs

I. Analysis of TLAC and Long-Term Debt Requirement Changes

1. Baseline

2. Changes in Requirements

3. Anticipated Economic Effects

J. Conclusion

K. Appendix

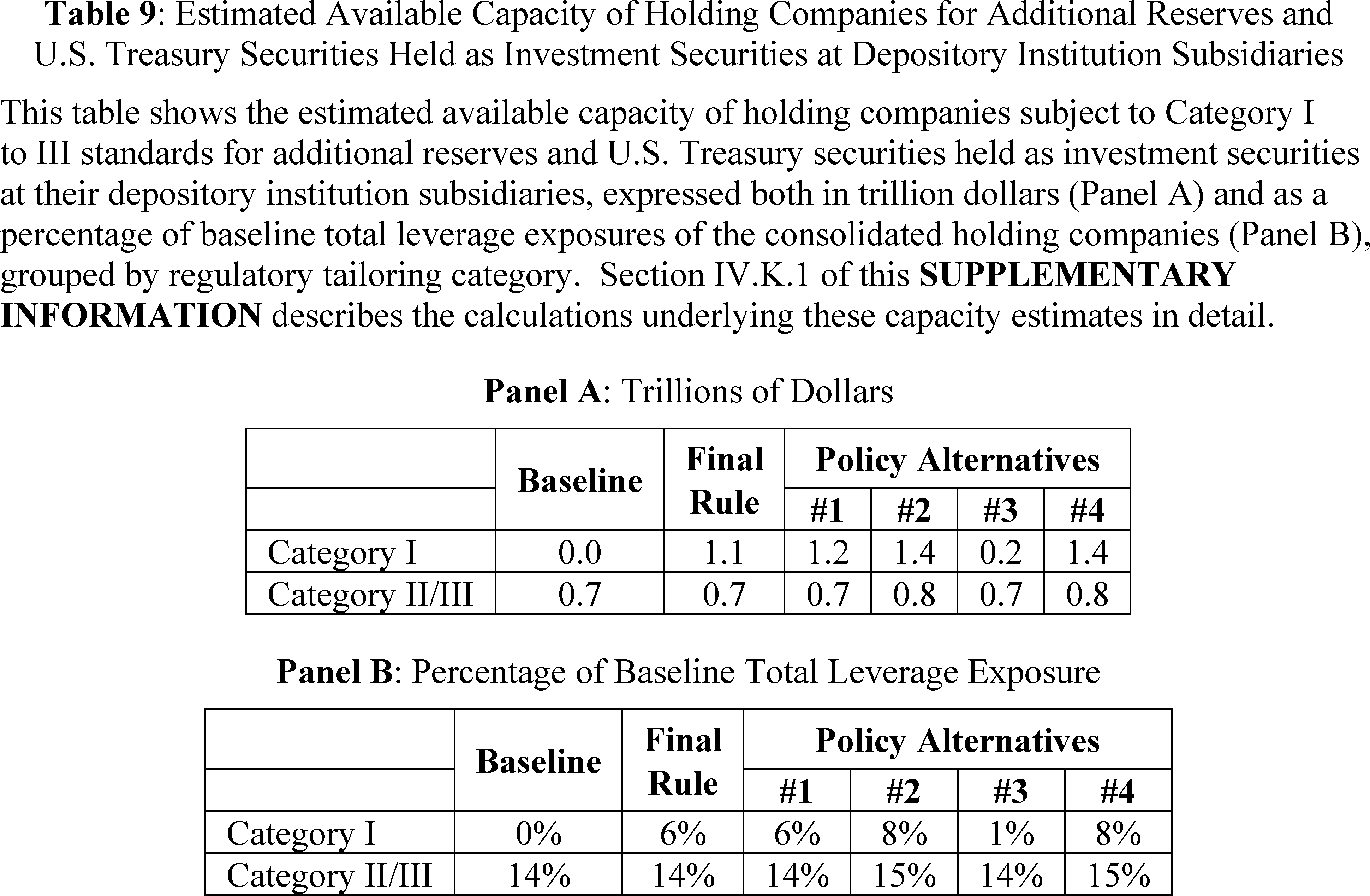

1. Estimating the Available Capacity of Holding Companies for Additional Reserves and U.S. Treasury Securities Held as Investment Securities at Depository Institution Subsidiaries ( printed page 55249)

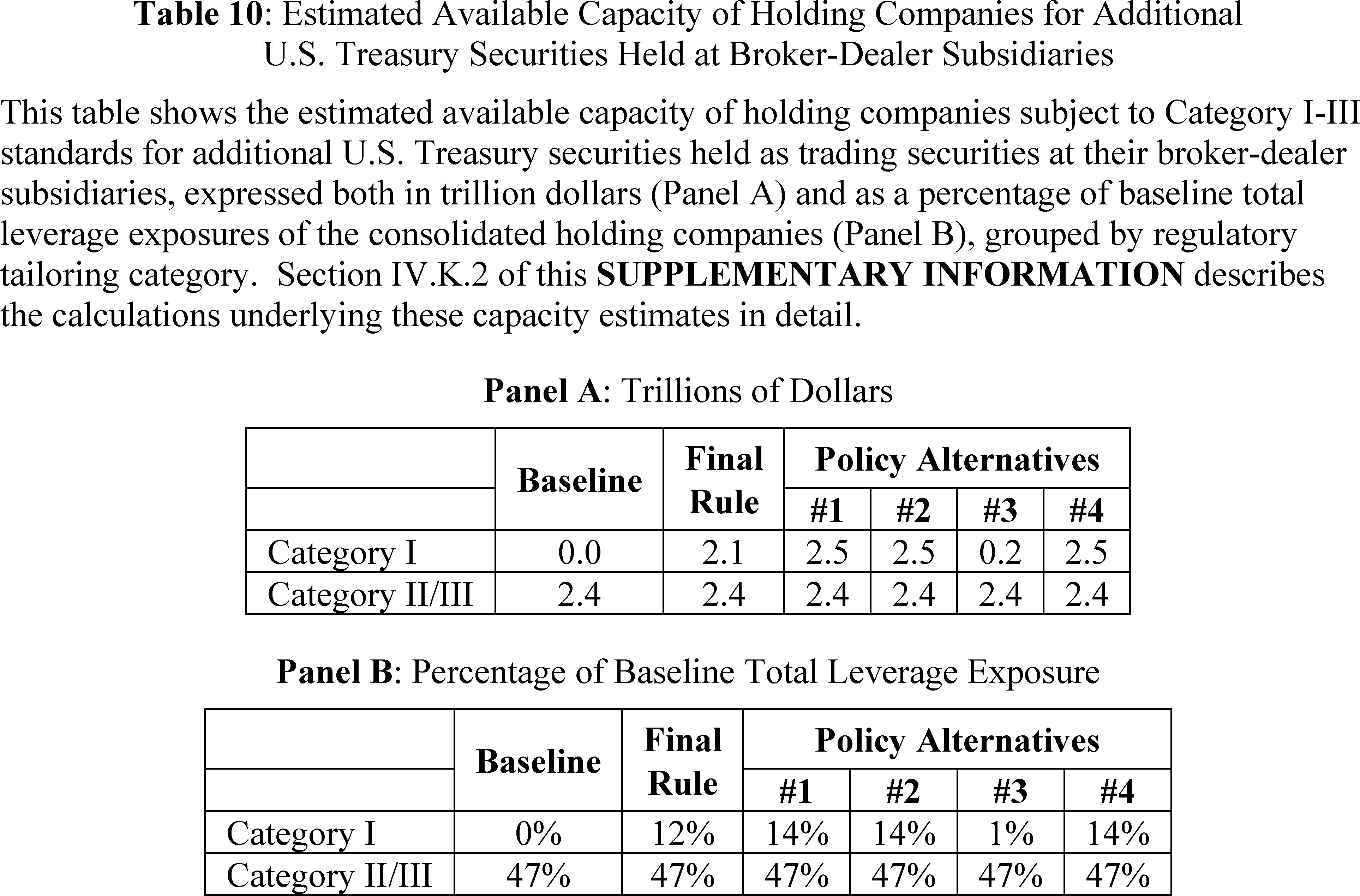

2. Estimating the Available Capacity of Holding Companies for Additional U.S. Treasury Securities Held at Broker-Dealer Subsidiaries, Assuming Perfect Hedging

V. Administrative Law Matters

A. Paperwork Reduction Act

B. Regulatory Flexibility Act Analysis

C. Plain Language

D. Riegle Community Development and Regulatory Improvement Act of 1994

E. Executive Orders 12866, 13563, and 14192

F. OCC Unfunded Mandates Reform Act of 1995

G. Congressional Review Act

I. Introduction

On July 10, 2025, the Office of the Comptroller of the Currency (OCC), Board of Governors of the Federal Reserve System (Board), and Federal Deposit Insurance Corporation (FDIC) (collectively, the agencies) published in the Federal Register a notice of proposed rulemaking (the proposal) [1] that would modify the enhanced supplementary leverage ratio (eSLR) standards that apply to U.S. bank holding companies identified as global systemically important bank holding companies (GSIBs) [2] and their subsidiary depository institutions (covered depository institutions).[3] Following review of the comments received on the proposal, the agencies are finalizing the proposed changes, with certain adjustments discussed below.

A. Overview of Leverage Capital Requirements for Large Banking Organizations

Congress has authorized the agencies to establish leverage capital requirements and standards for banking organizations subject to this final rule. Section 165 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act),[4] as amended by section 401 of the Economic Growth, Regulatory Relief, and Consumer Protection Act,[5] requires the Board to establish leverage limits for bank holding companies with $250 billion or more in total consolidated assets.[6] The prompt corrective action framework in section 38 of the Federal Deposit Insurance Act (FDI Act) requires the agencies to prescribe capital standards for insured depository institutions that include a leverage limit and provides that the agencies may establish any additional relevant capital measures to carry out the purpose of that section.[7] Various statutory authorities provide the agencies with broad discretionary authority to set capital requirements and standards for banking organizations supervised by the agencies, including national banking associations, state-chartered banks, savings associations, and depository institution holding companies.[8]

In 2013, the agencies adopted a revised regulatory capital rule to address weaknesses that became apparent during the financial crisis of 2007-09,[9] which includes two leverage-based requirements for large banking organizations.[10] The tier 1 leverage ratio, measured as the ratio of a banking organization's tier 1 capital to average total consolidated assets, applies to all banking organizations subject to the capital rule. Under this requirement, a banking organization is required to maintain a minimum leverage ratio of at least four percent; moreover, an insured depository institution is required to maintain a leverage ratio of at least five percent to be considered “well capitalized” under the prompt corrective action framework.[11] The supplementary leverage ratio, measured as the ratio of a banking organization's tier 1 capital to its total leverage exposure, applies only to banking organizations subject to Category I-III capital standards.[12] Each of these ( printed page 55250) banking organizations must maintain a supplementary leverage ratio of at least three percent. Total leverage exposure includes certain off-balance sheet exposures in addition to all on-balance sheet assets.[13]

In 2014, the agencies adopted a final rule that required GSIBs and covered depository institutions to meet enhanced supplementary leverage ratio standards.[14] Specifically, this framework requires each GSIB to maintain a supplementary leverage ratio of at least three percent plus a leverage buffer greater than two percent to avoid limitations on the GSIB's capital distributions and certain discretionary bonus payments.[15] In addition, any insured depository institution subsidiary of a GSIB must maintain a supplementary leverage ratio of at least six percent to be “well capitalized” under the prompt corrective action framework of the Board, OCC, or FDIC, as applicable.[16]

B. Objective of Rulemaking

Within the regulatory capital framework, leverage and risk-based capital requirements play complementary roles, with each addressing potential risks not addressed by the other.[17] Risk-based capital requirements that are commensurate with the risk profile of a banking organization's exposures help to encourage prudent behavior by requiring a banking organization to maintain higher levels of capital for activities and exposures that present greater risk. Historical experience, however, has demonstrated that risk-based measures alone may be insufficient to support loss-absorbing capacity at banking organizations through economic cycles. Leverage capital requirements, which do not take into account the risks of a banking organization's exposures, can help to mitigate underestimations of those risks by both banking organizations and risk-based capital requirements.[18]

As discussed in the proposal, an appropriately calibrated leverage capital requirement sets a simple and transparent limit on a banking organization's leverage. In addition, leverage capital requirements can be useful to address cases where the level of risk at a particular banking organization or across the financial system is difficult to measure. However, when a leverage capital requirement is calibrated too high and becomes a banking organization's regularly binding capital requirement, it can create incentives for the banking organization to engage in higher-risk activities in search of higher returns and to reduce participation in lower-risk, lower-return activities. A banking organization that has a leverage capital requirement as its binding capital requirement can, on the margin, replace a lower-risk asset with a higher-risk asset without a corresponding increase in its overall regulatory capital requirement.[19]

The proposal discussed, as an example, concerns that a regularly binding leverage capital requirement could disincentivize large banking organizations from intermediating in the U.S. Treasury market. Market participants have suggested that such disincentives could, under certain circumstances, impede the orderly functioning of the U.S. Treasury market and of U.S. and global financial markets more broadly.[20] As discussed further below, some commenters on the proposal echoed this concern. The U.S. Treasury market is one of the deepest and most liquid markets in the world and serves as a source of safe and liquid assets that are used for a variety of purposes in the financial markets.[21] Confidence in the efficient functioning of the U.S. Treasury market, including during times of stress, is critical to the stability of the domestic and global banking and financial systems.

As discussed in the proposal, appropriate calibration of regulatory capital requirements involves a balancing of considerations. A banking organization should maintain sufficient capital to absorb losses and continue to serve as a financial intermediary over a range of conditions. In addition, it is important that the capital framework not create potential disincentives for a banking organization to prudently engage in low-risk activities or important market functions. The agencies regularly review the regulatory capital framework to help ensure requirements are appropriate in view of evolving risks and financial innovation and that the framework is functioning as intended. In reviewing the eSLR standards, the agencies considered factors such as alignment of requirements with risks; incentives for banking organizations to perform critical financial services over a range of economic conditions; and ways to enhance the efficiency of the framework. ( printed page 55251)

C. Overview of the Proposed Rule and Summary of Comments

In light of the agencies' review of the eSLR standards and experience gained since their initial adoption, on July 10, 2025, the agencies published the proposal. The proposal would recalibrate the eSLR standards to reduce the likelihood and frequency of the eSLR standards becoming a binding capital requirement for GSIBs and covered depository institutions. The proposed recalibration of the eSLR standards sought to reduce disincentives for banking organizations to engage in lower-risk, lower-return activities, such as U.S. Treasury market intermediation, and reduce the need for temporary adjustments in the event of severe market stress, as occurred in 2020.[22]

Under the proposal, the Board proposed to recalibrate the eSLR buffer standard for GSIBs to equal 50 percent of a GSIB's method 1 surcharge calculated under the Board's GSIB surcharge framework, rather than the current leverage buffer standard of two percent.[23] Similarly, the agencies proposed to modify the eSLR standard for covered depository institutions from the current six percent “well capitalized” threshold under the prompt corrective action framework to an eSLR buffer standard equal to 50 percent of the parent GSIB's method 1 surcharge calculation, above the minimum supplementary leverage ratio requirement of three percent. The proposal also included conforming amendments to the leverage-based components of the Board's total loss-absorbing capacity and long-term debt requirements, and the OCC proposed changes to the criteria it uses to identify which national banks and Federal savings associations are subject to the eSLR standards. In addition, the Board and FDIC proposed to make certain technical corrections to the capital rule and prompt corrective action framework, and the Board proposed to make conforming amendments to relevant regulatory reporting forms.

The proposal also requested comment on potential additional or alternative approaches that could help to achieve the objectives of the proposal, including a potential exclusion of Treasury securities held for trading at broker-dealer subsidiaries (and foreign equivalents thereof) of depository institution holding companies from the denominator of the supplementary leverage ratio (the narrow exclusion approach).

The agencies received approximately 40 comments on the proposal from a range of parties, including policy advocacy groups, banking organizations, banking and financial industry trade associations, other financial market participants, academics, members of Congress, research organizations, and individuals.

Some commenters, including nearly all trade associations, large banking organizations, and other financial market participants, along with some academics and other individuals, were broadly supportive of the proposal. These commenters stated that the current eSLR standards disincentivize banking organizations from participating in a range of low-risk activities, including U.S. Treasury market intermediation and holding customer deposits. These commenters stated that the proposed modifications to the eSLR standards would increase the capacity of banking organizations to serve their clients and the broader economy across a range of low-risk activities. Some of these commenters also stated that the proposed modifications may prove especially beneficial to U.S. Treasury market intermediation and other low-risk activities during episodes of financial stress, when, these commenters stated, supplementary leverage ratio requirements are more likely to become a binding capital constraint. Some of these commenters urged the agencies to promptly finalize and implement the proposal.

Other commenters, including advocacy groups, members of Congress, a trade group for community banking organizations, academics, and individuals, objected to the proposal. These commenters generally asserted that the proposal would significantly weaken the existing capital framework for GSIBs and covered depository institutions and increase risks to the safety and soundness of banking organizations, the banking system, and overall financial stability. Some of these commenters also asserted that the agencies should not adopt the proposal because, in these commenters' view, the proposed changes would not aid U.S. Treasury market intermediation. Instead, these commenters asserted that banking organizations would choose to allocate extra capital capacity created by the proposal to other higher-risk activities or to distribute extra capital to shareholders, thereby putting banking organizations and the Deposit Insurance Fund at greater risk while not improving Treasury market intermediation. Additionally, one commenter argued that the proposal would give preferential treatment to GSIBs relative to other banking organizations and undermine the competitive position of smaller banking organizations.

The agencies also received comments regarding specific aspects of the proposal discussed further below.

D. Overview of the Final Rule

The agencies are finalizing the proposal, with some modifications. The final rule recalibrates the eSLR standard for GSIBs as proposed. For covered depository institutions, the final rule includes a change from the proposal based on comments received. Specifically, the final rule adopts an eSLR buffer standard equal to 50 percent of a covered depository institution's parent GSIB's method 1 surcharge, capped at 1 percent. The eSLR buffer standard will apply in addition to the three percent supplementary leverage ratio minimum requirement.

The final rule also implements the proposed changes to the leverage-based components of the total loss-absorbing capacity and long-term debt requirements for GSIBs without modification. The final rule does not adopt the proposed criteria that the OCC would have used to determine applicability of the eSLR standard for OCC-supervised institutions. Further, the agencies are not including in the final rule any additional modifications to the supplementary leverage ratio ( printed page 55252) requirement, such as the narrow exclusion approach discussed in the proposal, or changes to other elements of the agencies' regulatory framework requested by some commenters. The final rule adopts technical corrections to the capital rule and changes to the prompt corrective action framework consistent with the proposal. The final rule includes an effective date of April 1, 2026, with the optional early adoption of the final rule's modified eSLR standards beginning January 1, 2026. This SUPPLEMENTARY INFORMATION also presents the economic analysis of the final rule's changes and discusses administrative law matters.

II. Final Rule

A. Changes to the Enhanced Supplementary Leverage Ratio Standards

1. Proposed Calibration and Comments Received

The proposal would have recalibrated the eSLR buffer standard for GSIBs to equal 50 percent of a GSIB's method 1 surcharge calculated under the Board's GSIB surcharge framework, rather than the current leverage buffer standard of two percent. Similarly, the proposal would have modified the eSLR standard for covered depository institutions from the current six percent “well capitalized” threshold under the prompt corrective action framework to an eSLR buffer standard equal to 50 percent of the parent GSIB's method 1 surcharge calculation.[24] As a result, the eSLR standards would have been the same in both form and calibration at the bank holding company and subsidiary depository institution levels.

The agencies received a number of comments on the proposed modifications to the eSLR standards. Many commenters strongly supported recalibrating the eSLR standards to help ensure that this requirement serves as a backstop to risk-based capital requirements, rather than a frequently binding constraint. These commenters stated that a regularly binding leverage ratio requirement disincentivizes banking organizations from participating in low-risk, low-return activities, such as intermediation in the U.S. Treasury market, and more broadly decreases the capacity of banking organizations to perform critically important functions across a range of low-risk activities, particularly in periods of stress. Some of these commenters further stated that recalibrating the current eSLR buffer of two percent to a buffer that is equal to 50 percent of a GSIB's method 1 surcharge would help ensure that the eSLR standards serve as a backstop to risk-based capital requirements and increase the capacity of GSIBs to engage in low-risk activities, including U.S. Treasury market intermediation. Some of these commenters also asserted that GSIBs would continue to have strong levels of capital, while being more capable of effectively allocating capital within their organizations.

Conversely, many commenters opposed the proposed modifications to the calibration of the eSLR standards, with some commenters stating the agencies should withdraw the proposal. Some of these commenters argued that the proposal did not provide sufficient justification or rationale for the recalibration. Some commenters also asserted that the proposed changes would reduce the eSLR standards by too much relative to risk-based capital requirements, such that supplementary leverage ratio requirements would not serve as a meaningful backstop to risk-based requirements, or disagreed with the idea that the eSLR standards should serve as a backstop rather than a regularly binding constraint. In these commenters' views, the eSLR standards should serve a more primary or equal role relative to risk-based capital requirements, in order to better address risks not well addressed by risk-based capital requirements. For example, some commenters asserted that the risk-based capital framework has many shortcomings and does not sufficiently capture credit and interest rate risks of U.S. Treasury securities or risks related to off-balance sheet exposures. Therefore, in these commenters' view, the supplementary leverage ratio requirement serves as a simple and important requirement to help mitigate such risks, which, in turn, promotes the safety and soundness of the banking system and the financial system more broadly. Additionally, one commenter asserted that leverage capital requirements must be binding in some cases to ensure such requirements are effective.

Some commenters asserted that declines in capital requirements resulting from the proposed changes to the eSLR standards would undermine banking organizations' ability to lend during economic downturns or periods of financial stress, particularly if the agencies also reduce risk-based capital requirements in the future. Some commenters also stated that reductions in capital at GSIBs as a result of the proposal would increase the risks of bank failures and financial crises. Several commenters expressed concerns that the proposal would advantage the largest banking organizations over community and regional banking organizations.

Some commenters suggested alternative approaches to the proposal that the agencies should consider that, in these commenters' views, would help ensure the safety and soundness of banking organizations, alter the incentives arising from capital requirements, or achieve other objectives of the proposal. One commenter suggested that agencies should increase risk-based capital requirements to address the incentive concerns, rather than lowering the eSLR standards, and some commenters stated that the agencies should generally increase capital requirements, including leverage capital requirements. Some commenters suggested that the agencies could make the eSLR buffer standards more countercyclical, such as by adopting a mechanism that would temporarily lower the eSLR buffer standards in periods of stress.

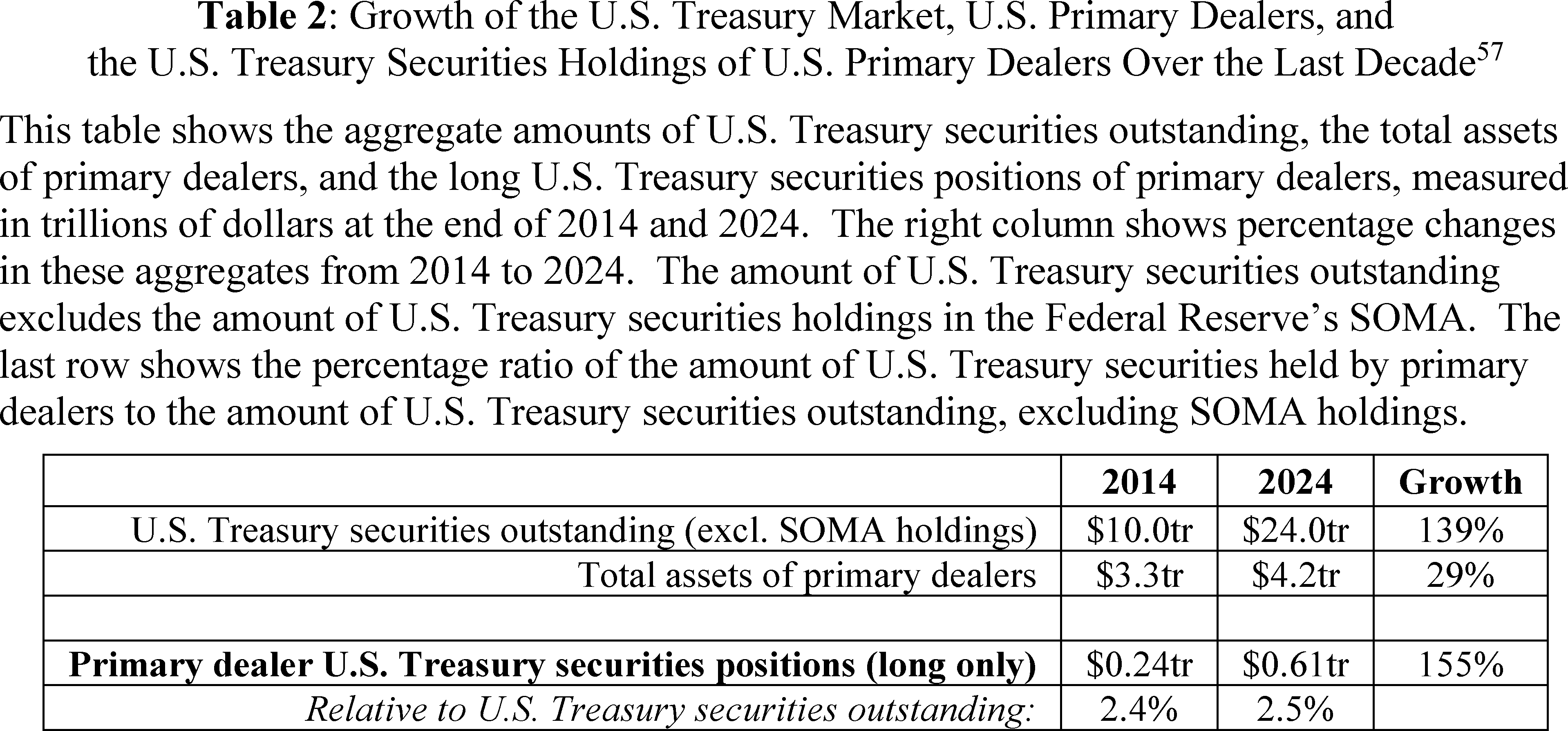

Several commenters supported the proposal because, in these commenters' view, it would reduce regulatory disincentives for GSIBs to participate in low-risk, low-return businesses, such as U.S. Treasury market intermediation, and welcomed the agencies' proposed modifications to the eSLR standards as a change that would reduce costs of intermediating in the U.S. Treasury market. These commenters expressed concerns with the current bindingness of the eSLR standards and its effects on U.S. Treasury market intermediation, other low-risk activities, and the broader financial system. Commenters supportive of the proposal stated that a binding supplementary leverage ratio requirement has an adverse impact on intermediation in the U.S. Treasury market by constraining the activities of GSIBs' broker-dealers, particularly during periods of stress, when GSIBs may face additional balance sheet constraints due to such factors as deposit inflows, increased demand for Treasury market intermediation, and changes in the aggregate level of deposits at Federal Reserve Banks.[25] Some commenters stated that lower-risk assets have increased proportionally with banking organizations' balance sheets over the past decade, driven in ( printed page 55253) part by increased overall levels of Treasury security issuance and deposits at Federal Reserve Banks; these commenters stated these developments have caused the supplementary leverage ratio requirement to become more binding over time. One commenter asserted that, when the agencies originally calibrated the eSLR standards, the agencies underestimated growth in the supply of these assets, resulting in supplementary leverage ratio requirements becoming regularly binding in a manner that was not intended.

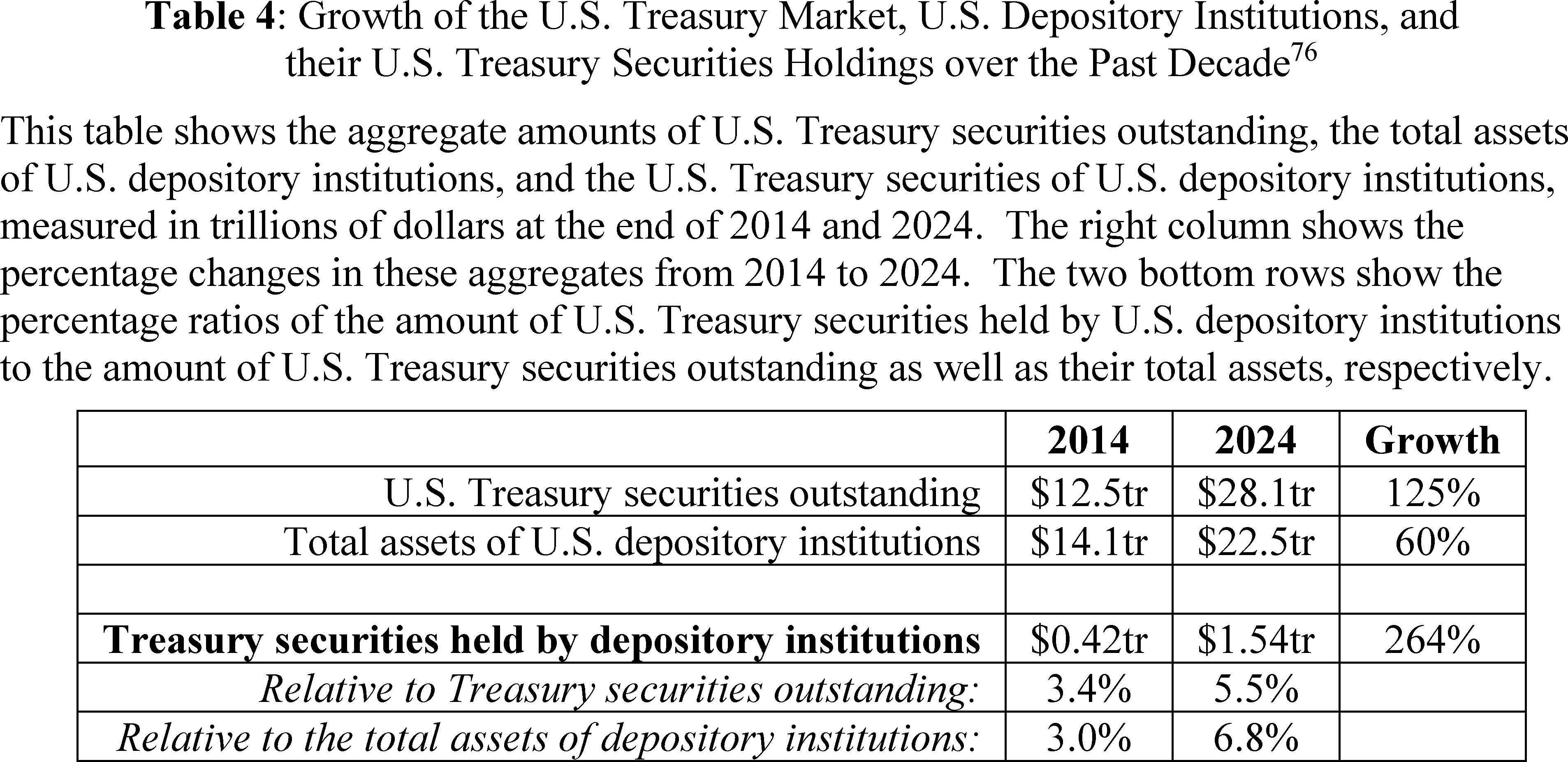

In contrast, some commenters asserted that the agencies should not adopt the proposed changes because, in the view of these commenters, there is not sufficient evidence that the supplementary leverage ratio is a binding requirement that constrains GSIBs' U.S. Treasury market intermediation or that the proposal would support U.S. Treasury market intermediation. These commenters asserted that banking organizations have sufficient capacity under the current supplementary leverage ratio requirement to engage in Treasury market intermediation and can, in periods of stress, use their buffers to absorb any increased demand for Treasury market intermediation. One commenter stated that insured depository institutions and primary dealers have more than doubled their exposure to U.S. Treasury securities relative to other assets in the last decade, which, in the view of this commenter, indicates that the proposed changes to the eSLR standards are not necessary.

Some commenters asserted that the agencies should not adopt the proposed changes because other measures could help promote Treasury market intermediation, such as increased central clearing of U.S. Treasury security-related transactions, improvements to data quality, enhancements to market transparency, and examination of the effects of risk management practices. Some commenters also asserted that increased central clearing of U.S. Treasury security-related transactions could provide additional balance sheet capacity for banking organizations due to netting benefits, which some of these commenters asserted would reduce the need for the proposal, whereas another commenter saw the proposal as beneficial to Treasury market intermediation notwithstanding developments in central clearing. Several commenters asserted that large holdings of U.S. Treasury securities could pose risks to banking organizations because the risks of these assets may not be sufficiently captured by risk-based capital requirements. Another commenter suggested that recent issues in U.S. Treasury markets relate primarily to the sustainability of fiscal deficits rather than the capital framework for banking organizations. Certain commenters expressed concern that the objective of the proposal was to reduce government borrowing costs, rather than the objectives stated in the proposal. Some commenters expressed concerns that banking organizations would elect not to use available capital to facilitate Treasury market intermediation, and some asserted that banking organizations would instead increase capital distributions to shareholders or engage in riskier activities, such as lending to hedge funds.

The agencies also received comments on the proposed use of the Board's GSIB surcharge framework to determine eSLR buffer standards. Several commenters supported using the GSIB surcharge framework to calibrate the eSLR buffer standard and more specifically supported the use of a GSIB's method 1 surcharge. These commenters stated that this calibration methodology would appropriately achieve the proposal's objective to help ensure that the supplementary leverage ratio requirement serves as a backstop to risk-based capital requirements, rather than a binding constraint. Some commenters also noted the benefit of consistency in the eSLR standards for GSIBs with the leverage ratio framework published by the Basel Committee on Banking Supervision (Basel Committee) and with the implementation of these requirements in other jurisdictions.[26]

Several commenters supportive of the proposed recalibration also recommended capping the eSLR buffer at the current level of two percent to help ensure that the supplementary leverage ratio requirement continues to appropriately function as a backstop to risk-based capital requirements should a banking organization's method 1 surcharge increase in the future. Specifically, these commenters asserted that the proposed approach might result in an eSLR buffer standard that, in the view of these commenters, could be inappropriately high, which these commenters stated would be contrary to the intent of the proposed recalibration. According to these commenters, capping the eSLR buffer standard at a fixed amount, such as two percent, would mitigate the potential for constraints in U.S. Treasury market and other intermediation activities if increases over time in the method 1 surcharge calculation flow through to the eSLR calibration. Conversely, one commenter asserted that it is important that GSIBs with surcharges above four percent would be subject to the eSLR buffers above two percent to reflect their higher risk profiles.

Other commenters opposed the proposed use of the Board's GSIB surcharge framework to calculate the eSLR buffer standards. Some of these commenters asserted that using the GSIB surcharge framework to establish a firm's eSLR buffer standard would undermine key features of the eSLR standard as a leverage requirement, such as its relative simplicity and its insensitivity to risk. In these commenters' view, leverage capital requirements are designed to operate independently of risk assessments and therefore integrating the risk-based GSIB surcharge methodology into a risk-insensitive leverage capital requirement would not be prudent. Some commenters also asserted that the proposed calibration based on a GSIB's method 1 surcharge would introduce unnecessary complexity because this approach would differ from the Board's GSIB risk-based surcharge framework, which uses the higher of a GSIB's method 1 or method 2 surcharges. One commenter asserted that use of a GSIB's method 1 surcharge would not be appropriate because potential variations in the method 1 surcharge could be driven by changes to aggregate global indicator amounts used in the method 1 calculation, which incorporate data provided to the Basel Committee by foreign banking organizations. This commenter stated that the relevance of certain foreign banking organization indicators in measuring the riskiness of U.S. banking organizations is unclear.

One commenter asserted that setting the eSLR buffer annually based on a GSIB's most recent GSIB surcharge could introduce unnecessary volatility. This commenter suggested calculating simple averages for the last two years and phasing in any change equally over two consecutive quarters to mitigate any ( printed page 55254) volatility in the GSIB surcharges. Some commenters suggested alternative methodologies for the calibration of the eSLR buffer, such as using the higher of a GSIB's method 1 or method 2 surcharge, only using a method 2 surcharge with a multiplier, developing a new methodology, or establishing a one percent minimum floor to ensure that the eSLR buffer would not fall below one percent of total leverage exposure. One commenter suggested that the agencies should apply a distinct calibration to GSIBs that are heavily involved in custody activities, to reflect the exclusions applicable for deposits at the Federal Reserve and certain other central banks that are linked to fiduciary or custodial and safekeeping accounts from the denominator of the supplementary leverage ratio.[27]

Some commenters raised concerns regarding the agencies' statutory authority to implement the proposed changes, including assertions that the agencies were not permitted to consider burden, efficiency, or U.S. Treasury market functioning when establishing capital requirements. In addition, another commenter asserted that the proposed changes would result in the eSLR standards becoming less stringent than requirements applicable to banking organizations with a lesser systemic risk profile, which the commenter asserted was not permitted under provisions of the Dodd-Frank Act. Another commenter asserted that provisions of the Dodd-Frank Act and FDI Act require the agencies to ensure that their risk-based and leverage capital requirements are both binding and effective.

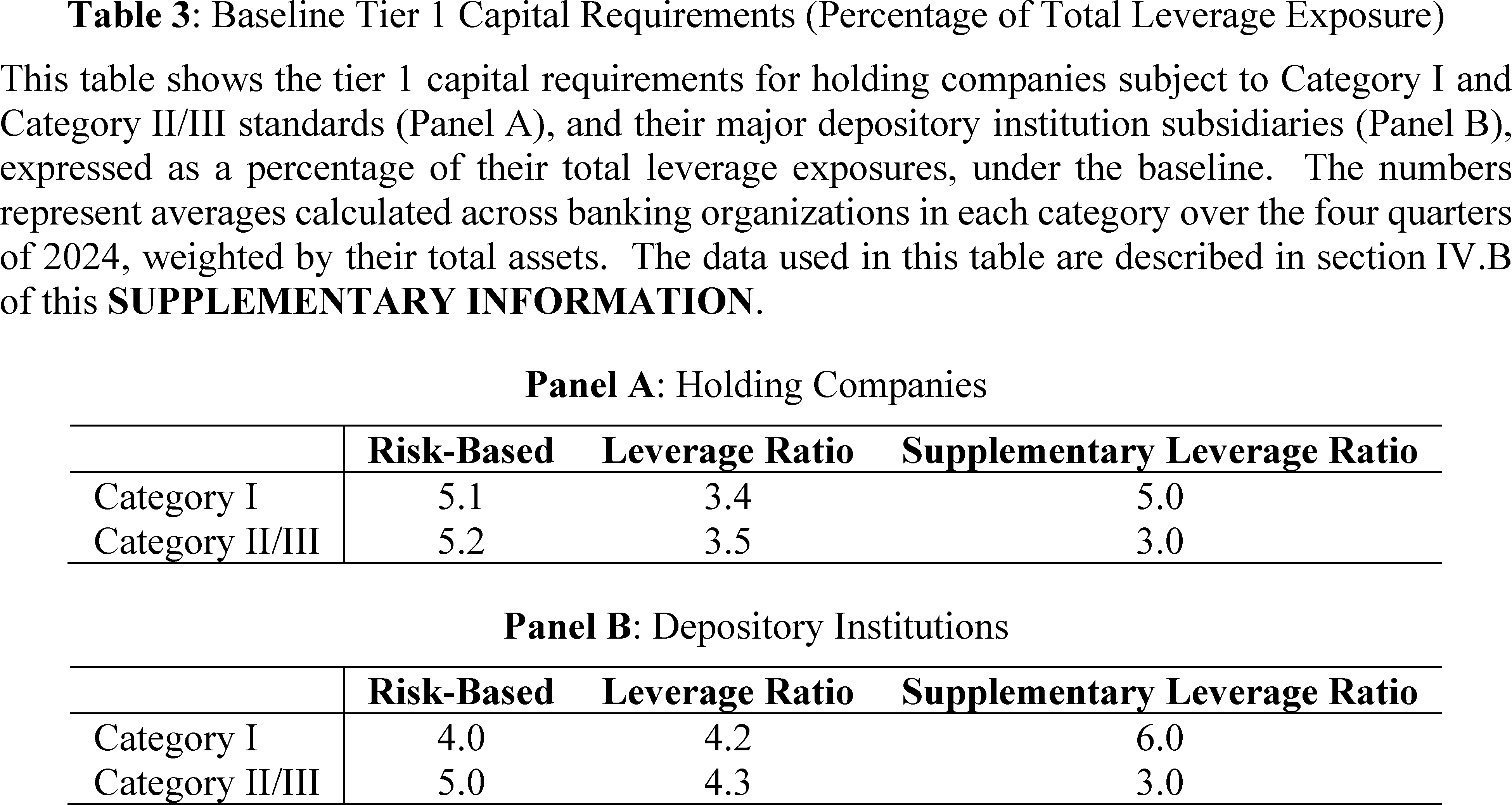

As discussed in section I.A of this SUPPLEMENTARY INFORMATION , Congress has granted the agencies with authority to establish leverage capital requirements and standards for banking organizations subject to this final rule. The agencies regularly review and may implement changes to improve the effectiveness of their regulations, including to minimize unintended, adverse consequences or interactions, while continuing to achieve the intended effects. The agencies note that the eSLR standards exceed leverage capital requirements applicable to less systemically important firms, as the eSLR buffer standard is additive to the supplementary leverage ratio minimum requirement of three percent that also applies to banking organizations subject to Category II and III capital standards. Moreover, GSIBs and covered depository institutions will remain subject to tier 1 leverage ratio requirements. Both risk-based and leverage requirements will continue to have an impact on decision making. For example, there are business models and market conditions that could result in the eSLR standards and supplementary leverage ratio, along with the tier 1 leverage ratio, becoming binding constraints for certain banking organizations. Indeed, as discussed in section IV.E of this SUPPLEMENTARY INFORMATION , the agencies estimate that some covered depository institution subsidiaries are still expected to have higher supplementary leverage ratio requirements than risk-based requirements.

In addition to the comments discussed above, the agencies also received comments that specifically discuss proposed changes to covered depository institutions, as discussed in more details in section II.A.3 of this SUPPLEMENTARY INFORMATION .

As discussed below, the agencies are finalizing the proposal with some modifications to the calibration of the eSLR standards for covered depository institutions.

2. Calibration of the Holding Company Standard

After reviewing the comments, the Board is adopting as final the recalibration of the eSLR buffer standard for GSIBs to equal 50 percent of a GSIB's method 1 surcharge. This recalibration is important to help mitigate potential disincentives for GSIBs to engage in low-risk, low-return, balance-sheet-intensive activities, such as intermediation by GSIBs' broker-dealer subsidiaries in markets for Treasury securities, and from holding low-risk assets in general. As many commenters observed, a regularly binding supplementary leverage ratio requirement can create disincentives for banking organizations to engage in low-risk, low-return activities and may contribute to increased volatility and reduced liquidity in U.S. Treasury markets during periods of stress. GSIBs play a key role in supporting market liquidity and providing financing in Treasury markets, as discussed in section IV of this SUPPLEMENTARY INFORMATION .[28]

As noted above, many commenters stated that the agencies should not change the eSLR standards to create additional demand for U.S. Treasury securities, or that the agencies should not adopt the proposed changes to enhance U.S. Treasury market functioning when, in the view of the commenters, other regulatory changes or measures could directly achieve such an outcome. While the agencies expect the final rule to reduce unintended disincentives for GSIBs to intermediate in the U.S. Treasury market,[29] the primary purpose of the final rule is not to support increased U.S. Treasury market issuance or substitute for other regulatory or private sector efforts that more directly seek to target U.S. Treasury market structure or functioning, as some commenters suggested. Rather, the final rule seeks to calibrate the eSLR standards such that they serve as a backstop to risk-based capital requirements, rather than a regularly binding capital constraint, to address the potential negative incentive effects that can occur when a leverage requirement is too frequently binding or near-binding. Furthermore, and importantly, while the final rule seeks to reduce regulatory disincentives for low-risk activities, the final rule does not create preferences for certain low-risk activities over others.

As some commenters noted, the use of method 1 to calculate the eSLR buffer standard for GSIBs would incorporate the use of a risk-based indicator methodology to determine the calibration of a risk-insensitive leverage requirement. Such an approach, however, results in the application of more stringent requirements to banking organizations that present the greatest systemic risks. It is also consistent with the methodology used in the Board's existing regulatory framework to determine whether a bank holding company is a GSIB, and therefore whether it is subject to the eSLR standards under both the current and final rule.[30] The use of a risk-based measure to determine application of a leverage requirement is also consistent with other parts of the agencies' regulatory tailoring framework, which, for example, uses indicators of risk to determine the application of the supplementary leverage ratio requirement.[31] Importantly, the GSIB surcharge is risk-based in the sense that it is based on the risks that the failure of a systemically important bank ( printed page 55255) holding company could present to the stability of the financial system, which is different from the risk-based capital requirements' differentiation of exposures by risk presented to the banking organization by each exposure.[32] The final rule determines a GSIB's eSLR buffer standard based on its systemic footprint and therefore subjects such systemically important banking organizations to more stringent capital requirements.

The final rule's calibration of the eSLR standard based on the GSIB surcharge framework also helps promote consistency in the eSLR standards for large, complex, and internationally active banking organizations across jurisdictions, as it is consistent with the leverage ratio framework published by the Basel Committee. International consistency can enhance the resilience of the U.S. financial system by limiting the potential for a global “race to the bottom” on prudential standards and reduce the likelihood of financial distress in foreign jurisdictions having negative effects in the United States.[33] In addition, international consistency of banking regulations, in general and where appropriate, can help to reduce compliance costs and barriers to market entry for banking organizations that operate across jurisdictions.

The final rule does not base the calibration of a GSIB's eSLR buffer standard on the higher of its method 1 or method 2 surcharge as some commenters advocated. As discussed in the proposal, using a GSIB's method 1 surcharge produces a generally lower calibration that meets the objective for leverage capital requirements to act as a backstop to risk-based capital requirements, and it is consistent with the leverage ratio framework published by the Basel Committee.

The final rule's calibration of the eSLR standard for GSIBs does not include a cap, as suggested by some commenters. The Board considers the final rule's calibration of the eSLR standard to be appropriate, as it correlates with the systemic footprint of a GSIB at the consolidated level and achieves the goals of the rule.

The Board does not consider it appropriate to apply, as one commenter suggested, a different eSLR standard calibration for GSIBs with significant custodial activity than would apply to other GSIBs. Under the current rule, uniform calibrations of the eSLR standards apply to GSIBs and covered depository institutions, respectively. No adjustment to the calibration of the eSLR standards applies for banking organizations that are predominantly engaged in custody, safekeeping, and asset servicing activities (custodial banking organizations), which are subject to a modified supplementary leverage ratio calculation as required by section 402 of the Economic Growth, Regulatory Relief, and Consumer Protection Act. The final rule would not change this aspect of the current rule.[34]

The Board expects the final rule's recalibration of the eSLR standard for GSIBs will reduce disincentives for these banking organizations to participate in low-risk, balance sheet-intensive activities that are important for the functioning of the banking system and the financial system more broadly, while generally not materially changing the amount of capital in the banking system.[35] However, because GSIB risk-based capital requirements and buffers fluctuate over time in response to changes in stress test results and other factors, the effect of recalibrating the eSLR standard on capital requirements will vary over time and may result in more or less material changes in overall capital requirements. Additionally, although the final rule is intended to calibrate the eSLR standards to serve as a backstop to risk-based capital requirements rather than as a constraint that is frequently binding, the eSLR standards may nonetheless, in certain circumstances, serve as the binding constraint. As discussed in section IV of this SUPPLEMENTARY INFORMATION , the supplementary leverage ratio is currently the binding tier 1 capital requirement for almost all GSIBs, creating unintended incentives and rendering tier 1 capital requirements less risk sensitive. The agencies estimate that the final rule will achieve the objective of making the supplementary leverage ratio requirement a backstop to risk-based capital requirements for all GSIBs.

The Board is not adopting modifications to the eSLR standards that would cause them to automatically change over economic cycles or specifically during periods of stress, as recommended by some commenters. As discussed in section IV.F of this SUPPLEMENTARY INFORMATION , the final rule's approach would provide significant capacity for banking organizations to engage in low-risk, balance-sheet intensive activities, including during periods of economic or financial market stress. Moreover, as the agencies have previously emphasized, capital buffers are designed to be used in times of stress.[36]

3. Calibration of the Depository Institution Standard

The proposal would have modified the six percent eSLR standard applicable to a covered depository institution to instead be an eSLR buffer standard equal to 50 percent of its parent GSIB's method 1 surcharge as determined under the Board's GSIB surcharge framework in addition to the minimum supplementary leverage ratio requirement of three percent. As described in the proposal, this approach would have resulted in a lower eSLR standard for most covered depository institutions. It also would have produced a dynamic standard that could change from year-to-year for each banking organization subject to the eSLR standard.

Commenters expressed a range of views on the proposed eSLR calibration for covered depository institutions, in addition to the comments discussed in section II.A.1 of this SUPPLEMENTARY INFORMATION . Commenters supportive of the proposal mostly supported the proposed modification to the eSLR standard for covered depository institutions, as it would support the objective of an eSLR standard that generally serves as a backstop to risk-based capital requirements and reduce disincentives for low-risk activities, similar to the views on the proposed ( printed page 55256) modification to the eSLR standard for GSIBs. These commenters also generally supported aligning the proposed eSLR standard for covered depository institutions with the proposed GSIB eSLR standard because, in their view, having a consistent standard at the parent and bank-subsidiary levels would allow GSIBs to more flexibly manage capital allocation throughout their organizations. One commenter supportive of the proposal noted that banking organization affiliates other than broker-dealers also engage in activities related to U.S. Treasury market intermediation, including depository institutions that hold Treasury securities for investment, liquidity, or risk management, and engage in repurchase and reverse repurchase agreements collateralized by Treasury securities, such as inter-affiliate transactions for funding and collateral. This commenter stated that custodian and trust affiliates also provide services related to U.S. Treasury markets, such as safekeeping, settlement, collateral management, and facilitation with central counterparties. This commenter further stated that the proposal would help reduce constraints on these entities' capacity to conduct such activities.

As discussed above, some commenters that were generally supportive of the proposal also asserted that the variable standard that could result from using the risk-based surcharge applicable to GSIBs might result in inappropriately high eSLR standards in certain cases, which would be contrary to the intent of the proposed recalibration. To avoid such an outcome, these commenters suggested capping the eSLR standard at a fixed amount. According to these commenters, capping the eSLR standard would mitigate the potential for constraints in U.S. Treasury market and other intermediation activities that could result if increases in the GSIB risk-based surcharge calculation over time flow through to the eSLR calibration.

Other commenters asserted that the proposed eSLR standard for covered depository institutions would undermine such institutions' safety and soundness and increase the risk of bank failure, especially in light of the expected decrease in required tier 1 capital levels at covered depository institutions. Some of these commenters expressed concerns that the decrease in capital could pose risks to the Deposit Insurance Fund and would reduce loss-absorbing capacity of GSIBs and covered depository institutions. Some of these commenters also asserted that such concerns would not be mitigated by smaller changes in tier 1 capital requirements for GSIBs because, these commenters asserted, GSIBs may not be well positioned to support the financial condition of their depository institution subsidiaries in the event of stress. Some of these commenters also noted that depository institutions facing a capital shortfall in a downturn are less able or likely to continue lending to customers over the course of the economic cycle. Certain commenters expressed concern that the proposal would increase the risks arising from insured depository institutions holding more U.S. Treasury securities, asserting that this increase would pose risks similar to those that impacted banking organizations and financial markets during the 2010-12 Eurozone sovereign debt crisis. Other commenters stated that the proposal to reduce the eSLR standards for covered depository institutions would not improve Treasury market intermediation because that activity is conducted through broker-dealers.

Some commenters criticized the use of the method 1 GSIB surcharge in the proposed eSLR standard for covered depository institutions. One commenter asserted that the agencies should not adopt this approach because it would calibrate the eSLR standard based on factors measured at the holding company level that may diverge substantially from the measurement of such risk factors for depository institutions, especially where such depository institutions have limited direct international activities. As such, in this commenter's view, the proposed eSLR buffer standard may not appropriately reflect the risks and business models of covered depository institutions. The same commenter also asserted that using a systemic risk measure, such as a GSIB's method 1 surcharge, for the leverage capital requirements but not the risk-based capital requirements of covered depository institutions would create inconsistency in the regulatory capital framework.

After reviewing the comments and considering the potential impact of reducing the eSLR standard for covered depository institutions, the agencies have decided to adopt an eSLR buffer standard applicable to covered depository institutions equal to 50 percent of a covered depository institution's parent GSIB's method 1 surcharge, capped at one percent.[37] The cap recognizes that the method 1 surcharge of a parent GSIB may be in part driven by activities outside of the covered depository institution. As such, the agencies consider it appropriate to limit the role that a depository institution's affiliates play in sizing capital requirements applicable to the depository institution itself.

In addition, because covered depository institutions, unlike GSIBs, are not subject to the GSIB risk-based capital surcharge or the stress capital buffer requirement, the final rule's capped approach helps to better ensure that the eSLR standard serves as a backstop to risk-based capital requirements for covered depository institutions, as compared to an uncapped approach. Moreover, compared to the proposal, imposing a cap of one percent would have a similar aggregate impact on capital requirements based on covered depository institutions' current assets and exposures. Therefore, this approach supports the objectives of establishing the eSLR standard for covered depository institutions that serves as a backstop to risk-based capital requirements, rather than as a frequently binding requirement.

Under the final rule, covered depository institutions must maintain the eSLR buffer in addition to the minimum supplementary leverage ratio of three percent to avoid restrictions on capital distributions and certain discretionary bonus payments. In addition, insured depository institutions must maintain the three percent minimum supplementary leverage ratio to be considered “adequately capitalized” under the prompt corrective action framework, as discussed further in section II.A.4 of this SUPPLEMENTARY INFORMATION .

The final rule does not adopt an adjustment to the eSLR standard calibration for covered depository institutions that are custodial banking organizations, as suggested by one commenter. As discussed above for the eSLR standard for GSIBs, no such adjustment to the eSLR standards applies under the current rule, and the final rule does not change this approach for covered depository institutions.

As discussed in section IV of this SUPPLEMENTARY INFORMATION , the agencies estimate that the final rule will set the level of the supplementary leverage ratio requirement below the level of the risk-based tier 1 capital requirement for the majority of major ( printed page 55257) covered depository institutions.[38] Accordingly, the recalibrated eSLR buffer standard under the final rule generally achieves the objective of adjusting the eSLR standard so that it better serves as a backstop to risk-based capital requirements for covered depository institutions. As discussed above and consistent with the objective of the proposal, reducing the eSLR buffer for covered depository institutions reduces disincentives for these banking organizations to participate in low-risk, low-return activities.

The final rule's calibration would result in a reduction in the level of covered depository institutions' tier 1 capital requirements.[39] Under the agencies' current prompt corrective action framework, covered depository institutions must maintain a level of tier 1 capital to be considered “well capitalized” that is higher than the level required by the risk-based capital framework for these depository institutions. The final rule would improve the alignment of the eSLR standards for covered depository institutions with their risk-based capital requirements, which take into account these entities' risk profiles. In so doing, the final rule would help to reduce the negative incentive effects that can result when leverage requirements, rather than risk-based capital requirements, are too frequently binding. The final rule would not change the risk-based capital requirements of covered depository institutions.

In addition, although the capital requirements of covered depository institutions would decrease, the capital requirements applicable to GSIBs generally would remain near their present level, with better incentive effects from leverage-based requirements declining below risk-based requirements.[40] As a consequence, the final rule would not materially alter the ability of these consolidated banking organizations to distribute capital to shareholders. Under the final rule, GSIBs would have greater flexibility in allocating capital among different subsidiaries and would continue to be required to act as a source of strength for their depository institution subsidiaries, including in the event of financial stress.

4. Modification to the Form of the Depository Institution Standard

The proposal would have removed the eSLR threshold for a covered depository institution to be considered “well capitalized” under the prompt corrective action framework and instead implemented the eSLR as a buffer standard for covered depository institutions.

The prompt corrective action framework establishes capital categories at which an insured depository institution will become subject to increasingly stringent limitations on its activities.[41] Among other measures, the prompt corrective action framework includes a three percent supplementary leverage ratio threshold for any insured depository institution subject to Category I-III capital standards to be considered “adequately capitalized.” Until the adoption of the eSLR standards in 2014, the prompt corrective action framework did not specify a corresponding supplementary leverage ratio threshold at which such an insured depository institution subsidiary would be considered “well capitalized.” The 2014 eSLR standards established a six percent supplementary leverage ratio threshold at which covered insured depository institution subsidiaries of the largest and most complex banking organizations would be considered “well capitalized.”

The proposal would have removed the six percent supplementary leverage ratio threshold from the definition of “well capitalized” in the prompt corrective action framework and instead would have implemented the eSLR standard for covered depository institutions as a regulatory capital buffer. If a covered depository institution's supplementary leverage ratio dropped below the buffer amount, under the proposal, the institution would become subject to increasingly strict limitations on its ability to make certain capital distributions, including the issuance of dividends, and to pay certain discretionary bonuses. This approach would have aligned the form of the depository institution eSLR standard with that of the holding company eSLR standard.

Some commenters expressed strong support for the proposal to remove the eSLR standard from the prompt corrective action framework. These commenters noted that implementing the eSLR as a regulatory capital buffer at both the holding company and covered depository institution levels would better harmonize the standards and promote more coherent capital management across consolidated GSIB organizations. These commenters also stated that the buffer approach would ensure that regulators maintain flexibility necessary for dealing with a depository institution with decreasing capital. The commenters stated a buffer would act as an early warning and trigger changes in a banking organization's capital management before more severe consequences of the prompt corrective action framework apply.

One commenter supported the proposed change and advocated for removing all leverage-based thresholds from the prompt corrective action framework, based on a view that the prompt corrective action framework should be based only on risk-based capital measures. This commenter stated that adopting a buffer approach that would only impose limits on distributions, rather than the more severe limitations included in the prompt corrective action framework, would help ensure the eSLR standard serves as a backstop to the risk-based capital rules.

After reviewing the comments and considering the potential impact of applying the eSLR standard to covered depository institutions as a regulatory capital buffer, rather than as part of the definition of “well capitalized” in the prompt corrective action framework, the agencies have decided to finalize this aspect of the proposal as proposed. The agencies are retaining the minimum supplementary leverage ratio threshold of three percent to be considered “adequately capitalized” under the prompt corrective action framework.[42]

The agencies continue to expect that a buffer approach will enhance effective capital management across a banking organization, have fewer pro-cyclical effects as it would provide “early warning” benefits relative to the prompt ( printed page 55258) corrective action-based approach, and lessen the likelihood that a covered depository institution will reduce lending and other activities during times of economic stress.

At the same time, the payout restrictions of a leverage buffer framework will provide an incentive for covered depository institutions to maintain sufficient capital and reduce the risk that their capital levels may fall below their minimum requirements during economic downturns.

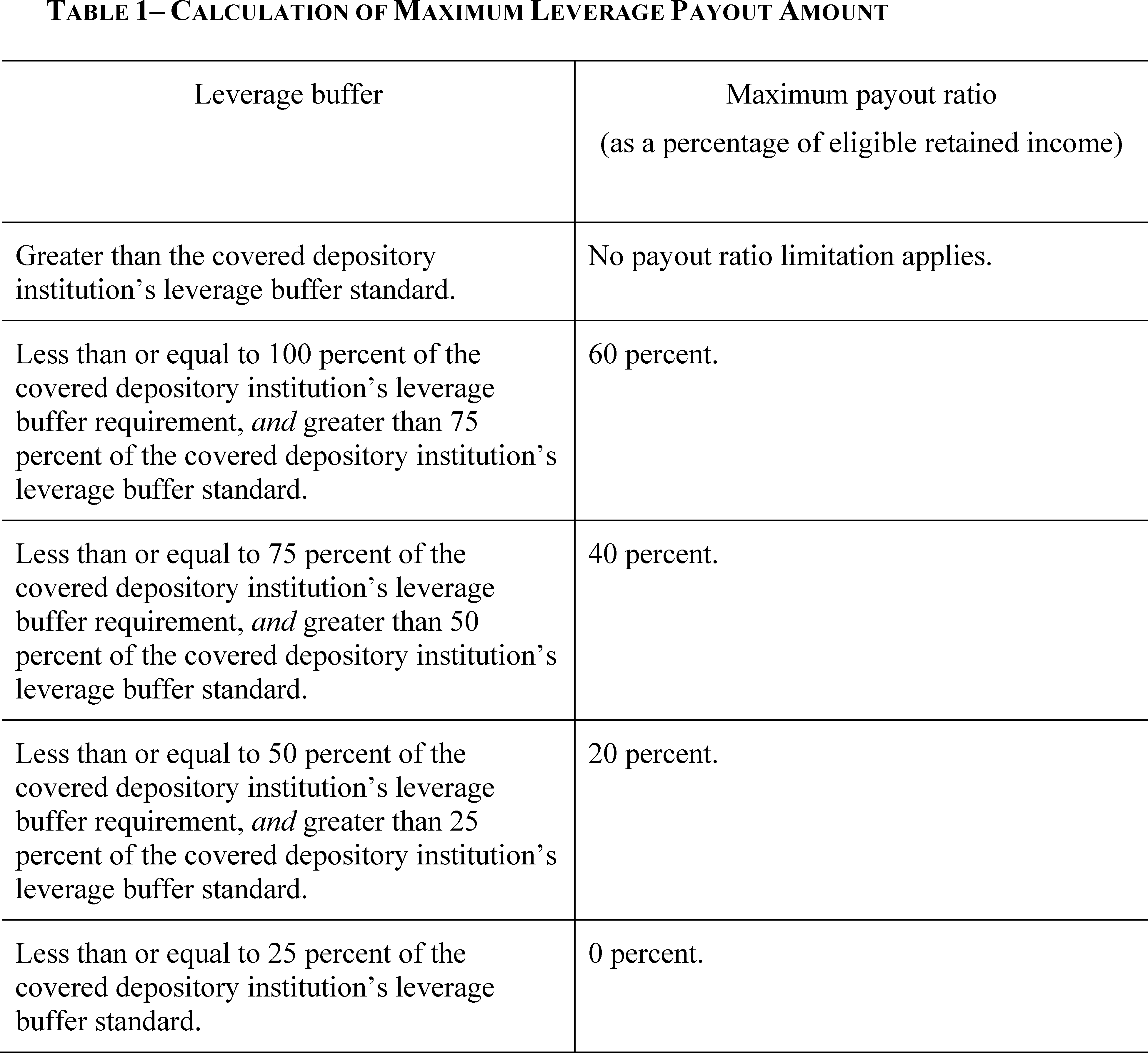

Consistent with the proposal, the final rule implements a leverage buffer framework that follows the same general mechanics and structure as the capital conservation buffer and the leverage buffer applicable to GSIBs currently contained in the agencies' respective capital rules. A covered depository institution will need to have a supplementary leverage ratio equal to three percent minimum supplementary leverage ratio requirement plus the eSLR buffer standard to avoid limitations on capital distributions and certain discretionary bonus payments. If the covered depository institution maintains a leverage buffer that is less than or equal to 100 percent of its leverage buffer standard, a payout limitation will apply in accordance with Table 1 below. The limitations on distributions and discretionary bonus payments will be applied to a covered depository institution alongside any limitations imposed by the capital conservation buffer or any other supervisory or regulatory measures. If the depository institution is constrained by either the capital conservation buffer or the leverage buffer, or both, the depository institution will be required to apply the more binding payout ratio.

{kind=link}

B. Amendments to Total Loss-Absorbing Capacity and Long-Term Debt Requirements

The proposal would have made conforming amendments to the leverage-based components of the Board's TLAC and long-term debt requirements to maintain alignment of these components with the eSLR buffer standard for GSIBs. Under the TLAC framework, GSIBs must maintain outstanding minimum levels of TLAC based on risk-based and leverage-based measures. GSIBs must also maintain TLAC levels sufficient to meet buffers on top of both the risk-weighted asset and leverage components of the TLAC requirements in order to avoid ( printed page 55259) limitations on their capital distributions and certain discretionary bonus payments.[43] The leverage-based TLAC buffer is equal to two percent, above the 7.5 percent minimum leverage component of a GSIB's external TLAC requirement.[44] This buffer amount was expressly designed to align with the eSLR buffer standard applicable to these firms.[45] Accordingly, the Board proposed to replace the two percent TLAC leverage buffer with a new TLAC leverage buffer equal to the eSLR buffer standard under the proposal.

The Board also requires GSIBs to maintain a minimum leverage-based external long-term debt amount equal to a GSIB's total leverage exposure multiplied by 4.5 percent. As described in the preamble to the final rule that established the long-term debt requirement, the requirement was calibrated primarily on the basis of a “capital refill” framework.[46] According to the capital refill framework, the objective of the external long-term debt requirement is to ensure that each GSIB has a minimum amount of eligible external long-term debt such that, if the GSIB's going-concern capital is depleted and the covered bank holding company fails and enters resolution, the eligible external long-term debt can be used to replenish the GSIB's going-concern capital to at least the amount required to meet the minimum leverage capital requirement and buffer applicable to GSIBs. Therefore, the Board proposed to revise the minimum leverage-based external long-term debt requirement to reflect the proposed change to the eSLR standard. The proposed minimum leverage-based external long-term debt requirement would have been total leverage exposure multiplied by 2.5 percent (the minimum supplementary leverage ratio of three percent minus 0.5 percentage points to allow for balance sheet depletion) plus the eSLR buffer standard under the proposal.

The Board also requested comments on other potential adjustments to the TLAC and long-term debt framework that it should consider, including whether the Board should apply a 50 percent haircut on the amount of long-term debt principal that is due to be paid in one year or more but less than two years that can be considered for purposes of the minimum TLAC requirements and buffers. In addition, the Board requested comment on the advantages and disadvantages of adjusting the amount of balance sheet run-off embedded in the minimum long-term debt requirement or of removing the assumption of balance sheet run-off entirely from the minimum long-term debt requirement.

The Board received several comments on the proposed changes to the TLAC and long-term debt requirements. Many commenters supported the proposed changes, seeing them as necessary to maintain the internal consistency of the Board's regulatory framework. Some commenters opposed the proposed modifications to TLAC and long-term debt requirements, asserting that they would undermine the orderly resolution of GSIBs and weaken the safety and soundness of the U.S. banking system, particularly given these commenters' concerns with declines in capital requirements resulting from the proposal. One commenter suggested that the Board clarify how the proposed changes would interact with the resolution planning process.

In response to a question asking whether the Board should apply a 50 percent haircut on certain long-term debt used to satisfy the TLAC requirement and buffers, some trade association and banking organization commenters recommended that the Board not do so, arguing that the 50 percent haircut would add significant costs for issuers without material benefits. Some commenters also recommended that the Board eliminate, or reduce, the long-term debt requirement and thereby allow firms greater flexibility to determine the composition of their TLAC. Some trade association and banking organization commenters also recommended that the Board eliminate the existing 50 percent haircut on long-term debt that is due to be paid in one year or more but less than two years and which is used to satisfy the long-term debt requirement as well as the assumption of balance sheet run-off. Several commenters recommended that the agencies rescind the 2023 long-term debt proposal applicable to certain non-GSIBs. One commenter suggested that the TLAC requirement applicable to U.S. intermediate holding companies of foreign banking organizations be recalibrated to account for their risk profiles, local supervisory frameworks, and particular structural considerations.

The final rule revises the TLAC and long-term debt requirements as proposed. As discussed in the proposal, these changes maintain alignment between the TLAC and long-term debt requirements and the enhanced supplementary leverage ratio standard for GSIBs, in accordance with the manner in which these requirements were originally calibrated. Consistent with the proposal, the final rule does not change the minimum level of TLAC that a GSIB is required to maintain or change the general structure of the TLAC and long-term debt frameworks.

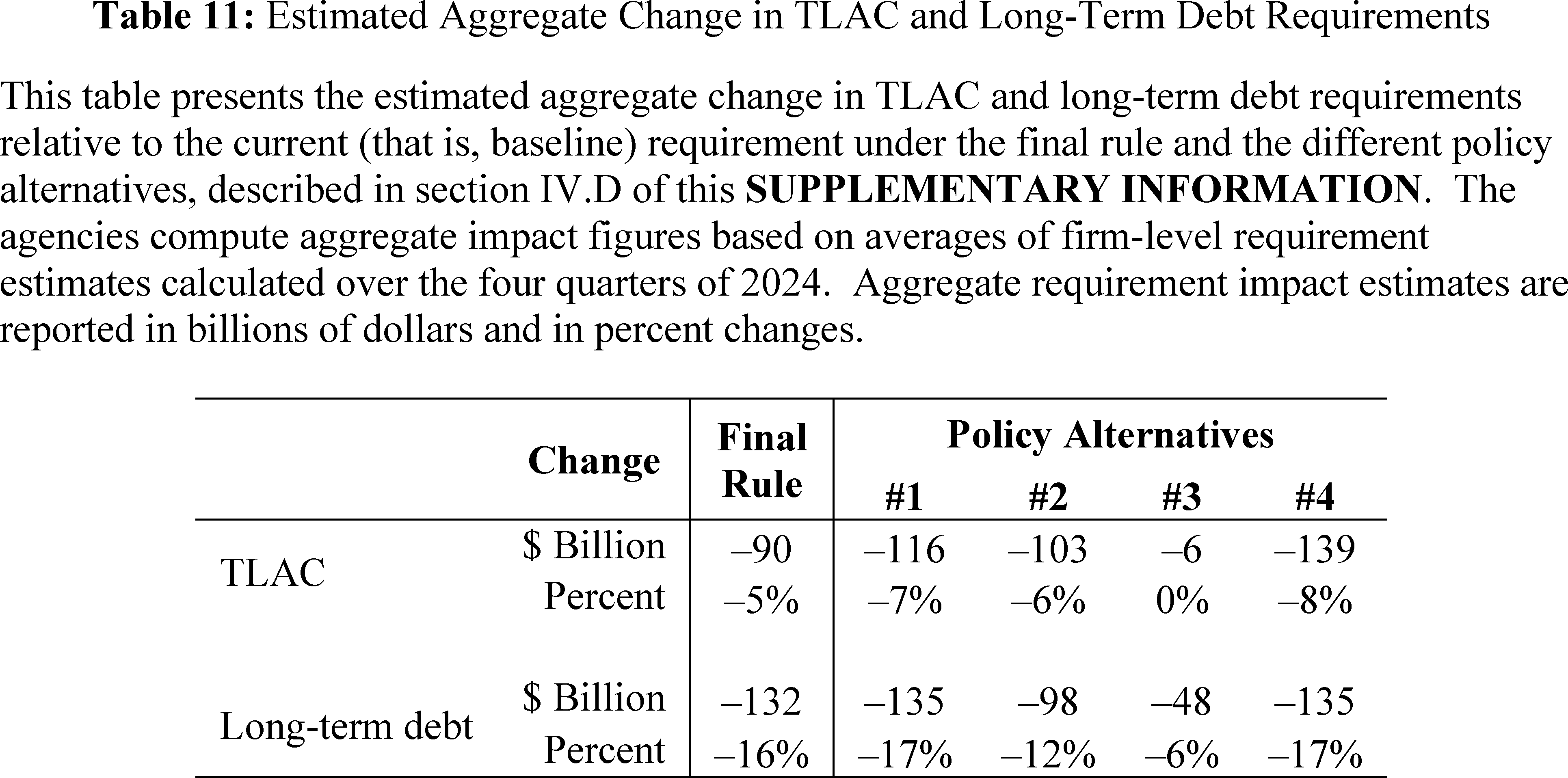

As discussed in section IV.I of this SUPPLEMENTARY INFORMATION , the final rule results in a reduction in the overall level of TLAC for some GSIBs and in the levels of long-term debt necessary to comply with the long-term debt requirement for all GSIBs. However, GSIBs will continue to be subject to robust TLAC and long-term debt requirements.

The Board considered commenters' views on other potential modifications it could make to the TLAC and long-term debt frameworks. Consistent with the proposal, the Board is not making any further changes to the TLAC and long-term debt frameworks at this time and is amending these requirements only to maintain alignment with the eSLR standards.

C. Applicability Thresholds of the eSLR Standard for OCC-Supervised Institutions

The OCC's eSLR standard applies to national banks and Federal savings associations that are subsidiaries of holding companies with more than $700 billion in total consolidated assets or more than $10 trillion in total assets under custody.

In the proposal, the OCC proposed to revise the applicability thresholds of its eSLR standard to be consistent with the Board's regulations for identifying GSIBs and applying the eSLR standard only to national banks and federal savings associations that are subsidiaries of bank holding companies identified as GSIBs. In the proposal, the OCC further noted that the asset thresholds the OCC uses to determine applicability of the eSLR standard scope in all the national bank and federal savings association subsidiaries of GSIBs, but no other institutions. Therefore, this proposed change would not have had any practical impact on the current application of the eSLR ( printed page 55260) standard to national banks and federal savings associations.

Some commenters supported the proposal to revise the scope of the OCC's eSLR standard and asserted that it would be appropriate to remove the thresholds based on asset size and custody activities and instead reference the GSIB determinations made under the Board's rules. The commenters asserted this revision would have harmonized the OCC, FDIC, and Board rules and would not result in unintended consequences.

One commenter, on the other hand, argued against adopting this aspect of the proposal. This commenter acknowledged that the proposed change would not have any immediate impact, but it noted that the OCC's standard was potentially broader than the Board's and FDIC's and may capture different banking organizations at some point in the future. The commenter further suggested expanding the application of the eSLR standard to scope in even more organizations, including those with well below $700 billion in total consolidated assets because, according to the commenter, the failure of large regional banking organizations can pose systemic risks.

The OCC has decided not to finalize this aspect of the proposal. The asset thresholds the OCC currently uses to determine the applicability of the eSLR standard scope in all the national bank and federal savings association subsidiaries of GSIBs, but no other institutions. Therefore, the decision not to finalize this aspect of the proposal will have no impact on which entities will currently be subject to the eSLR standard.

Regardless of whether their parent holding companies are identified as GSIBs by the Board, the OCC believes the eSLR standard should apply to those national banks and federal savings associations that the OCC determines pose the greatest risks to public and private stakeholders in the event of adverse performance, disruption, or failure of the national banks or federal savings associations or the activities they engage in. The OCC will continue to monitor the national banks and federal savings associations under its supervision and as the banking industry grows, the OCC will consider whether changes are needed to ensure the continued appropriate application of the eSLR standard through a future rulemaking action, if necessary.

D. Comments on Other Potential Modifications to the Supplementary Leverage Ratio Requirement and Other Elements of the Agencies' Regulatory Framework

In addition to the proposed changes to the eSLR standards, the proposal requested comment on potential additional or alternative changes the agencies could make that would achieve the objectives of the proposal. The Board requested comment on a specific potential additional change, the narrow exclusion approach described above. The proposal also requested comment on other changes to the bank regulatory framework that the agencies should consider to reduce regulatory impediments to well-functioning U.S. Treasury markets.

Many commenters opposed any exclusions from the supplementary leverage ratio denominator, including the narrow exclusion approach. Some commenters asserted that the narrow exclusion approach would diminish the effectiveness of the supplementary leverage ratio requirement, which broadly treats assets and exposures in a risk-insensitive manner, and that the narrow exclusion approach would prompt requests for additional exclusions that would further erode the risk-insensitive nature of the requirement. Other commenters asserted that the narrow exclusion approach—and other approaches that exclude assets or exposures from the supplementary leverage ratio denominator—would represent a departure from the Basel Committee's leverage ratio framework and could invite a “race to the bottom” in the international regulatory treatment of sovereign exposures. Additionally, some commenters expressed concern that the narrow exclusion approach would lead banking organizations to increase holdings of Treasury securities, including longer-dated securities that carry greater interest rate risk, a scenario which, in these commenters' view, could lead to banks having inadequate capital to absorb losses from shifts in market interest rates. Finally, one commenter expressed doubt that the narrow exclusion would result in a meaningful increase of U.S. Treasury market intermediation.

A few commenters supported including the narrow exclusion approach in a final rule, and some additional commenters expressed openness to this concept but supported finalizing the proposal without the narrow exclusion. One commenter stated that the narrow exclusion approach may aid market intermediation while limiting additional exposure to interest rate risk, since the securities excluded from total leverage exposure would be trading securities measured at fair value and would be subject to the market risk capital requirements of the risk-based capital framework. Another commenter asserted that the narrow exclusion approach would provide some incremental support for Treasury market intermediation, but the approach's benefit would be limited by the current method 2 GSIB surcharge calculation in the risk-based capital framework.

Other commenters suggested broader exclusions from the supplementary leverage ratio denominator. Some commenters suggested excluding banking organizations' deposits held at central banks (reserves); reserves and short-term Treasury securities; or reserves and all Treasury security holdings. In addition, one commenter supported excluding from the denominator of the supplementary leverage ratio all reserves, Treasury securities, and repurchase and reverse repurchase agreements backed by Treasury security collateral across all entities within a banking organization. A few commenters called for applying some of these exclusions to all leverage capital requirements applicable to banking organizations. Some commenters requested that the agencies state that they may exclude certain assets from total leverage exposure during exceptional macroeconomic circumstances, as the agencies did on a temporary basis through interim final rules in 2020, as the onset of the COVID-19 pandemic significantly and adversely affected global financial markets.[47]

The final rule does not adopt the narrow exclusion approach or other exclusions requested by commenters. As discussed in the proposal and in section IV of this SUPPLEMENTARY INFORMATION, and as observed by many of the commenters, the final rule's changes to the eSLR standards achieve the objectives of the rulemaking and continues to broadly treat exposures equally under the supplementary leverage ratio framework.

The proposal also included a question about potential additional modifications to the regulatory capital framework that the agencies should consider to reduce ( printed page 55261) regulatory impediments to well-functioning U.S. Treasury markets. Many commenters recommended several additional changes to the regulatory capital framework for the agencies to consider in potential future rulemakings. Specifically, some commenters suggested modifying the GSIB surcharge framework by, for example, removing U.S. Treasury security holdings or other assets or exposures from the GSIB surcharge calculation and recognizing the risk-mitigation effects of cross-product master netting agreements in the standardized approach for counterparty credit risk.[48] Some commenters advocated for changes to the tier 1 leverage ratio requirement, such as a reduction in the level of the requirement at the holding company and depository institution levels or exclusion of certain assets, such as reserves, Treasury securities, and certain other Treasury-collateralized exposures, from the denominator of the ratio.